The FED: Hawkish Jay Cometh

Please see here for more information on The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along (it’s free, after all). Thank you.

Discussion

What follows is less formal than a typical write-up, as it started out as a text message that went on so long I thought it would work better as a post.

I think Powell plays 4D chess with the market under the cover of data dependence.

I think, by design, Powell follows other FOMC members.

In November/December inflation was decelerating. He wanted to rip markets. I think break-evens were too close to 2% for comfort, and he used decelerating inflation as an excuse to reinflate.

At the January FOMC he took a March cut off the table, following FOMC members’ re-hawking.

Jan/Feb CPI reports were hot. FOMC members re-hawked. Powell knew hawkish policy was coming, so he plays 4D chess with markets and rips them at the March FOMC to foam the runway with higher asset prices.

In March in front of Congress, he’s ultra dovish. Says “we’re close” to cutting based on the data. This shows extreme data dependence. Allows him to pivot in response to hot data.

He stated very specifically before blackout: 3- and 6-month Core PCE inflation is running above 12-month. And that was with markets down and rates ripping.

The data now very obviously and specifically not only do not support rate cuts, but suggest the Fed would be actively debating more hikes were it not for the election.

Powell’s got equity and housing prices near all-time highs, credit spreads tight, and over $900 billion of potential QE sitting in the TGA. MASSIVE cushion in place to attack the last mile of inflation with lower asset prices.

This is the fourth term premium-driven correction in asset prices since 2021: April-June 2022, August-October 2022, August-October 2023, and so far April 2024.

The three prior corrections lasted exactly three months, and resulted in a quick slowing in economic data that allowed FEDeral policymakers to pivot.

Jay and Janet have a window here to manage asset prices lower, slow the economy, cut off the second inflation wave tail, and then pivot with several months to go before Election Day.

Ya, ya. That’s all great: But will he be hawkish on May 1? Isn’t it in his nature to be soothing and calming? Yes, but…

1. 3- and 6-month Core PCE inflation is running ahead of 12-month, so he’s dealing with a real-time reacceleration. He’s demonstrated extreme data dependence. And the data are now hot.

2. FRB New York President John Williams not only very specifically put rate hikes on the table, he said rate cuts wouldn’t come until inflation is back to 2%…a HUGE raising of the rate cut bar. Powell, by design, follows his colleagues. Especially Waller and members of the “Troika”.

3. Today’s Nick Timiraos FOMC preview directly endorses the move at the long end of the UST curve. Counter-intuitively, the more the Fed raises Fed Funds, the more difficult it is for the long end to steepen, which is what matters for taming inflation.

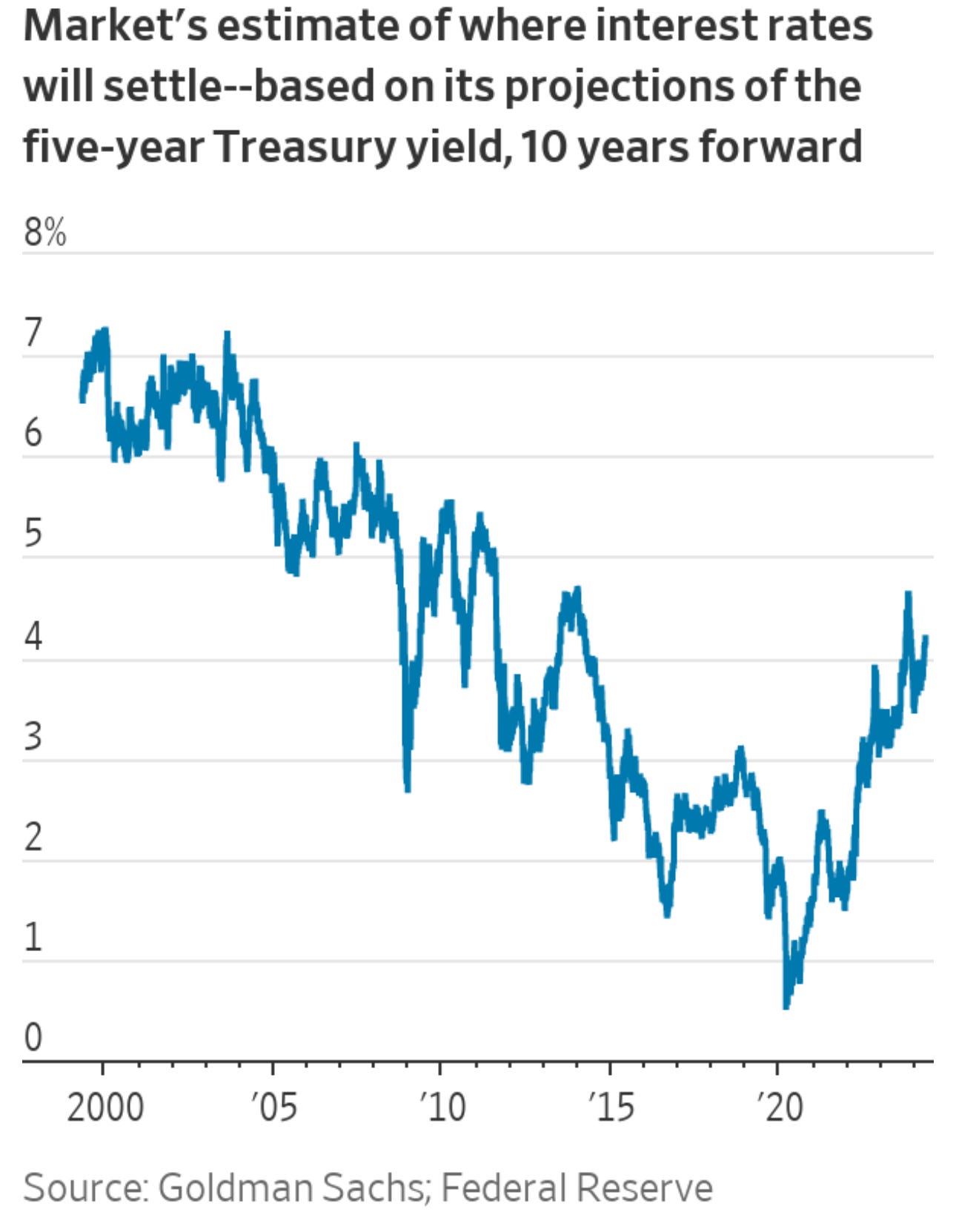

Most importantly, the Timiraos piece specifically called out asset prices, saying that a higher neutral rate has implications for a wide range of asset prices.

Hawkish Jay cometh.

Exhibits

John Williams puts rate hikes on the table while substantially raising the bar to rate cuts.

This morning, through Nick Timiraos the Fed endorsed the market’s estimate of the long-run neutral rate.