The Fed: Powell d/b/a Burns

Discussion

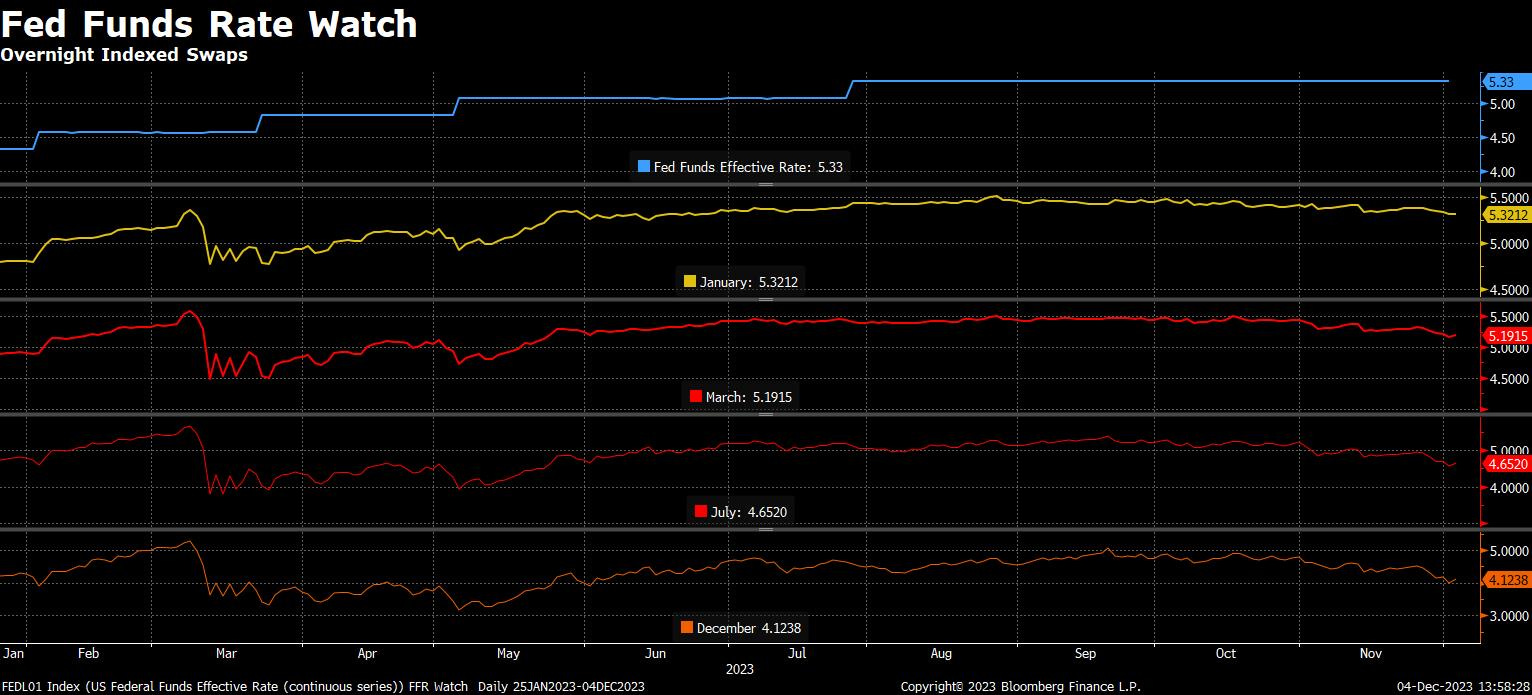

The OIS market currently has the Fed cutting rates sometime between January and March.

In his speech Friday Powell “pushed back” against rate cut pricing, saying:

It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so.

But once he spoke glowingly about the likelihood of a soft landing in Q&A UST 2s sold off from over 470 down to below 455.

Sure, 2s are up from their Friday lows, but the trend is clear since their October 18 peak: DOWN.

D/B/A Burns

Can Powell & Co. come out on December 13 with an SEP that projects no rate cuts from 525-550 in 2024 and follow up with highly aggressive rhetoric to support “higher for longer” rate policy? Sure. But based on Powell’s actions Friday, it sure doesn’t look like it.

On December 1 I wrote about the “Fed Strangle”, with Waller selling the “put” to the market by floating rate cuts 3-5 months from now, and Timiraos selling the “call” leg by expressing the Fed’s desire to not have a “market rally” undermine their war on inflation. I expected Powell to reiterate the “call” leg on Friday, and initially he appeared to by pushing back against rate cuts (the text of his speech was released before he spoke), but both the tone of his speech and the subsequent cooing about a soft landing were the key “tells” about which leg of the “strangle” he favors: the “put” side.

Powell knows exactly what he is doing. He wants easier financial conditions and easier financial conditions he is getting.

Why does he want easier financial conditions? Because he believes inflation is under control.

The infamous “stop and go” policy error of the Great Inflation period was the result of the Burns Fed easing monetary policy in response to rising unemployment. Powell is easing policy at full employment!!!

Powell is d/b/a Burns, full stop.

Fast forward to December 2024 when Fed Funds is 411 as currently implied by the OIS market and a variety of key inflation gauges have turned back up and are trending toward 3.5-4.5%. What’s Powell going to do? Re-hike back to 525-550? 600? 700?

It’s borderline laughable policy at this point.

Sure, I could be misreading the situation and he’ll come out a screeching hawk on December 13 and we’ll be right back into the “FCI doom loop”. But three things say this latest soft landing pivot is different:

Equity market breadth is beginning to point to substantial upside in the next 6-12 months, something that is unlikely to happen from very elevated starting valuations unless the economy really picks up speed over the course of 2024.

The “guts of the stock market” - as Stan Druckenmiller likes to say - are on the edge of confirming the bullish economic message emanating from the breadth signals discussed in point #1.

Lastly, Powell knew exactly what he was doing Friday. Waller knew exactly what he was doing just days prior. They think inflation is under control and are very comfortable with the market pricing over 100 bps of rate cuts in 2024.