The Market: The Path Ahead

The Market: The Path Ahead

A preliminary look at the SPX path to 12/31/2024 and a more tactical view of the next two months.

Discussion

As discussed yesterday in preparation for tomorrow’s TMC space, it’s time to zoom out and look toward the end of 2024 to formulate a higher time frame outlook for stocks and bonds with the following three phases in mind:

2H23 Reacceleration

1H24 Recession

2H24 Election

I’m not going to formulate a detailed outlook here today, as I want to focus on the corrective phase the market is currently in - but preliminarily I could see the following path for the S&P 500 looking out to 12/31/2024:

2H23 Reacceleration: Retest October 2022 low of 3490 in September/October on a breakout in UST 10s to above 500 bps, followed by a relief rally into year-end on a stabilization of long-term rates and not-yet-decisively-negative economic data.

1H24 Recession: 12.5x cycle-peak EPS of $205 (the current estimate1 for LTM 3/31/24 as-reported EPS), or circa SPX 2600 is my recessionary trough target. Far and away the biggest wildcard for where SPX troughs in recession is what FED and Treasury do with over $2 trillion of potential QE stored in the RRP and TGA. If $2 trillion of QE comes into financial markets while the unemployment rate rises to 5%, perhaps SPX never falls below 3000, or perhaps not even below the October 2022 low of 3490.

2H24 Election: Obviously anything can happen, but at this point I have very high confidence 2H24 will be extremely equity market positive as a result of Yellen and Brainard gunning markets ahead of Election Day. This has long been my projection, but now everything is really starting to line up for the 1H24 weakness that would prompt an aggressive policy response.

I will detail my outlook to 12/31/24 in the coming days and weeks. Today I want to focus more tactically on the outlook for September/October, historically a very dangerous period for financial markets.

September/October Danger Zone

On July 1 with the S&P 500 near its YTD high of 4460, I discussed the following three scenarios for 2H23:

Economy performs in line with the Fed’s SEP and they hike twice more to 550. Lags from past tightening limit upside, but ok earnings limit downside, resulting in a range-bound SPX (3800-4600).

Economy outperforms the Fed’s SEP and they hike at the remaining four meetings to close 2023 at a 600 FFR. In this scenario the recent upturn in SPX EPS estimates probably has legs into YE, limiting downside to no lower than the October 2022 low of circa 3500. A breakout in the 10y UST note to 425-450 would likely be the catalyst for a move down to 3500 sometime in the classic danger zone of September/October.

Economy underperforms the Fed’s SEP and they maybe hike once more in July. Economy is far weaker than implied by recent market action and sentiment, lags hit in force, and SPX EPS estimates turn lower. A move down to the upper end of the recessionary bear market trough P/E range (around 15x) would bring the SPX to circa 3000. That’s -36% lower than 4700, a big move in four months if it were to happen by September/October, but a very logical outcome given the fact we have a valuation bubble wrapped in an aggressive tightening cycle…and assuming, of course, that the economy is weaker than “higher for longer” bulls believe.

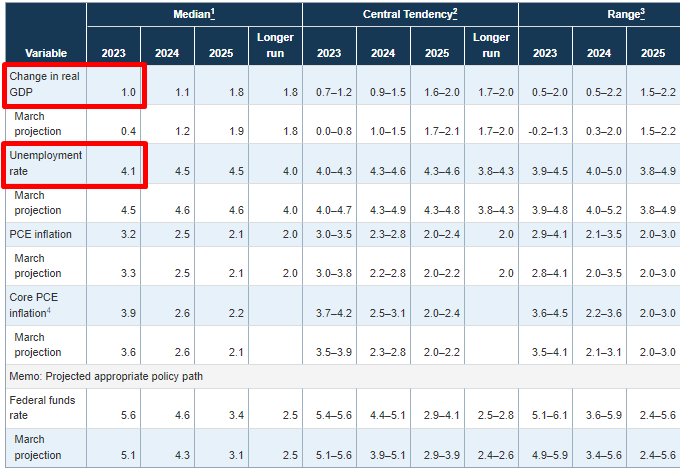

In the June SEP the Fed projected YoY real GDP growth of 1% and an unemployment rate of 4.1%.

Given the fact YoY real final sales have been trending up all year and the FRB Atlanta GDPNow currently projects real growth of almost 6% QoQ annualized in 3Q23…

…It’s safe to say that the economy is on track to outperform the June SEP in 2H23, unless of course the “long and variable lags” of monetary policy suddenly start to bite here in the coming weeks.

In my projection I said that the Fed would likely hike to 600 by year-end in the event the economy outperforms the June SEP, but it’s now looking like the Fed wants to slow-walk its remaining hikes in order to allow the long-end of the curve to “breathe”2. And this makes sense, because the more aggressive they are on the front-end the more inverted the curve becomes and the less the long-end transmits the policy firming the Fed is implementing on the front-end.

Now the question is where SPX heads from here. A full retest of the October 2022 low of 3492 would entail a -24% drop from the July high of 4607 - sizeable, yes, but very much in line with the -22% drop from March 29 to June 17, 2022 from both a magnitude and duration perspective. And March 29 to June 17, 2022 is not random…

The cross-asset market backdrop in April 2022 was very similar to today with SPX meandering lower alongside a bear steepening of the UST curve (done), a brief reprieve on a consolidation of long-term rates (currently underway), then a reacceleration lower on higher rates (likely ahead). HY CDX, VOL, breadth, and sentiment confirm.

Very similar SPX vs. bear steepener today vs. April 2022

SPX finding a reprieve on a consolidation of rates having corrected circa -6% in a meandering fashion.

HY CDX, VOL, breadth, and sentiment all confirm the analog.

S&P 500 EPS estimates from S&P Global.

FRB Boston President Susan Collins is a dovish FOMC member, so when she endorses the recent move up at the long-end that is very deliberate messaging by the Fed that it wants long-term rates up here.