The Market: Bounce Set-Up Into a Window of Weakness

The Market: Bounce Set-Up Into a Window of Weakness

Please see here for more information on The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along (it’s free, after all). Thank you.

Discussion

The S&P 500 has corrected -5.86% peak to trough since March 28, principally due to a sharp rise in the UST 10s term premium to above 0%1. The last three times the UST 10s term premium rose above 0% - March to June 2022, August to October 2022, and July to October 2023 - SPX corrected -22%, -19%, and -11%2.

The question from here is: Will SPX follow the last three analogs into double-digit correction territory, and if so, how deep will the correction be?

The first two term premium-driven SPX corrections were -22% and -19% and in close proximity to each other - a rare combination outside of recession. It was and remains my thesis that those corrections were the direct result of the Fed fighting inflation using asset prices while they worked interest rates higher as fast as they could without crashing the economy and markets. As a result, the “Fed Put” didn’t kick in until -20% down on SPX.

Fast forward to the July to October 2023 -11% SPX correction. With Fed Funds sitting at 533 and within spitting distance of the Fed’s projected terminal rate, and 2-3% realized inflation starting to come into view, the “Fed Put” strike price was higher than 2022. And it’s important to note: the 2023 -11% correction came despite higher starting valuation/positioning than the 2022 corrections3, illustrative of the power of the FEDeral government put.

Bounce Set-Up In Place

As I have outlined ad nauseam (see here, here, and here), I believe Biden & Co. will do whatever it takes to engineer higher asset prices into Election Day. The question is the strike price of the FEDeral government put. In March I posited that the strike price was -2.54% down on SPX. With SPX correcting almost -6% since March 28, clearly I was wrong on the strike price. Now the question is:

With the Federal Reserve seeking to tighten financial conditions in response to 3- and 6-month realized inflation moving above the 12-month rate (see Powell here), how low will Treasury Secretary Janet Yellen allow SPX to fall before she fires her TGA liquidity bazooka at financial markets?

As I wrote about Thursday, I believe the fact Yellen blessed coordinated currency intervention last week was a highly important “put” sale - small, yes, but indicative of where her head is at with regard to financial market volatility. Pre-market on Thursday I said:

These put sales don’t always work immediately, so there could be some chop today; but make no mistake, one does not want to be tactically short of equities with the most powerful policymaker in the world calling “time” on a sub-5% SPX decline.

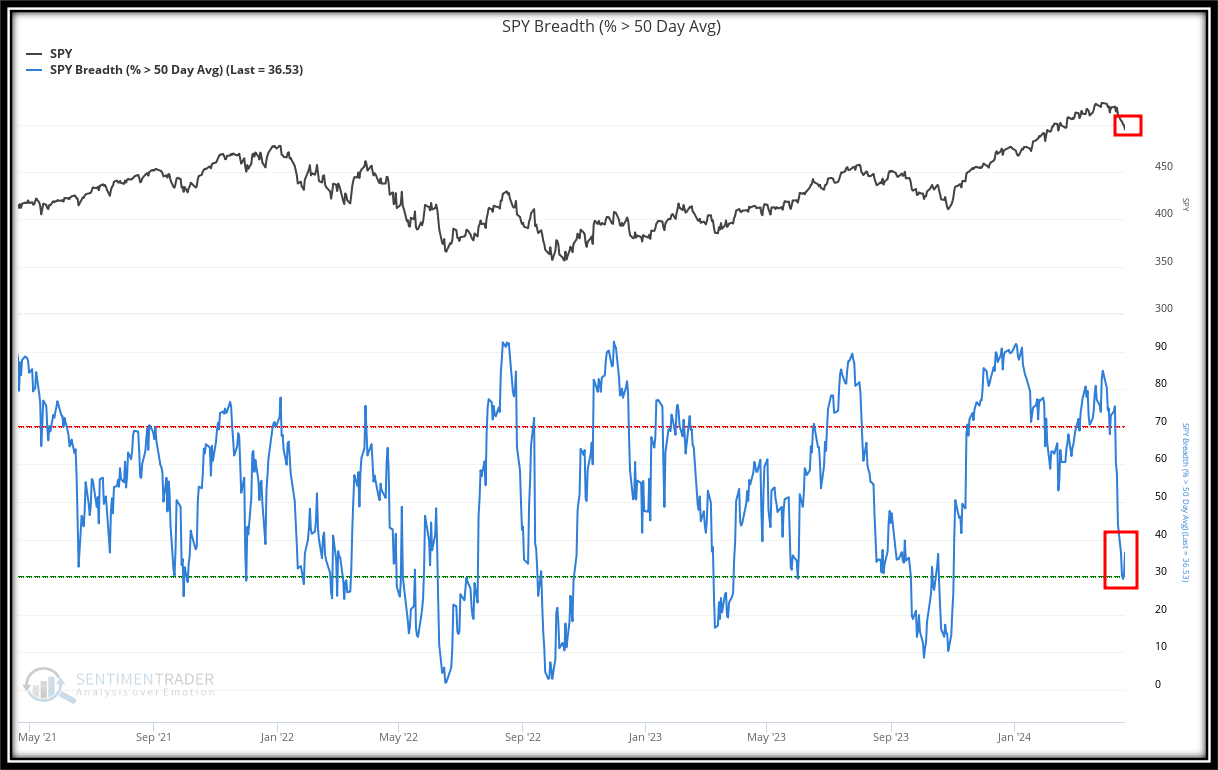

From the close of trading on April 17 to the low on Friday SPY declined an additional -1.34%, proving out the quote above. However, beneath the hood of the broad SPX/NDX indices, 50dma breadth closed higher and IG CDX closed lower4 on April 18 and 19 than they did on April 17 - small albeit key “tells” that Yellen’s put sale is working its way through the system.

In the three term premium-driven corrections cited above, SPX found relief up to its 20dma following the initial 5-6% leg down, and in the 2023 correction specifically SPX rose materially above its 20dma. Given the key bullish breadth/CDX divergences directly in the wake of the Yellen put sale this week, I believe the set-up is in place for a 2-3 day relief rally up to, or slightly above, the current SPY 20dma of $514 early next week.

However, there is a wide open…

Window of Weakness

I believe I am wrong about “H4L Rates and Stocks”. I do not believe the Fed will step aside and allow SPX to decline -20% in a straight line, but I think I was faked out by Chair Powell’s dovishness in front of Congress and at the March FOMC press conference. I’ll have more to say on this front in a self-reflective, process-oriented post about my FED watching framework, but suffice it to say, I think it is better to analyze the broad message coming out of the FOMC ex. Powell; and on that front the message is one of decisive hawkishness pointing toward a June 12 SEP that at minimum shows no cuts in 2024 and potentially a hike if the May 15 and June 12 CPI reports show convincing evidence of a reacceleration of inflation, not simply a stabilization well above the 2% target.

With the QRA and May FOMC both coming on May 1, the set-up is in place for a market-positive one-two dovish punch from Yellen and Powell. But not from current SPX levels.

The Fed was decisively hawkish in the lead-up to its blackout period, leaving financial markets incredibly vulnerable to a wide open window of weakness from now until May 1. I suspect that with SPX -10% off its 5265 ATH circa 4739 by May 1, Powell very likely will present the FOMC message in his standard dovish manner; and if Yellen uses the QRA to unleash her TGA liquidity bazooka, equities will go vertical.

But first things first:

SPY bounce to $514 by Wednesday in order to reset oversold tactical indicators, followed by a

-8% decline to $472 by May 1

More to come on the path beyond May 1.

SPX correction and UST 10s term premium.

SPX corrections the last three times UST 10s term premium rose above 0%.

SPX forward P/E and NAAIM.

50dma breadth and IG CDX.