The Fed: Rate Cuts are Coming

The Fed: Rate Cuts are Coming

While a rate cut is unlikely at the June 14 FOMC meeting, the July 26 and September 20 meetings are very much in play. Don't fight the US Treasury market: rate cuts are coming.

Discussion

One of three conditions would get the Fed to cut the Fed Funds Rate (FFR): underlying inflation falls to and remains on track to stay at 2%; the unemployment rate rises above 6%; or credit spreads widen to levels that obviate the need for the current FFR level. None of those conditions are in place today: FED’s inflation dashboard shows underlying inflation running above 4.5%; the unemployment rate just ticked back down to its cycle low of 3.4%; and key high yield credit spread measures sit right on their long-term averages. These conditions for cuts are well known, and have led financial market participants1 to dismiss the rate cuts priced into the Overnight Indexed Swaps (OIS) market as recession-trigger-happy US Treasury (UST) market participants positioned offsides for what is likely to be “higher for longer” FED policy. In The WOTE’s2 opinion, this is a dangerous line of thinking.

It’s easy to look at the OIS market pricing in a 434 basis points lower bound FFR by year-end and conclude that’s “only” 66 bps lower than the current FFR, and will be repriced higher once better-than-expected economic data are reported and economic bears in the UST market are forced to sell their positions (driving rates and curves higher). But this singular focus on OIS market misses the broader picture painted by the overall structure of the UST market, as discussed in the following section.

Exhibits

The Fed’s underlying inflation dashboard is running well above 2%. Given the very lagging nature of inflation it is highly unlikely the dashboard will show inflation on track to remain at 2% over time soon enough for the Fed to start cutting rates by year-end on this basis alone.

At 3.4%, the US unemployment rate is stuck below the Fed’s 4.5% target for year-end 2023, and well below the 5-6% zone3 it would like to see to ensure inflation returns to its 2% target over time.

Key measures of high yield credit spreads are right on their long-term averages, well below levels that would obviate the need for a 500 bps FFR.

Despite all of the above, the OIS market is currently pricing in 66 basis points of rate cuts by year-end. Given the Fed’s forceful insistence that it will not repeat the “stop and go” policy error of the Burns Fed that underwrote the Great Inflation of the 1970s and 1980s, to turn around and cut so soon after terminating the hiking cycle without good reason for doing so risks material impairment of the Fed’s inflation-fighting credibility. Nevertheless, market participants dismiss this rate cut pricing as simply the result of UST market participants positioning too aggressively for a recession.

Fed Funds Rate Cycle History

Before looking at the current structure of the UST market and what it implies for the direction of FED policy, a look back at past FFR cycles is necessary.

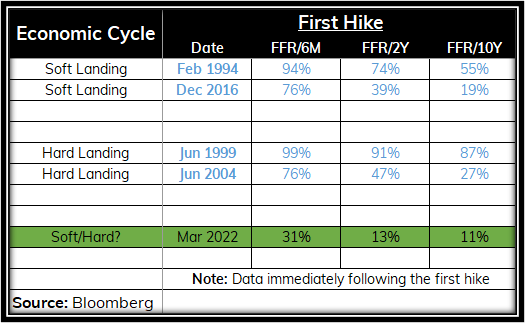

Since the 1994 there have been four clean-cut FFR cycles4, defined as multiple rate hikes of at least 25 basis points, and a multi-meeting pause followed by multiple rate cuts: 1994-1996, 1999-2003, 2004-2008, and 2016-2019. The 1999-2003 and 2004-2008 cycles each coincided with an NBER-defined US recession, commonly referred to as a “hard landing”, while the 1994-1996 and 2016-2019 cycles were successfully-engineered “soft landings” (the Powell Fed's oft-discussed goal for this FFR cycle).

The most straightforward way to assess the structure of the UST market vis-a-vis FED policy is to divide the FFR by a series of progressively longer-dated UST yields. For simplicity of analysis The WOTE uses the following yields: 6-Month Bill, 2-Year Note, and 10-Year Bond.

Historically, upon commencement of the rate hike cycle the FFR is below all longer-dated yields without exception, albeit to varying degrees. For instance, at the start of the 1994 and 1999 hiking cycles the FFR was close to parity with the 6M Bill yield, while at the start of this latest cycle in March 2022 the FFR/6M Bill ratio was just 31%.

The fact the FFR trades below future yields at the beginning of a hiking cycle is the UST market “telling” the Fed it has plenty of room to raise rate without imparting undue harm on the economy.

Now fast forward to the “pause” part of the cycle.

Looking back at history, the pause is where the UST market distinguishes between “soft” and “hard” economic landings. In the “soft landing” cycles of 1994-1996 and 2016-2019, when the Fed paused the FFR/6M, FFR/2Y, and FFR/10Y were 92%, 80% and 69% on average. In both cycles the Fed ultimately cut rates, but it had paused in time to let the economy absorb the impact of rate hikes without tipping into recession.

The “hard landing” cycles are a distinctly different story. At the time of the pause in the 1999-2003 and 2004-2008, the FFR/6M, FFR/2Y and FFR/10Y were 100%, 98% and 101% on average, materially higher than the “soft landing” averages and higher in every individual instance. In those “hard landing” cycles that was the UST market “telling” the Fed it was playing with economic fire.

And finally, the current structure of the UST market.

Don’t Fight the US Treasury Market

The age-old market adages are “don’t fight the Fed” and “don’t fight the tape”. The WOTE would like to add “don’t fight the US Treasury market” to the discussion.

For all intents and purposes the Fed just paused its hiking cycle at the May 3 FOMC meeting. They left the door open to more hikes if needed, but given the low market-based probability of a hike and the current structure of the UST market as discussed below, the Fed is done hiking for this cycle.

Now that the Fed has paused, an assessment can be made as to how the current structure of the UST market compares to the last four FFR cycle pauses. It’s not pretty. Immediately following the May 3 hike to a lower bound FFR of 500 bps, the FFR/6M, FFR/2Y and FFR/10Y were 100%, 131%, and 150%.

Focusing specifically on the FFR/2Y and FFR/10Y for now, at 131% and 150% these ratios are not only well above the two “hard landing” pauses (average and individual instances), they are above the average level (and individual instances) just prior to the first rate cut of the “hard landing” cycles. The UST market is currently pleading for the Fed to ease monetary policy.

As far as the timing of rate cuts, what’s interesting about the current UST market structure is that the FFR/6M ratio is right in line with the “hard landing” pause average of 100%, but well below the “hard landing” pre-cut average of 118%. When the FFR/6M shoots up well above 100%, historically that means rate cuts are no more than a month away, so it’s safe to say at this point that the Fed is unlikely to cut rates at the June 14 FOMC meeting. But given the extreme inversion of the FFR/2Y and FFR/10Y, the July 26 and September 20 meetings are very much in play.

Don’t fight the UST market: rate cuts are coming soon.

Conclusion

The outlook for SPX 2500 by Q1 2024 as discussed on March 31 is very much intact, bolstered by the developments in the banking sector since then and the developing prospect of rate cuts by the September 20 FOMC meeting. More will be discussed in upcoming Market notes, but in the meantime, the late 2007 SPX vs. HY CDX analog (as discussed in the March 31 post referenced above) continues to play out, with SPX chopping around while HY CDX makes a series of higher lows around the critical 500 basis points level. Equity market and economic downside in the coming months and quarters is likely to shock market participants. But don’t be fooled: The US Treasury market is telling us what is to come. Just listen.

Neil Dutta of Renaissance Macro Research wrote a good piece on this issue for Business Insider on April 27.

The WOTE = The Weight of the Evidence

FED insider David Rubenstein said the quiet part out loud in an April 10 CNBC interview, that the Fed would like to see 5-6% unemployment but will never say so publicly.

There were one-off hikes in 1997 and 2015, and non-traditional cutting cycles in 1998 and 2020.

Very well written, thank you!