The Market: Thinking Slow, Medium, and Fast

The Market: Thinking Slow, Medium, and Fast

Discussion

The 6-18 month outlook for the S&P 500 is very straightforward as long as the Fed is committed to its 2% inflation target. In order to bring inflation back to 2% on a sustained basis, the Fed must bring the US economy into a recession deep enough to raise the unemployment rate to at least 4.5%. Given the “long and variable lags” of monetary policy, that recession is set to hit the US economy sometime in the first half of 2024, at the latest. Historically, around NBER-defined US recessions the S&P 500 troughs at 10-15x cycle peak EPS. As of today, according to S&P Global data the S&P 500 is projected to earn circa $205 per share on an as-reported LTM basis by June 30, 2024. At a mid-point trough P/E target of 12.5x, the S&P 500 looks set to bottom at around 2600 sometime between now and the middle of 2024. That’s thinking slow.

The path from its 8/30/23 closing price of 4515 to 2600 is unclear.

On a medium-term basis SPX appears to be mid-correction ala April and August 2022, where sentiment stalls while the Index moves higher.

On the other hand, SPX could be following the 1987 pattern of a move to new rally highs on the back of consolidating UST 30s.

Setting recessions and analogs aside, SPX has diverged massively from long-term real rates - it is at least 700 points too high relative to TIPS 10s and 30s - as well as HY CDX.

Yes, earnings estimates have moved up, but that simply means the economy is not yet weak enough for the Fed to bring inflation back to 2% on a sustained basis.

Adding it all up, the medium-term outlook for SPX looking out 1-2 months is mixed at best. As JOLTS data proved this weak, the economy could be slowing faster than expected as a result of “long and variable lags”, but that could underwrite a continued soft landing rally where long-term rates fall while economic data remains reasonable stable. On the other hand, as discussed above SPX has diverged massively from rates, setting itself up for a lose-lose situation as the economy slows (recession trade) or reaccelerates (2022 bonds/stocks down trade).

Thinking Fast

On a very short-term basis today was quite telling (I cover all this in real time via the private Xwitter account). HY CDX moved higher throughout the afternoon despite SPX staying bid.

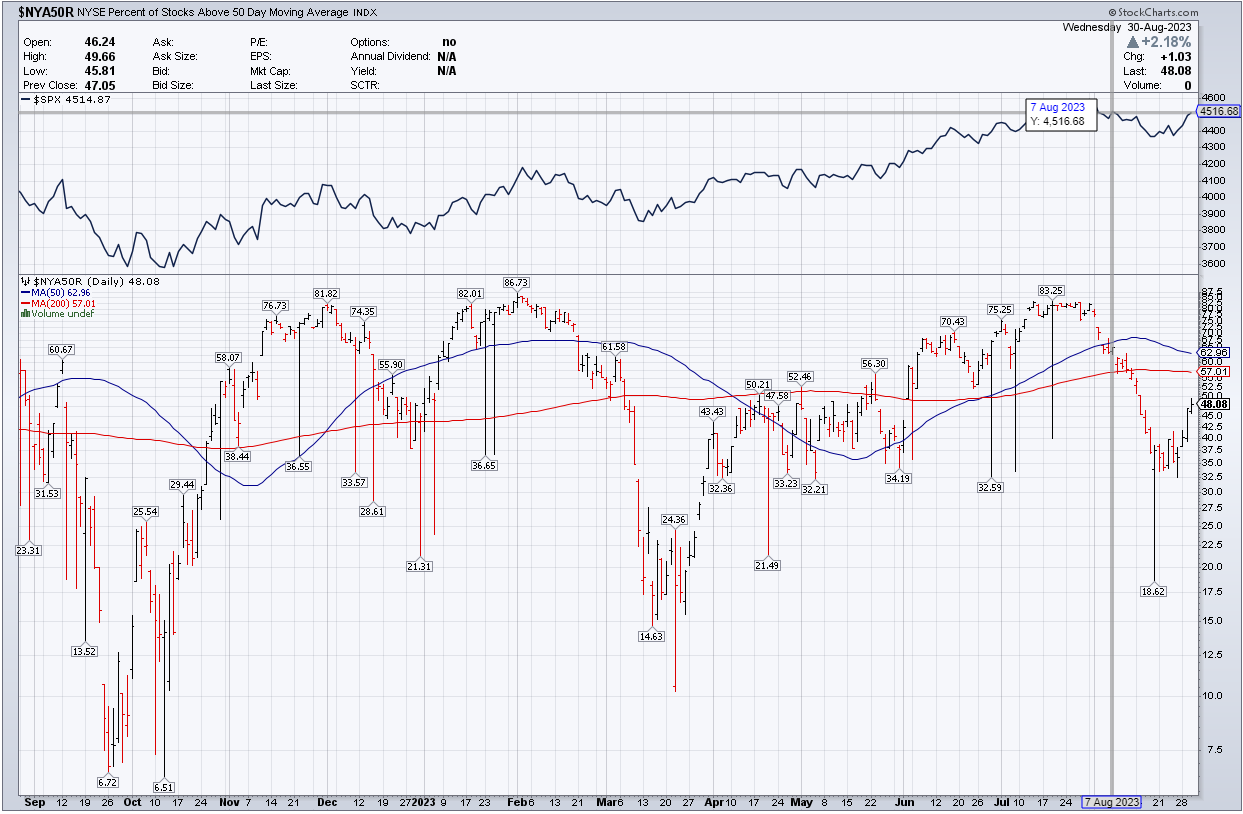

The % of stocks above their 50dma is diverging massively from SPX.

And the % of stocks above their 10dma is rapidly approaching overbought levels.

Lastly, breadth was quite weak today despite the move in SPX and NDX, VVIX outperformed VIX, and defensive sector relative strength actually improved a bit through the day as USTs recovered through the day (i.e. higher rates are likely to be viewed as bearish for stocks here in the next couple of days).

The bottom line: With the big downward move in JOLTS this weak I think the environment is going to be too choppy for a one-way move in either direction. The market is likely to ping-pong in the near-term between “recession” and “soft landing”. Given the negative divergences this afternoon, my guess is tomorrow is a down day on higher rates, but downside is likely limited to no lower than the SPX 100dma circa 4325 ahead of the September FOMC meeting. Once we get through the FOMC, downside opens up into the seasonally dangerous October time frame.

On the other hand, I do not see much upside beyond current levels because I do not believe the “threading of the soft landing needle” is a plausible path. Unicorns are not real - the Fed has either tightened enough to the point the economy is turning down NOW, or they haven’t tightened enough and the economy is in the process of reaccelerating.

From a portfolio management perspective I am thinking about this on two levels: For money with a 6-18 month time horizon I want to be max short and hold, and for money with a 2-12 week time horizon I want to dodge and weave around these 5-10% moves until we reach the point where the economy is very obviously moving down and a tactical short equities position can be held without concern of near-term drawdown. (For informational purposes only, of course.)