The Market: April 2022 Redux

The Market: April 2022 Redux

Look for this snap-back rally to conclude today or tomorrow ahead of a likely negative MSFT reaction to earnings on Thursday.

Please see here for more information on The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along (it’s free, after all). Thank you.

Discussion

Market participants currently need to hold three counter-intuitive thoughts in their head at once: SPX is highly likely to rally to 5500-6000 by Election Day; odds are high SPX will experience a -50% recessionary bear market in 2025; and SPX is likely to fall 10-15% to as low as $446 on SPY before this current pullback is over.

As detailed in the WOTE Asset Management Trade Log chat, the way I am positioning for and trading around this discombobulated outlook is as follows:

WOTE US 60/40: Sticking to a max equity overweight of 80/20, in line with the bullish structural and cyclical outlook ratings.

WOTE US Long/Short Equity: Aggressively trading this pullback from the long and short side (currently short), in line with the bearish tactical outlook rating.

WOTE US Special Ops: Aggressively trading this pullback from the long and short side (currently positioned for downside into May 1), in line with the bearish tactical outlook rating.

As discussed in the tactical outlook downgrade yesterday, yesterday’s bounce was unimpressive according to my read of the cross-asset market response. Clearly, that was a premature read, as the market has gone on to rip again today on the back of weak PMI data and modest rate relief. This bounce is exactly in line with what I discussed over the weekend, I was just too quick to downgrade the outlook. With the SPY 20dma sitting around $512, but moving down around 50-75 cents a day, there is still some upside left to perhaps call it $511. But…

The current market set-up looks nearly identical to the April 2022 rates/inflation/FED-driven pullback, which means this bounce is likely to end quickly and sharply…so, I don’t want to get cute playing for a last gasp up to the 20dma, especially with MSFT set to report on Thursday.

April 2022 Redux

This is now the fourth term premium-driven correction in equities since the Fed pivoted to an inflation-fighting policy stance in late 2021.

March-June 2022. Recall, in early 2022 after the Fed backed off on the start of rate hikes amidst the start of the Russia-Ukraine war, Chair Powell gave a hawkish speech in mid-March 2022 laying the groundwork for the Fed to begin hiking rates at 50 bps per meeting. Equities subsequently ripped into the end of March before slowly meandering lower in a low-vol -5.73% pullback from March 29 to April 18 before retracing 3.35% back up to the 20dma. The retracement back up to the 20dma was catalyzed by a hint of relief from rates, with TIPS 30s falling a bit into April 21.

Then from late April to late June the Fed was dragged by the inflation data into even more aggressive rate hikes, guiding to the start of 75 bps hikes in response to the May CPI data reported in June. SPX went on to correct -22% from its late March peak.

August to October 2022. Everyone knows this correction well, kicked off by hawkish August FOMC minutes and then fully catalyzed by Chair Powell’s aggressively hawkish speech at Jackson Hole and the subsequent hawkish September SEP. SPX corrected almost -20% from August peak to October trough.

July to October 2023. The Fed played less of a part in this correction, as the -11% peak-to-trough decline was initiated by the hawkish August 1 QRA issued by Treasury.

The reason I believe this latest term premium-driven correction is strongly akin to April 2022 is three-fold:

It is predominately a Federal Reserve-driven correction. Yes, UST issuance is elevated (I’ll let Andy Constan explain the ins and outs of Treasury issuance policy), but rates have been rising all year and equities didn’t crack until the Fed started aggressively re-hawking. The July-October 2023 correction was predominately Treasury-driven.

Federal Reserve re-hawking is slow-moving. Unlike the August-October 2022 correction where the Fed was very intentionally seeking to drive down asset prices, the March-June 2022 correction was the result of the Fed slowly but steadily tightening the policy screws…precisely what is occurring now.

The Fed is playing catch-up with inflation data at risk of running away from them. In the March-June 2022 correction, the Fed was dragged by hot inflation data into a tighter policy stance. In the August-October 2022 correction, the Fed knew what it was up against and was clearly ready to respond - it was just a matter of getting broader financial conditions into a “sufficiently restrictive” configuration.

Point #3 is critical. The Fed didn’t just overestimate the durability of the disinflationary process in 2H23, it has put itself behind the curve of a clear second inflation wave, as evidenced by the decisive upturn in “supercore” inflation. And you can tell they know they’re behind the curve by the fact they are hinting at the possibility of rate hikes.

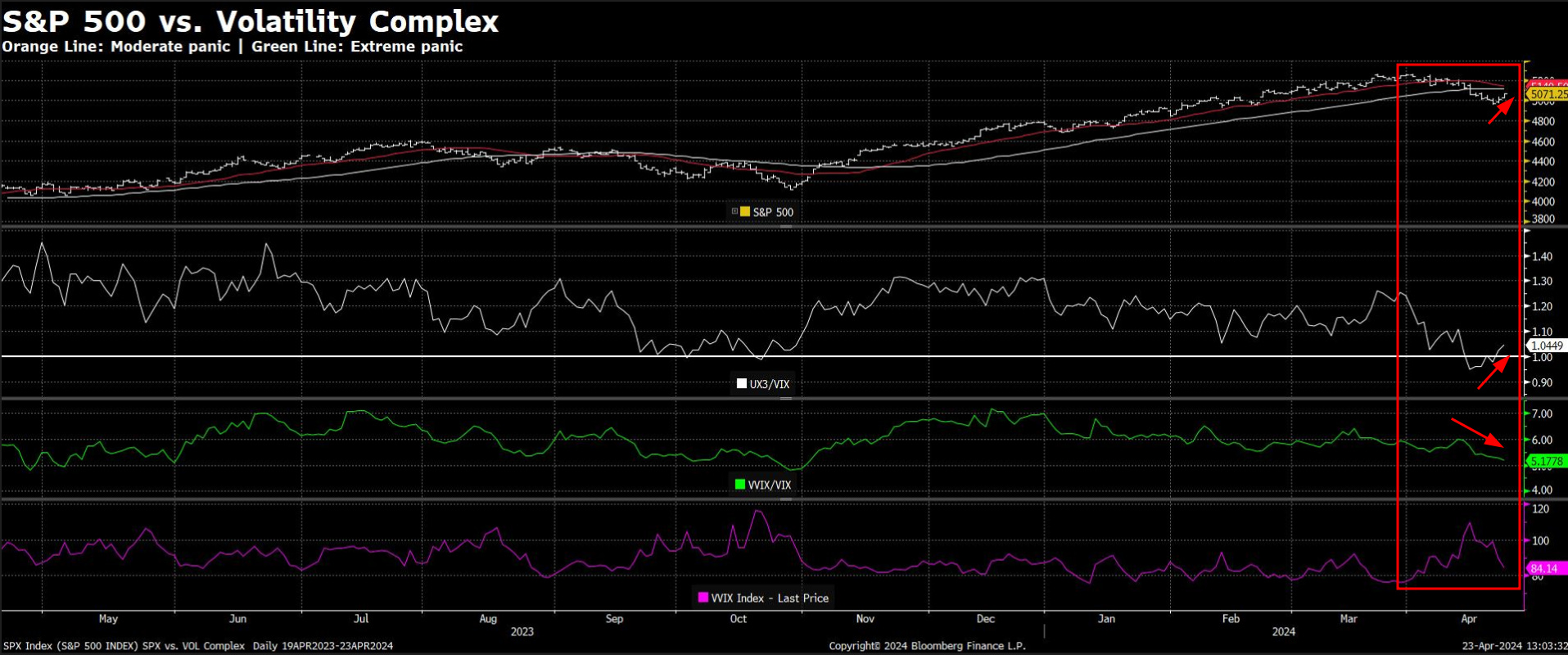

Following the initial -5.73% leg down in April 2022, SPX went back up to retest the 20dma on a small hint of TIPS 30s rate relief while the IG CDX fell back to its 50dma…precisely what is currently underway following SPX’s -5.86% pullback.

Also akin to today is the fact the VVIX/VIX ratio trended lower (bearish) into the April 2022 20dma retest.

Downside Catalyst

There is a confluence of factors pointing to the next leg of SPX downside commencing soon, but one that I believe is going overlooked by many if not all market participants is the vulnerability of the NASDAQ 100, led by MSFT.

NDX has broken key relative strength levels ahead of what I believe will be a negative reaction from MSFT to its earnings on Thursday. MSFT is the greatest company of planet earth, but it is trading at a P/E premium to SPX of almost 70% on NTM earnings, placing it in a very vulnerable position in a market that has taken down otherwise high quality companies with good earnings but trading at overly rich valuations - think: ACN, NFLX, NKE, SBUX, ADBE.

In short, with real interest rates high and rising, the market is starting to care again about valuation. As such, look for the market to use MSFT’s earnings report as an excuse to de-rate ahead of a hawkish FED policy implementation over the course of May and June.