Cyclical Outlook: May 5, 2024

Cyclical Outlook: May 5, 2024

Downgrading the cyclical SPX outlook to "Bearish", implying a high probability of a -10% decline from last close (SPX 5128).

Please see here for more information about The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along. Thank you.

Discussion

The business of markets entails holding competing thoughts in one’s head at all times, often the result of competing time horizons for various views. As outlined in the last cyclical outlook update on April 13, odds are high SPX moves up to 5500-6000 by Election Day, implying a bullish cyclical outlook according to the framework above. But since the April 13 update, three developments have come into view that suggest there is an equally high probability SPX corrects -10% from current levels on its way to 5500-6000 by Election Day:

The oversold condition in place around April 13 has been relieved, clearing the way for SPX to move lower if positioning and fundamental factors allow,

Treasury Secretary Janet Yellen took the TGA liquidity bazooka off the table,

And the Fed has positioned itself to formally move toward rate hike guidance in the June 12 SEP.

In short, “Jay & Janet” proved this week that they are taking the opportunity currently available to tighten financial conditions and slow the economy in time to reflate ahead of Election Day. I suspect a correction down to circa SPX 4500-4700 by June 30 should be enough to slow economic activity enough to allow Jay & Janet to pivot dovishly in July. That pivot *should* underwrite a rally up to that 5500-6000 level implied by the breadth thrust signals that fired in late 2023.

Analysis

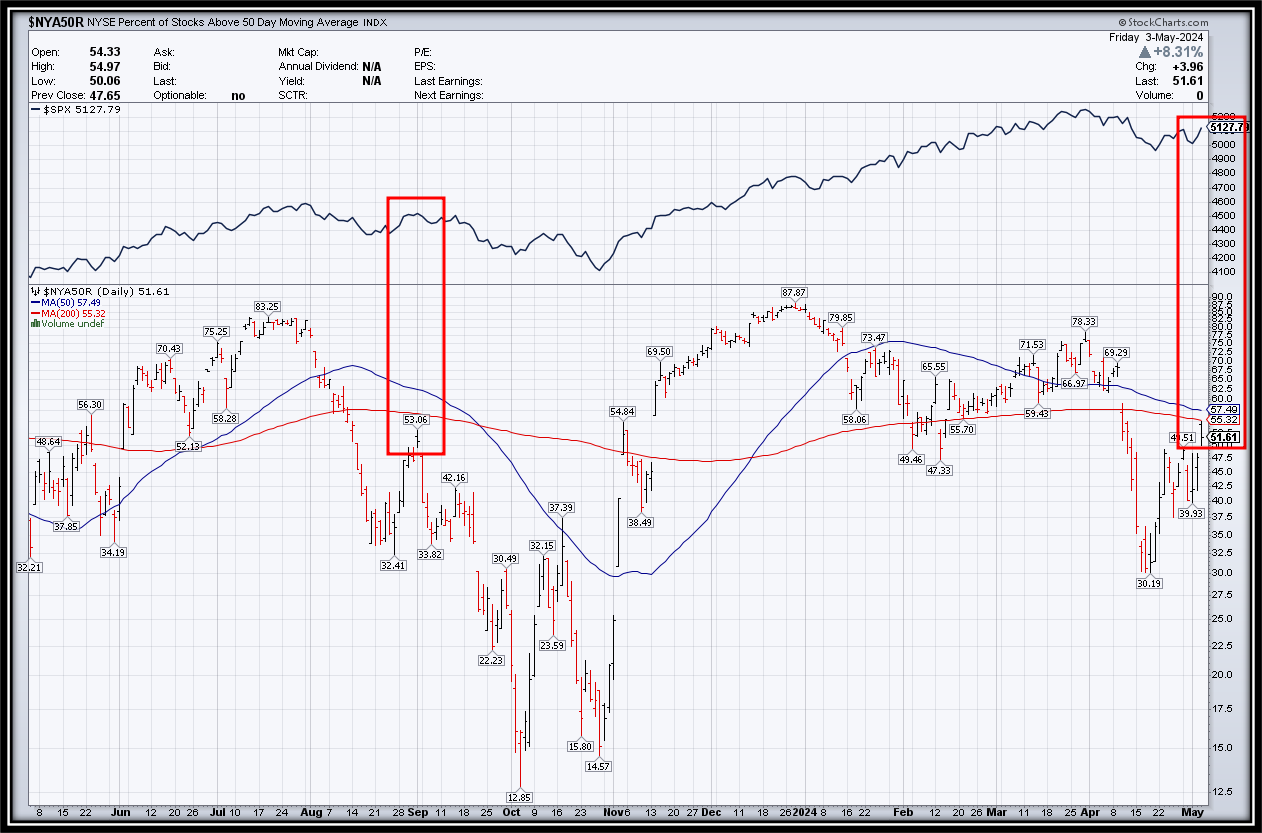

Oversold condition has been relieved on the critical advancing volume indicator.

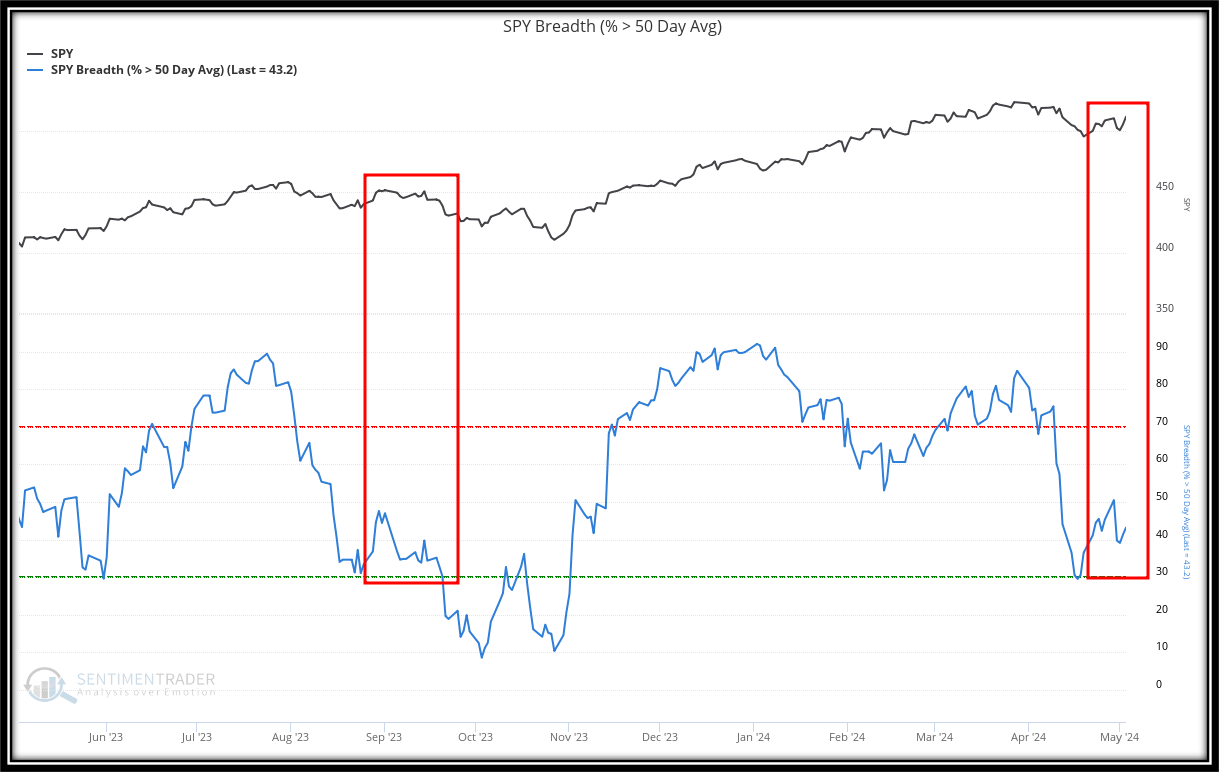

NYSE and SPY 50dma breadth behaving as one would expect mid-correction.

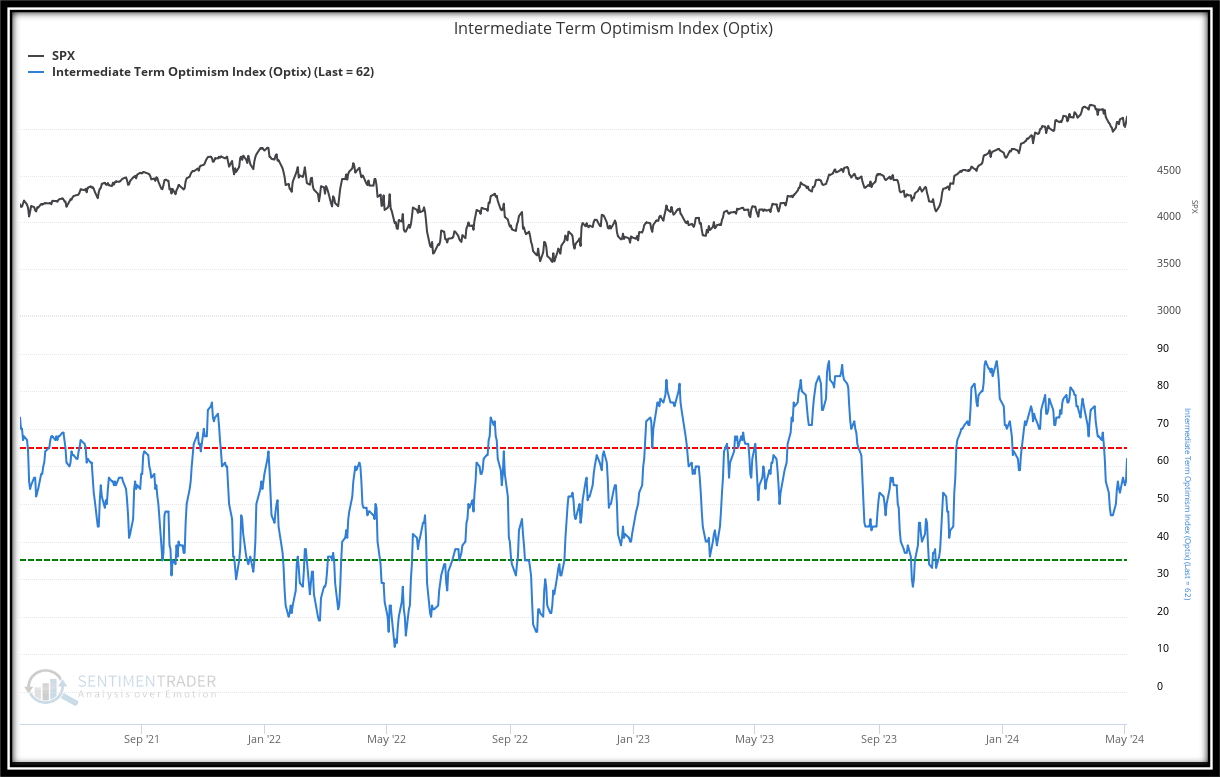

Medium-term sentiment has not fully flushed.

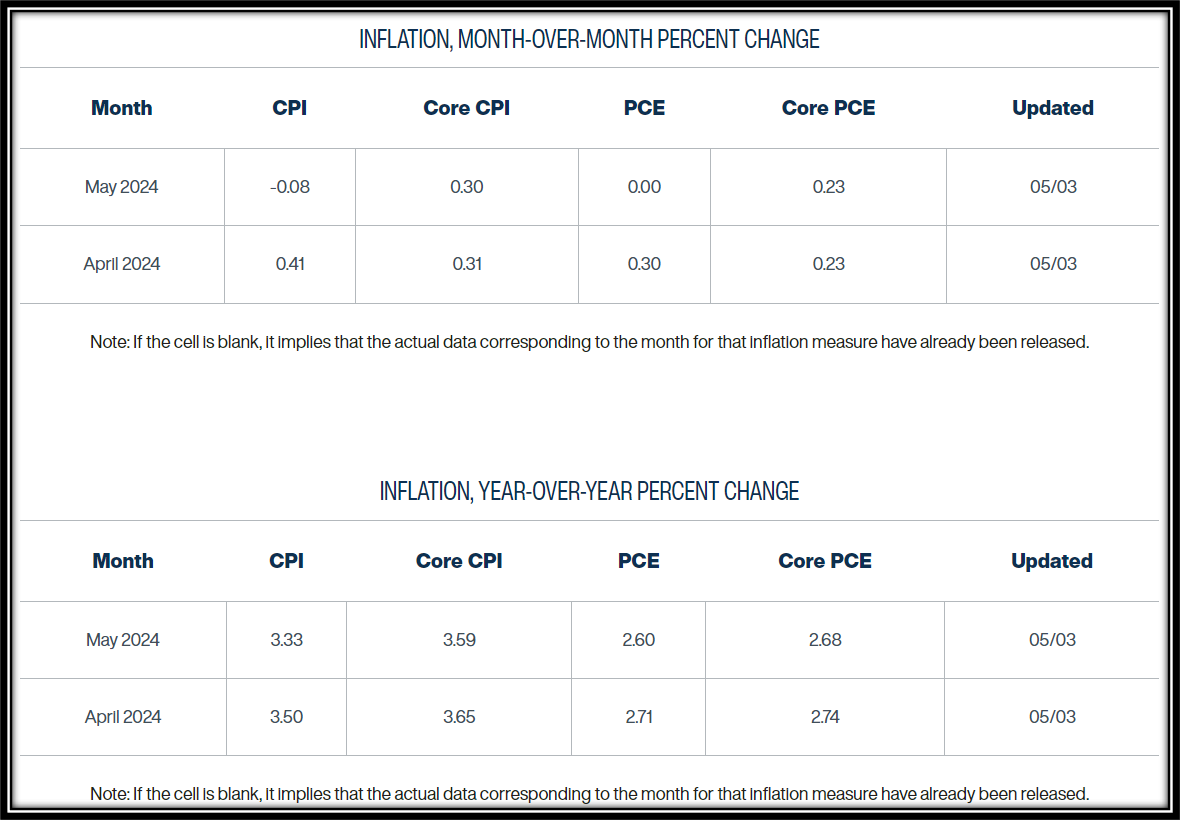

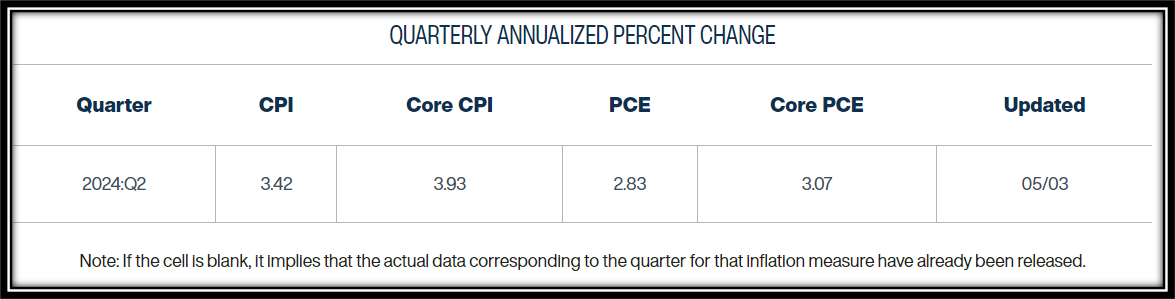

The April CPI report on May 15 is likely to act as a downside catalyst, per the FRB Cleveland inflation nowcast showing Core CPI and PCE inflation at 3.93% and 3.07% in 2Q24.

Upcoming inflation data are likely to act as a downside catalyst because the Fed provided important “tells” this week about its reaction function:

As discussed in the post below, in his post-FOMC press conference Chair Powell paused for five full seconds when asked if there was anything concerning in the Q1 inflation data. He and the FOMC know full well a second inflation wave is underway, but they want to contain the financial market fallout, so they’re going to downplay it as long as possible.

Also discussed in the post above, Powell evaded the question about whether rate hikes were discussed in the FOMC meeting. That looked intentional in real time, but if there was any doubt, FRB Chicago President Goolsbee removed it by evading the same question on Friday in the interview below.

Look for the release of May 1 FOMC minutes on May 22 to be a critically important market event ahead of the June 12 FOMC SEP release.

Portfolio Implication

With the US economy far from recession, the structural outlook for SPX remains bullish. So, with this downgrade of the cyclical outlook to “bearish”, the equity allocation called for in WOTE US 60/40 is 60%.

With the tactical outlook already bearish (last update here), the cyclical outlook downgrade to “bearish” means WOTE US Long/Short Equity is appropriately positioned -300% short.