The Market: Goldilocks and the Four Bears

The Market: Goldilocks and the Four Bears

The interaction of investor positioning, labor market data, the price of crude oil, and FED rate policy (the "four bears") will determine when Goldilocks jumps out the window.

Discussion

Interest rates across the UST curve have fallen dramatically since their peak in October. They remain in the range of where they’ve traded since late 2022, but it’s the speed of the fall that makes it dramatic and is why equity market sentiment and positioning have quickly shifted into a bullish posture in anticipation of a soft landing underwritten by FED rate cuts.

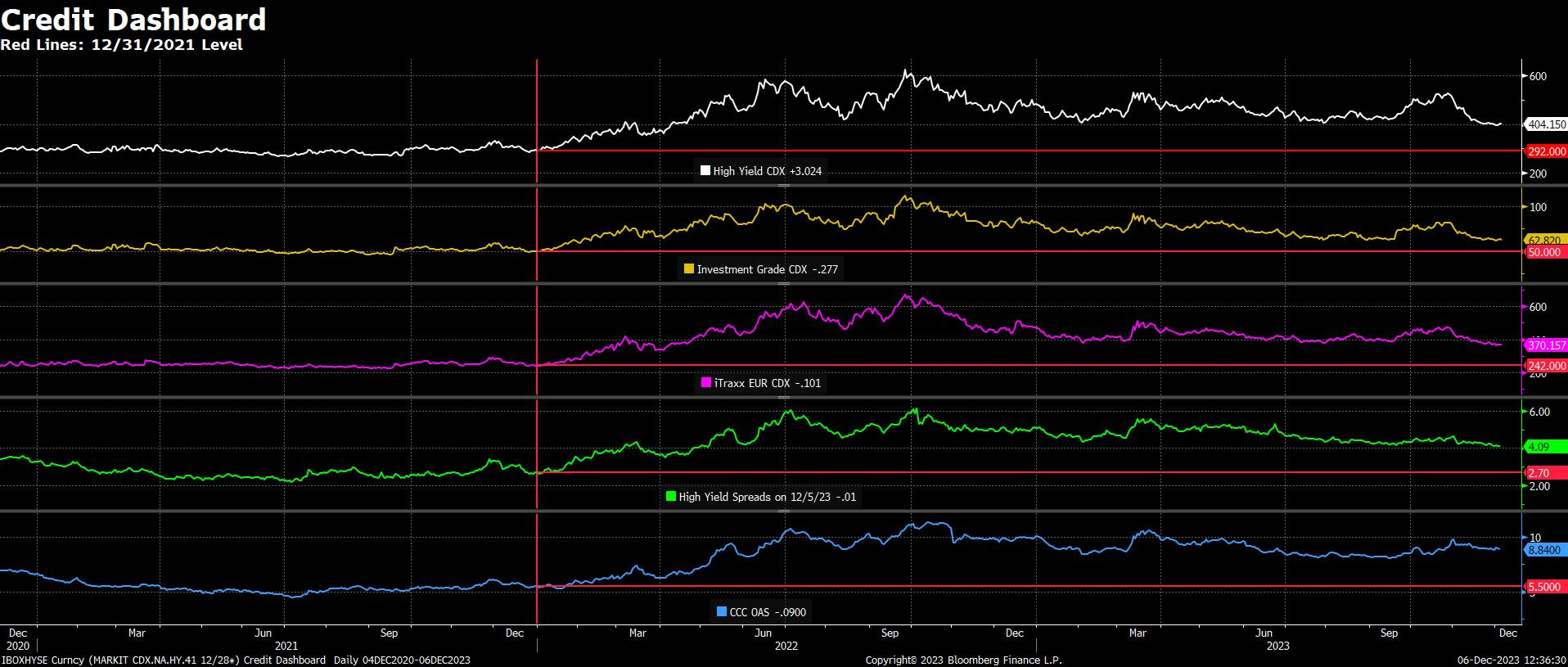

It’s difficult to watch such a sharp in UST rates this deep into a FED tightening program and not conclude that economic weakness is nigh. But right here and now cross-asset market signals do not support that view1: CDXs are drifting lower, Banks are breaking out relative to Utilities, and the equal weight SPX Discretionary sector is breaking out versus the equal weight SPX Staples sector. This is Goldilocks.

How long Goldilocks lasts will be determined by the interaction of the “four bears”: investor positioning, labor market data, the price of crude oil, and FED rate policy.

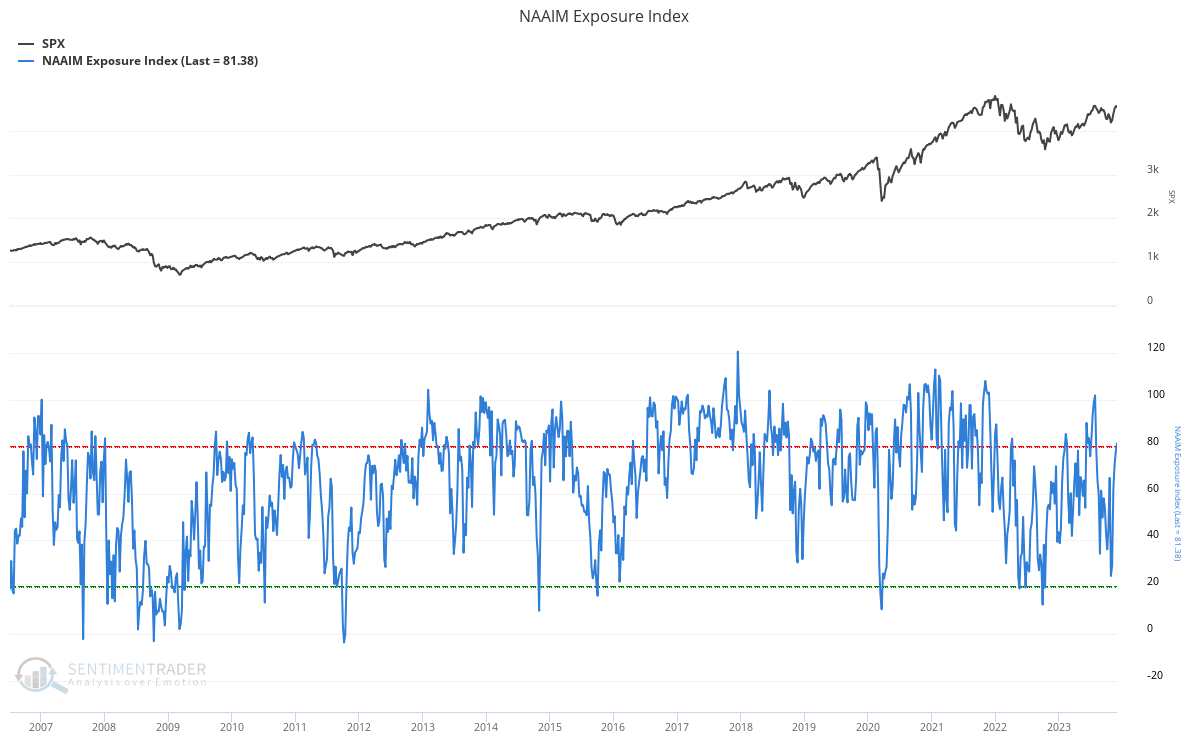

Investor Positioning: Not Yet Full

If and when the NAAIM index - an excellent proxy for broad investor positioning - gets up into the 100-120% exposure zone, it’ll be time to start looking for a key top in equities.

Labor Market Data: Bending, Not Yet Broken

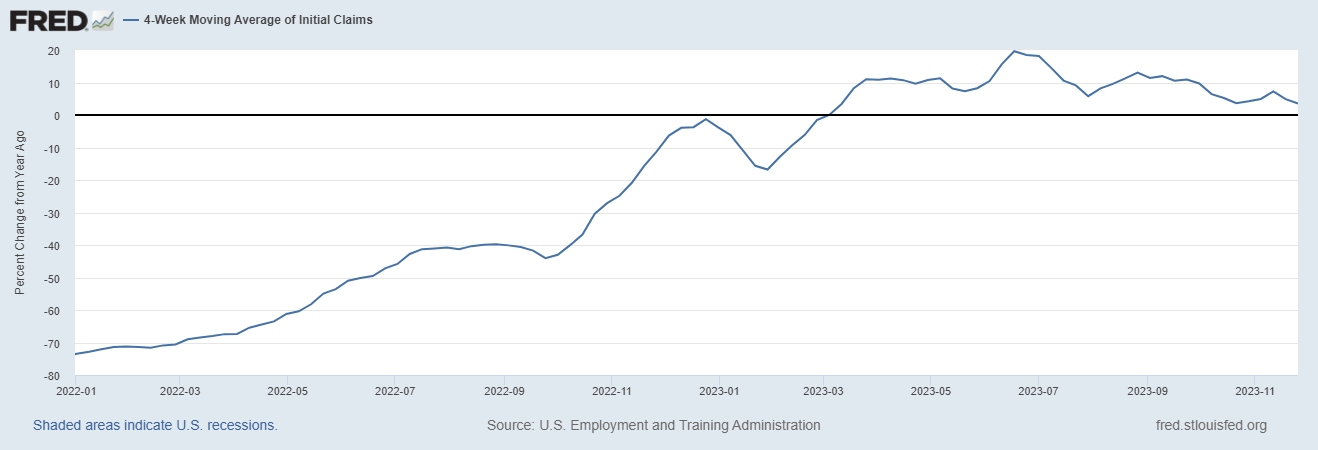

On a YoY basis continuing jobless claims are firmly in pre-recession territory, rising more than 20% since mid-2023. Bending.

But YoY initial claims has yet to sustain itself above the key 20% level. Not yet broken.

Crude Oil: Dragging Down Inflation Expectations

As discussed above, the long end of the UST curve has moved dramatically lower since the highs in October. The move down was kicked off by Treasury’s Bills-heavy QRA announcement, but has since been sustained by a sharp move lower in the price of oil. Key for Goldilocks is the resultant fall in TIPS break-evens. The Fed closely monitors break-evens and becomes equally if not more nervous when break-evens fall below target as they do when break-evens rise above target. As discussed on these pages, the fall in BEs goes a long way toward explaining recent FED dovishness. As such, oil needs to be closely monitored as a risk factor to the Goldilocks trade structure (economic weakness, too, but as discussed above the cross-asset market signaling suggests economic weakness is not yet a major issue).

FED Rate Policy

The Overnight Indexed Swaps (OIS) market is currently priced for the Fed to start cutting Fed Funds by the March 20 FOMC meeting and take it down to circa 410 by December 2024. These cuts are critical to the Goldilocks rally, as they embody the presumption that the Fed is going to do what it takes to engineer a soft landing. So, given the sharp move lower in rates now in place, it’s critical for Goldilocks equity bulls (myself included into January 2024) to monitor FED rhetoric broadly and the December SEP specifically for signs that Powell isn’t quite as Burns-like as it appears.

I believe Powell is playing with fire, as getting weak knees on falling break-evens and softening of labor before the inflation genie is put back into the bottle is even worse than Arthur Burns cutting rates in response to high and rising unemployment. He’s now allowed financial conditions to ease one too many times for the market to take his hawkish side seriously for more than a week or two - heck, nobody has taken his hawkishness as seriously as I have, and even I’m calling him Burns. I think his credibility is likely shot for the time being. However…

As I said last night over private Xwitter (see below), for as badly as Powell wants to go for the soft landing even he cannot be happy with the Burns moniker and getting backed into Rate Cut Corner.

As the xweet outlines, theoretically he could come out with a December SEP that projects no cuts for 2024, which IMO would quickly remove the Burns burden. But that’s unlikely given the specific guidance from Waller about rate cuts 3-5 months from now if inflation is back to target. It’s more likely that he tries to push rate cut pricing into 2H24 and/or explains in detail how maintaining the real Fed Funds rate is not an easing of policy.

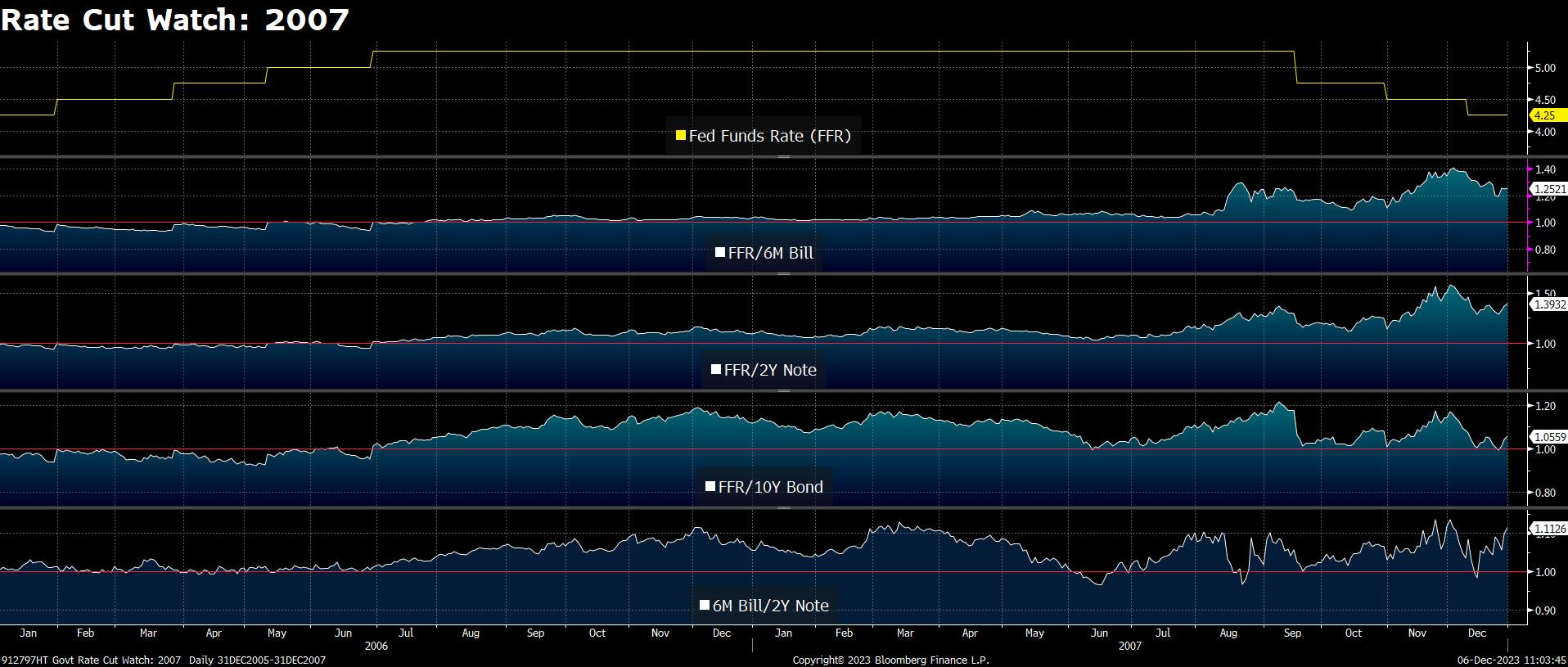

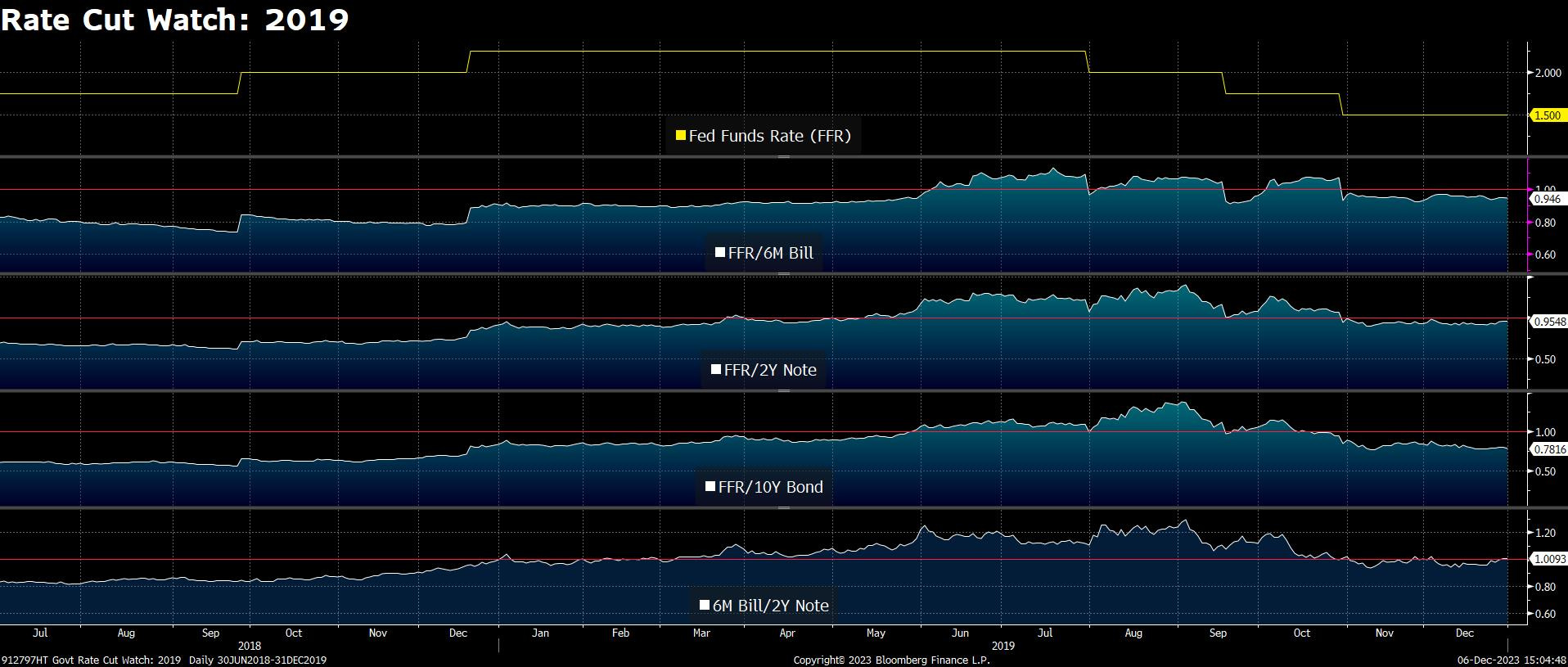

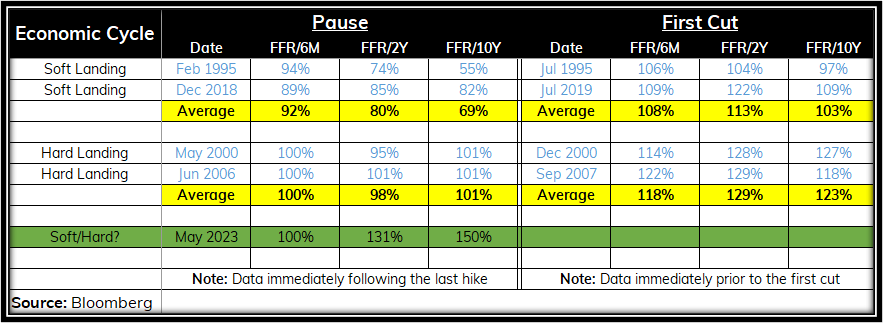

But regardless of how Powell might push back against near-term rate cut pricing, with Fed Funds trading below the 6-month UST Bill rate the current structure of the UST market2 says the Fed is unlikely to cut in March (in the weeks and months leading up to the first rate cut in the 1995, 2019, 2000, and 2007 cutting cycles Fed Funds traded above the 6M Bill rate). And frankly, history says it could take months of Fed Funds trading above the 6M Bill to confirm rate cuts are coming3.

As long as the Fed doesn’t produce a December 13 SEP that projects no cuts in 2024, the Goldilocks trade will be well-positioned to resume into January/February after perhaps a day or two of digestion in response to Powell attempting another hawkish press conference. But beyond January/February equity market bulls need to remain on high alert for the return of “higher for longer” rate policy and rhetoric, especially if investor position is full and/or inflation expectations are moving higher alongside oil.

CDXs and credit spreads are drifting lower.

Banks are breaking out relative to Utilities.

And Discretionary is breaking out relative to Staples.

See the following post from May for more detail on Fed Funds cycles.

Historical cutting cycles.