The Market: The Importance of the Yellen "Put" Sale

The Market: The Importance of the Yellen "Put" Sale

Treasury Secretary Janet Yellen sold a put last night via coordinated currency intervention, a key signal of future action. With over $900 billion in the TGA, Yellen will get what she wants.

Please see here for more information on The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along (it’s free, after all). Thank you.

Discussion

In last weekend’s Outlook write-up I said:

Based on where long-term US Treasury rates are right now and what realized inflation is doing, SPX has no business trading at 21x 2024 “Street” EPS estimates (5123/243). A still-too-high multiple of 17.5x would mean SPX 4253.

Given the fact the US fiscal deficit is running at 5-10% of GDP and projected to stay there ad infinitum without major policy changes, it is extraordinarily unlikely FED Chair Jerome Powell can return inflation to the Fed’s 2% target - and thus secure his inflation-fighting legacy - by his exit date of May 15, 2026 without engineering a downturn in the US economy. Odds are high that recession is coming in 2025 in the wake of a resumption of rate hikes starting at the December 2024 FOMC meeting. Hence, my quote above about SPX 4253.

So, why is SPX trading above 5000? Very simply: The FEDeral Government Put. Without this put, SPX has tremendous downside as a result of its overvalued state and bullish investor positioning.

Thinking Fast and Slow

The concept of holding two opposing thoughts in your mind as a market participant is always important, but it’s especially critical right now. I *think* a -50% SPX bear market is coming in 2025; so, even if SPX first rallies to 6000 before falling to 3000, one could argue: Why bother being a bull in 2024?

Two things: 1) As outlined in detail in last weekend’s Outlook note, the robust history of the 50dma breadth thrust signal suggests there is an extremely high probability that SPX rises to at least 5603 by December 26, 2024. But the problem with that quantitative outlook is that it doesn’t tell us “why” the market could rise to that level, especially in the face of such a bearish 2025 outlook…which brings us to number 2.

The bottom line is that over time policymakers have proven time and again they will do whatever it takes to get re-elected. The incentives are just too powerful1. Enter: The FEDeral Government Put - the “why” SPX is likely to rise to at least 5603 by the end of this year, if not sooner.

Yellen Sells a Put

In the March WOTE Report I suggested that the FEDeral Government Put sat roughly -2.54% below SPX.

As the market has gone on to correct more than -2.54%, I have questioned my assessment of where the put strike sits. The put still exists, I just thought perhaps the change in the inflation outlook may have dropped the price to -10%, as discussed yesterday morning. But then Yellen stepped in last night with a very clear put sale via coordinated currency intervention.

This is hugely important because it demonstrates that not only the put still exists, but it also clearly reveals the strike price: not even -5% down on SPX.

Yes, the market is unlikely to V-shape out of this correction with Israel-Iran tensions in the air and UST rates elevated; but make no mistake, Yellen stepped in, and she has the tools to ensure she gets what she wants.

Yellen’s Tools

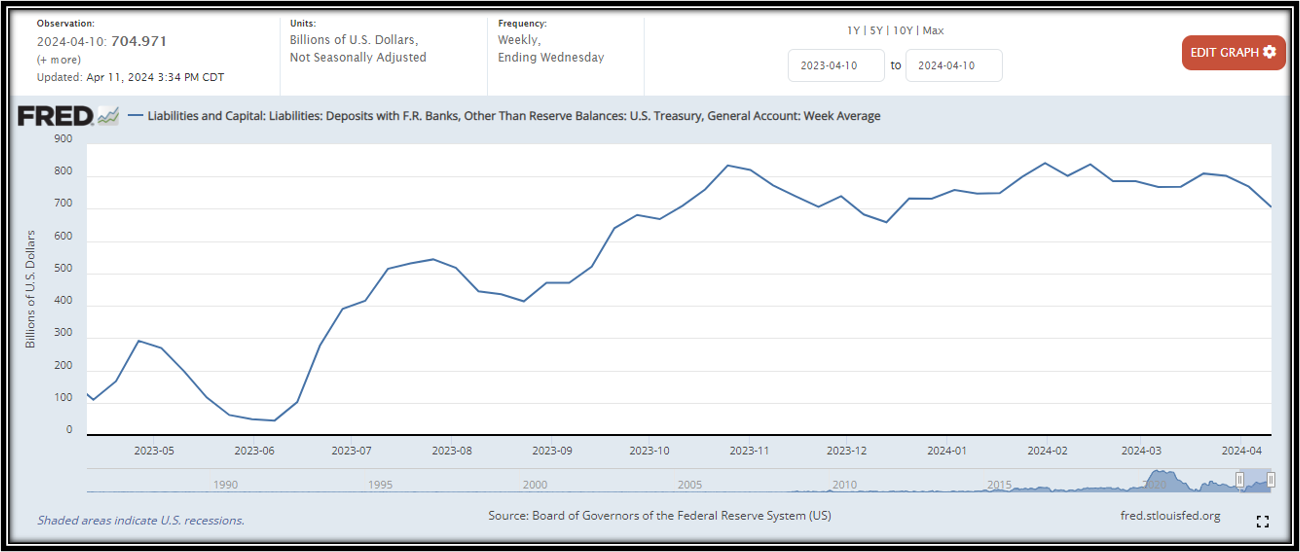

One of the drivers of this SPX pullback is the liquidity drain from tax payments going into the TGA, which rose from $705 billion on April 102 to $906 billion on April 163 and is projected to move to over $1 trillion in the coming days if it’s not there already.

But today’s liquidity drain = tomorrow’s liquidity bazooka.

With the rise in the term premium on a zero coupon 10-year US Treasury note pressuring asset prices, and Yellen heavily incentivized to drive asset prices higher into Election Day, odds are high that Yellen unleashes a liquidity bazooka at financial markets in the coming months via TGA “QE” + a UST Bills-heavy issuance package at the May 1 QRA.

Don’t fight the FEDeral government.

For reference, a month ago Cem Karsan walked through the history of election year returns in populist periods. A great case study that often flies under the radar of market participants looking to catch every 3-5% market wiggle.

April 10 TGA balance.

April 16 TGA balance.