The SPX Sector Report: December 4, 2023

The SPX Sector Report: December 4, 2023

Everything but Tech/Energy beginning to turn higher with the lead horse yet to emerge.

Discussion

Please see the November 21 report below for context.

Executive Summary

NDX Group: Struggling at Multi-Year Resistance. On the surface NDX itself appears to be bullishly consolidating around multi-year resistance. But when you walk through the various sub-groups the better description of the situation is “struggling at multi-year resistance.” Even the bulletproof cap weight Communication sector is starting to break down, an area I flagged at last review as an interesting place to allocate to within the NDX Group. With cap weight Communication breaking down, Software (IGV) is probably the most attractive area to allocate to on a pullback to key moving averages. At minimum, I’m in wait-and-watch mode with the NDX Group.

Cyclicals Group: Short Squeeze, or… Everything but Tech (and Energy) has spiked higher in a broad-based short squeeze, so the macro signaling from Cyclicals Group outperformance is a bit muddy here. But the fact the key macro relationships of Banks/Utilities and Discretionary/Staples are breaking out says the Cyclicals Group has the edge over Defensives on at least the near-term outlook for the economy - not enough for a heavy allocation, but enough to keep a close eye on and at least take a shot at the best looking sub-group: Banks and equal weight Financials.

Defensives Group: Prove It. As discussed directly above, the Cyclicals Group has the edge on the economy at the moment. My structural outlook says Defensives are likely to gradually build relative strength over the course of 2024 in anticipation of an economic/market bloodbath in 2025, but they need to prove it with a decisive breakout above key MAs followed by a pullback to test new bulls.

NDX Group: Struggling at Multi-Year Resistance

Cap weight SPX Tech coming back down to earth. Would be bullish to see it consolidate at the former relative strength highs, but middling equal weight relative strength suggests the breakout in cap weight Tech was a blow-off unlikely to hold.

Semis struggling beneath multi-year resistance.

Software the best looking NDX sub-group, but not a buy again until it finds support at key moving averages.

Cap weight Discretionary (essentially AMZN/TSLA) continues to languish.

Cap weight Communication is showing a surprising breakdown. In the last SPX Sector Report I said it looked like a good buy consolidating on its key MAs. Meanwhile, equal weight Communication is showing nascent signs of trying to bottom out, also somewhat contrary to my conclusion at last review.

Lastly, NDX itself is at an interesting spot. It appears to be bullishly consolidating above multi-year resistance, but given the lack of bullish evidence from the review of its various components above, at this juncture it appears NDX should be viewed as struggling at resistance with lots of work left to prove itself it’s going to make a sustainable run to new relative strength highs.

Cyclicals Group: Short Squeeze, or…

At last review my conclusion was that oncoming macro weakness was reflected well in relative strength weakness across the Cyclicals Group. But now the picture is muddied by a short squeeze across everything non-Tech. All equal weight sectors within the Cyclicals Group (with the exception of Energy) have spiked higher, led by Discretionary and Financials/Banks. This spike in cyclicals has coincided with a spike in Defensive sectors, muddying the macro signaling, but the fact the macro-aware Banks/Utilities and Discretionary/Staples relationships are breaking higher suggests the Cyclicals Group is perhaps beginning to sniff out an economic upturn, at least in the short-term. I’m still not comfortable betting heavily on a nascent economic upturn given that the economy is inching deeper into the “long and variable lags” portion of the FED’s tightening program, but I’m also not comfortable betting heavily on an economic slowdown. My conclusion is that a broad-based allocation to equal weight SPX via the RSP ETF is the cleanest way to allocate at this juncture, given Tech underperformance in 2024 is a much higher probability than either a new economic upturn or an economic slowdown. However…

I believe Banks and equal weight Financials are the most interesting areas in the equal weight space, as they’ve been consolidating relative to SPX since SVB in March, and should enjoy twin fundamental tailwinds in the form of Powell d/b/a Burns and cutting rates in March and Yellen/Brainard keeping long rates low into Election Day, therefore boosting the MTM value of Banks’ HTM book. And regardless of whether those tailwinds remain in place, given the scale of RSP underperformance broadly and the length of time Fins/Banks have consolidated specifically, the probability is sustained underperformance in 2024 is quite low outside of an economic/financial market crisis.

Defensives Group: Prove It

The Defensives Group appears to be carving out some form of a relative strength low, but in light of the discussion above regarding Banks/Utilities and Discretionary/Staples, the outlook is too mixed to make an out-sized bet on the Defensives Group versus just simply owning equal weight SPX via the RSP ETF.

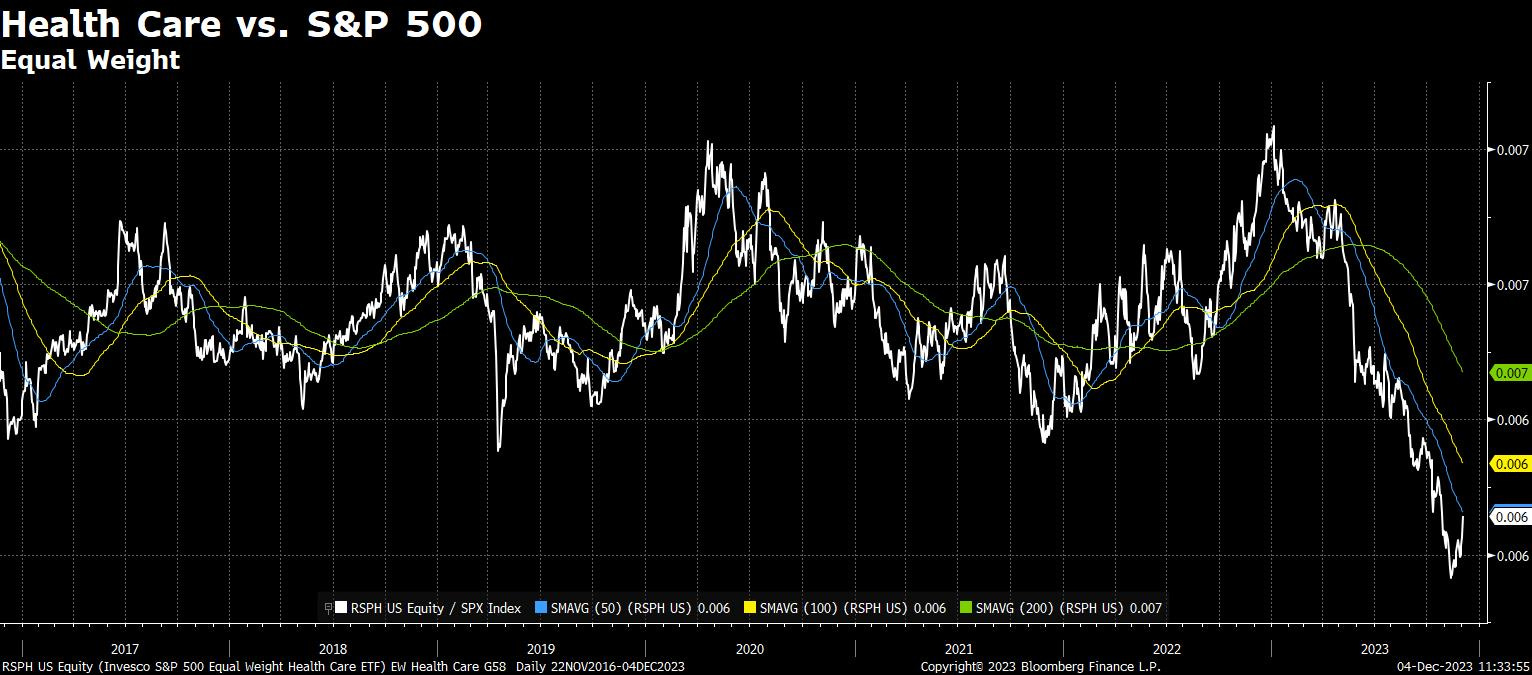

My structural outlook says equal weight Healthcare is the best equal weight sector to own in 2024, as I believe the market will begin to position for an economic/market bloodbath in 2025 (when the full weight of the Fed’s tightening program hits in force) over the course of 2024. But I want to see the group prove it first by breaking out above key MAs and coming back for a retest.