The Market: A Beautiful Set-Up

The Market: A Beautiful Set-Up

With SPX set to open this morning with a poke above its 20dma, Bitcoin failing to confirm the rally, and the groundwork for a hawkish Powell being laid, the set-up for new lows is in place.

Please see here for more information on The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along (it’s free, after all). Thank you.

Discussion

Last week I discussed how similar this market set-up is to April 2022: financial markets in the midst of a slow-moving, term premium-driven correction that saw initial relief up to the SPX 20dma following an initial -6% leg down. This set-up remains eerily prescient.

In April 2022, SPX rallied up to the 20dma but was initially rejected. The following trading day it then opened above the 20dma before reversing hard back down to just above pullback lows. This is EXACTLY the set-up in place today.

It’s currently 8:42am EST and SPY is $509.74 in pre-market trading, just below the last close 20dma of $509.933.

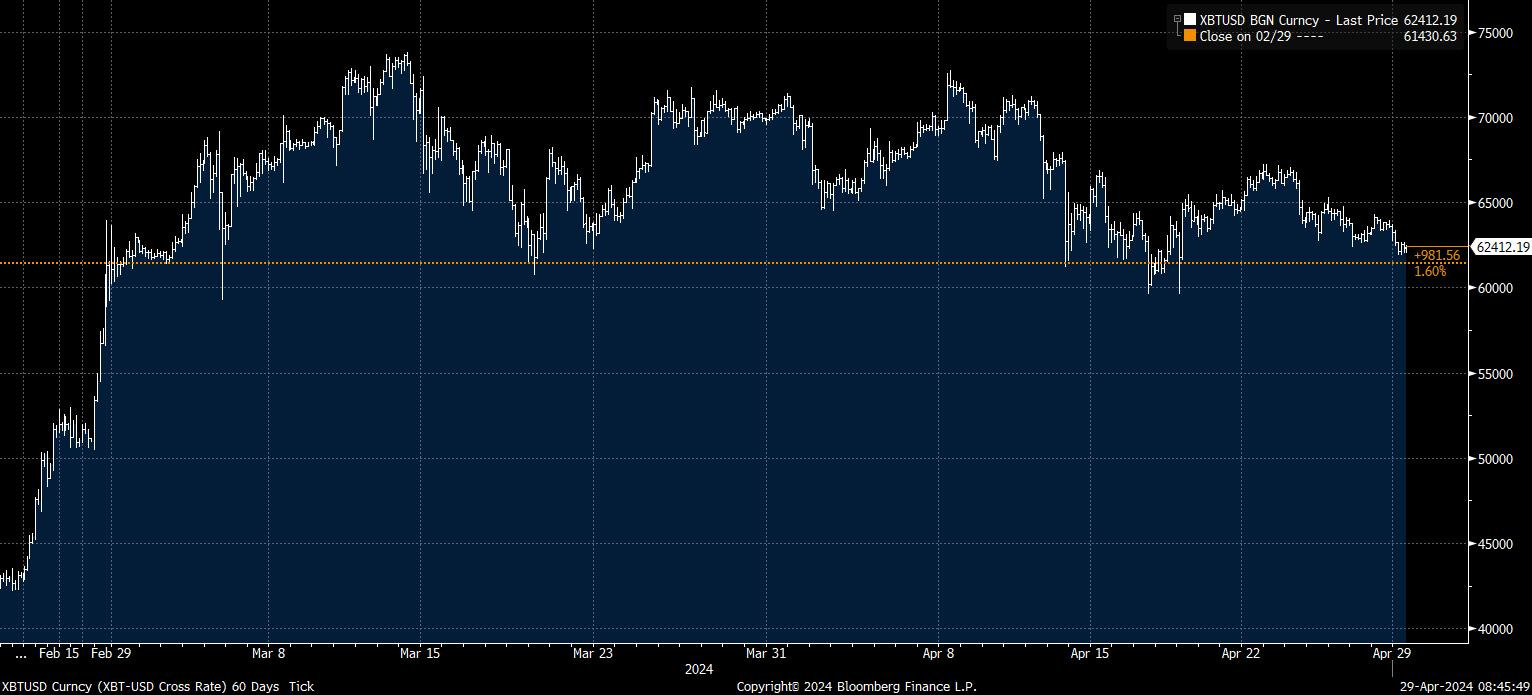

The market is presumably up on currency intervention by the BOJ, but this move is NOT confirmed by the ultimate risk-on indicator, Bitcoin, which is plumbing the lows of the April risk-off environment.

Downside Catalyst: A Hawkish Jay

The catalyst for new SPX lows this week is likely to be a hawkish Jay Powell, as discussed this weekend (see here and here), and my thesis for a hawkish Jay was confirmed in spades by former FED Vice Chair Roger Ferguson this morning. It’s unbelievable how quickly the narrative has shifted from “above-trend growth is ok” to now “the Fed needs to be prepared to engineer below-trend growth and higher unemployment in order to defend the 2% inflation target”, as outlined by Ferguson. This is right back to 2022-style FED policy, and it is no accident SPX is trading as such.

Lastly - this weekend I went back and watched an April 19 Nick Timiraos interview with FRB Chicago President Austin Goolsbee, and the change in tone is stark. Not only does he go out of his way to reiterate with force the 2% inflation target, he does not rule out the possibility of rate hikes, he pontificates about how restrictive policy actually is at present (i.e. pondering if policy is actually “sufficiently restrictive”, which is very clear groundwork being laid for hikes), and he calls out the reacceleration of supercore inflation and the lack of disinflation in housing.

Goolsbee is no FOMC leader. It’s clear he largely parrots what leadership is saying. But the fact he’s parroting such a stark change in stance is striking, particularly given his dovish tendencies.

A hawkish Jay cometh.