The FED: Hawkish Eggs in a Dovish Nest

The FED: Hawkish Eggs in a Dovish Nest

May 2024 FOMC review.

Discussion

In my April 30 press conference preview (see summary below) I said that “buried inside the dove’s nest will be a handful of hawkish ‘eggs.’” This preview played out in spades, with Powell both more dovish and hawkish than I anticipated.

If you believe in “long transitory” inflation and that 1Q24 inflation data was simply a bump along a “sometimes bumpy path” back to 2% inflation, then you got everything you were looking for from Powell: he made a passing wave toward hawkish rhetoric in response to temporarily hot inflation data, but really, deep down, he’s a dove and will cut rates as soon as the data allow him later this year or once the labor market weakens.

On the other hand - if you do not believe in “long transitory” inflation, but rather that above-2% inflation is the result of excess demand driven by a constant stream of fiscal stimulus emanating from a persistent 5-10% of GDP fiscal deficit, and that Q1 inflation data was confirmation of a second inflation wave, you also got everything you were looking for from Powell: a passing wave toward dovish rhetoric so not to send financial markets into a tailspin, but really, deep down, he knows full well that he needs to engineer a higher unemployment rate to bring inflation well and truly back to 2%.

The bottom line? Powell is a 4D market chess master. He knows where the data are headed, but does not want to cause undo financial market volatility on the way to “sufficiently restrictive” financial conditions. But that’s just my opinion…

Let’s review the nest and the eggs (for reference, please see detailed press conference notes at the end of this write-up), and you can decide for yourself how the press conference shook out. To the extent you make it through this entirely too long analysis, please reach out to push back if you have a different view!

A Dovish Nest

QT Taper. First and foremost, the most dovish part of the meeting was the tapering of QT to a lower than expected rate of $25 billion/month. There was some expectation out there that the Fed would announce a taper to $30 billion starting immediately, so $25 billion in June is largely the same. But I think that’s a minority view. It’s clear the Fed is working hand-in-glove with Treasury to manage the UST market, and by coming in at $25 billion and under the market’s broad expectation, the Fed is sending a moderately dovish signal that it does not want the long end of the UST curve running away from current levels.

It’s clear the FEDeral Government Put is currently at work in FICC markets with the Fed dovishly surprising on QT, JPY down, and the UST curve today bull/bear steepening. Bitcoin is starting to confirm this with a sharp move higher. Tactically bearish equity market participants, myself included, need to be mindful of this. At this point, I believe there is a bit more going on here than meets the eye, and policymakers are likely foaming the runway for hot employment/inflation data to drive rates higher. But eyes wide open to how VOL, CDX, and breadth evolve from here.

Rate Hikes. As previewed by Nick Timiraos ahead of the press conference, Powell was peppered with questions about what it would take for the Fed to hike rates. In direct response to the second media member’s question Powell said in no uncertain terms that “It’s unlikely the next policy move is a hike.” That’s about as unequivocal as it gets, and Wall Street took the bait, as evidenced by Goldman’s interpretation of the presser (Hatzius’s team):

“The May FOMC meeting was mostly uneventful but dovish overall. While the Committee added a hawkish acknowledgment of the ‘lack of further progress’ on inflation so far this year to its statement, Chair Powell offered a dovish message in his press conference. We have left our forecast unchanged and continue to expect two rate cuts this year in July and November.

“The most notable aspect of the press conference was Powell’s strong pushback against the possibility of rate hikes. Powell said that he thinks it is ‘unlikely’ that the next policy rate move will be a hike, that he is confident that policy is restrictive, and that the FOMC would need to see evidence that policy is not sufficiently restrictive in order to hike and is not seeing that. He also said that if progress on inflation stalled, the FOMC would respond by holding off on rate cuts, suggesting that the bar to hike is high.

“Powell offered no major clues on the timing of a rate cut but struck a consistently dovish tone on inflation. Consistent with our views, he said he took little signal from the inflation uptick in Q1; highlighted the consistent progress on wage growth over the firmer Q1 employment cost index; noted that he did not see signs of reheating and that inflation expectations remain anchored; emphasized the ‘lag structures built into the inflation process’; expressed confidence that a decline in housing and continued supply-side healing would deliver further disinflationary dividends; and forecast that (sequential) inflation will move back down this year.”

Financial Conditions. Nick Timiraos asked Powell if he thought the reacceleration of growth and inflation in Q1 was the result of the easing of financial conditions since November. Powell said they’ll know more in time, but that he thought it was unlikely, given the fact Q1 underlying growth (i.e. private demand) was similar to 2H23 - in other words, there was no reacceleration.

Housing Inflation. Multiple times Powell stated that it’s just a matter of time before reported housing inflation catches up to softer real-time rental inflation.

Wage Inflation. Multiple times Powell said that the Fed does not target wage inflation, implying the Fed isn’t going to actively seek to weaken the labor market.

“Our Tools”. Lastly, Powell repeated the mantra he used throughout Q1: The Fed will use its tools to keep the labor market strong and inflation coming down to target.

Hawkish Eggs

#1: Opening Statement Change

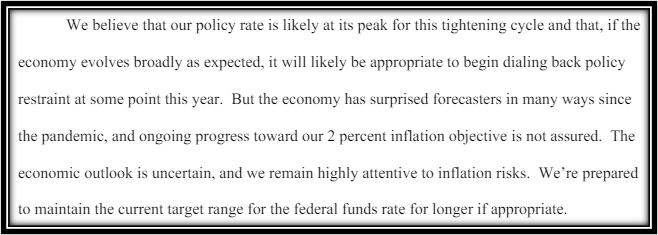

For all of the hand-wringing over the probability of rate hikes and what Powell said about it, Powell’s opening press conference statement literally dropped the sentence “we believe that our policy rate is likely at its peak for this tightening cycle” that was in the January and March statements. I’m no genius, but to my simple way of thinking, there seems to be signal in this change.

#2: The 5-Second Pause

In the clip below (minute 1:16:26 if it doesn’t automatically go there) Powell is asked about whether there were any worrying signs in the Q1 inflation data. He pauses for 5 very full seconds, looking up pondering how he should answer.

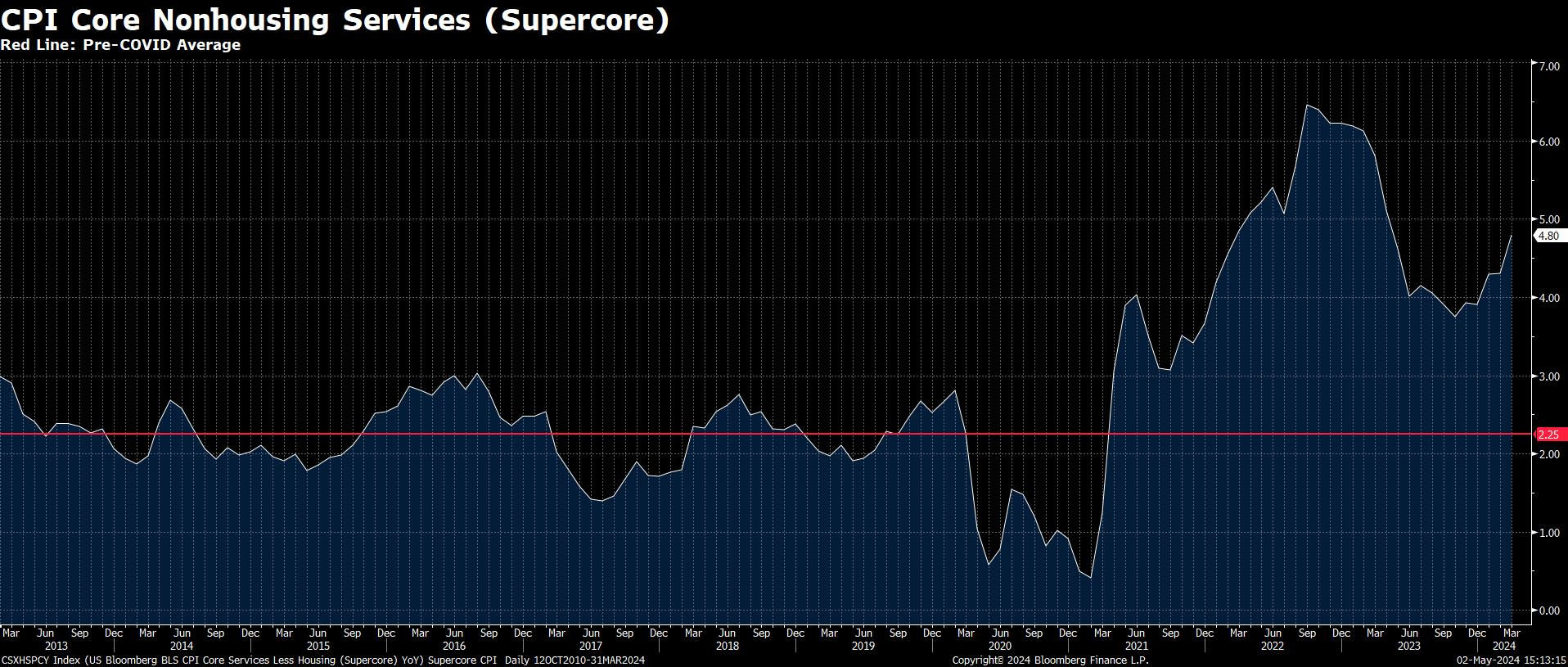

Again, I’m a simple person who looks for obvious answers. The 5-Second Pause could not be clearer of a signal to me, confirming what is obvious in the YoY CPI Supercore inflation data: a second inflation wave is underway. IMO, Powell knows this, but wants to slow-walk the market there so not to have anything disorderly happen along the way to a resumption of rate hikes later this year (or just higher long term UST rates in the meantime, which replace the need for additional rate hikes).

#s 3 & 4: Reiteration of the 2% Target and Rate Hike Discussion

Ed Lawrence of FOX (minute 1:27:45 below) really tried to pin Powell down on hikes, and out of that back-and-forth came two key hawkish ‘eggs’: 1) Powell reiterated that the Fed would not be at all satisfied with 3% inflation, a tacit reiteration of the 2% inflation target, but most importantly 2) Powell specifically evaded a follow-up question about whether rate hikes were discussed at the meeting.

Powell’s evasion of the question as a signal that rate hikes are on the table is bolstered by the fact Nick Timiraos followed up his normal post-FOMC review piece later last night with another piece about rate hikes, ending with the following:

For now, the Fed’s view that a rate cut is more likely than an increase “is a reasonable one,” said English. “I’m not inclined myself to think they should be raising rates today, but there is now a real possibility that the next move could be to the high side.”

#5: Financial Conditions

As discussed in the “dovish nest” section above, in response to Nick Timiraos’s question about financial conditions (FCI) Powell stated that he did not think easing FCI resulted in the Q1 reacceleration of growth and inflation. However, he responded with specificity to Timiraos’s second question about whether financial conditions would need to tighten in order to return inflation to the disinflationary trend it was on in 2H23:

In terms of tightening, you’re right, rates are certainly higher now, and have been for some time, than they were before the December meeting. That’s tighter financial conditions, and that’s appropriate given what inflation has done in the first quarter.

This tells me that the Fed is fine with the long end of the UST curve where it currently sits. But, combined with the fact QT was tapered by more than expected, my read is that they want rates to be driven by the data in an orderly fashion.

#6: Unemployment

Last, but far from least - in my press conference preview I said that Powell was likely to bring back the discussion about needing to engineer below-trend growth to get inflation back to 2%. He did not do that specifically, but late in the press conference he made a very important comment about tying rate hikes to rising unemployment (1:41:50 in the clip below).

I said an unexpected weakening [would warrant rate cuts]. It would have to be meaningful and get our attention. A couple of tenths in the unemployment rate probably wouldn’t do that. It would be a broader thing that would suggest it would be appropriate to consider cutting. Whether you decide to cut would depend on all the facts and circumstances, not just that one [the unemployment rate].

As highlighted by me in the quote above, not only does Powell emphasize the deterioration in labor would need to be “unexpected” - i.e. likely beyond the 4.1% projected in the March SEP - even that unexpected deterioration would not automatically lead to rate cuts. Rate cuts would be “considered”, but whether rates are cut would depend on the totality of the data.

Press Conference Notes

Question 1: Is the current policy rate sufficiently restrictive?

Policy is restrictive and weighing on demand as evidenced by labor market cooling (i.e. JOLTS reported the morning of May 1) and interest-sensitive spending

Follow-up question homed in on “sufficiently” restrictive and Powell said: “We believe it is restrictive and that over time it will be sufficiently restrictive. That will be a question the data will have to answer.”

Question 2: What change in conditions would merit a rate hike?

“It’s unlikely the next policy move is a hike.”

Current focus is how long to keep policy restrictive

To hike rates, would need to see “persuasive evidence that the current stance of policy is not sufficiently restrictive.”

My note: Critical to note that he read this answer

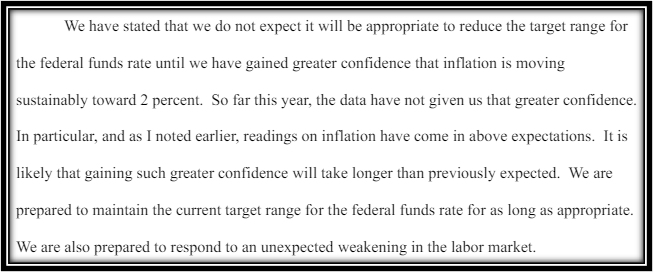

Question 3: The Fed no longer says Fed Funds is likely at a peak for this cycle. Has the Fed dropped its easing bias?

“If inflation proves more persistent than expected and goes sideways, while the labor market remains strong, that would be a case where it could be appropriate to hold off on rate cuts.”

Two paths to rate cuts would include gaining greater confidence inflation is on its way back to 2%, and another path would be an unexpected weakening in the labor market.

“As far as peak rate, the data will have to answer that question for us.”

Question 4: To what extent has the easing of financial conditions since November contributed to the reacceleration in growth? And do you now expect a period of sustained tighter financial conditions will be needed to resume the sort of disinflation the economy saw last year?

Hard to say - we’ll know more in time

1Q24 GDP growth was in line with 2H23, so hard to say easing FCI caused a reacceleration

My note: This is a sleight of hand by Powell. He knows full well that if the tight FCI last September/October was maintained into this year that the economy would have been materially weaker than it is today. OF COURSE the easing of FCI into 2024 reaccelerated activity…just from a lower projected base rate of growth than 2H23

“In terms of tightening, you’re right, rates are certainly higher now, and have been for some time, than they were before the December meeting. That’s tighter financial conditions, and that’s appropriate given what inflation has done in the first quarter.”

Follow-on question asked about needing to weaken the labor market, and Powell said that he would not give up on the idea that the economy could still experience what it did last year with growth and labor strong while inflation falls due to supply side healing.

Paraphrasing a lengthier statement from Powell: “We do not target wage inflation. We target price inflation. But part of the process of bringing inflation down will likely result in wage inflation coming down incrementally to levels consistent with 2% inflation.”

Question 5: You talked about needing time to develop confidence. It’s May already. Do you have time this year to cut 3 times given the calendar?

“I’m not really thinking of it that way.”

We don’t know when we will gain confidence, but when we do then rate cuts will come into focus

Question 6 (18:35): With the benefit of hindsight, were there any signs from the first quarter inflation data that suggested something more worrying than expected bumpiness?

Powell paused for 5 full seconds while he pondered this question.

“Not really.”

“We’re taking signal from the first quarter data.”

Question 7: What particular areas were temporary or blips in the inflation data in the first quarter, and what’s the dynamic by which you expect them to work out in the coming quarters?

We’ve put that under a microscope. But nothing is going to come out of that that will change the view we did not gain greater confidence

Higher goods inflation expected

Higher nonhousing services than expected

“My forecast is that we will see inflation move back down over the course of this year. My confidence in that is lower than it was because of the data that we’ve seen.”

Housing services inflation will come down over time, but there is a larger lag between real-time and reported data than previously thought

My note: 3Fourteen Research data shows that real-time housing inflation is picking back up. Powell obviously knows this, but is dovishly hedging.

Question 8: Has the probability of no cuts risen or stayed the same since first quarter inflation data? Is there an argument for being patient and working with the economic cycle to get inflation down over time while preserving jobs?

“I don’t have a probability estimate for you.”

“There are paths to cutting, there are paths to not cutting. It’s really going to depend on the data.”

“As inflation has come down to below 3% on a 12-month basis, the employment goal comes into focus.”

Question 9: It appears you believe the most likely path of inflation into the end of the year will allow for rates to be cut. It would be good if you could confirm that that’s the correct reading. Q1 GDP resulted in commentary about stagflation - do you or anyone else on the FOMC think this is a risk?

“I’m not dealing in likelihoods. I think there are paths the economy can take that would involve cuts, and there are paths that wouldn’t. And I don’t have great confidence in which of those paths. My personal forecast is that we will begin to see further progress. I don’t know if that it will be sufficient. I don’t know if it won’t.”

“I was around for stagflation of double-digit unemployment and high single-digit inflation. We don’t have that today.”

Question 10: Has potential growth moved up and therefore policy isn’t tight enough?

Didn’t answer the question, just talked about higher labor supply driving up potential growth and how that is not inflationary or disinflationary over time.

Question 11: If growth is up and you’re not considering rate increases, does that imply that you’re more worried about growth than inflation?

“No. We believe our policy stance is in a good place and is appropriate to the current situation. We believe it’s restrictive.”

Question 12 (29:55): It feels like the economy is in a steady-state and we have 3% inflation. If the data remain the same, it stands to reason that you’ll need a rate hike to get from 3% to 2%. Was there any discussion today about a rate hike? And are you satisfied with 3% inflation for the rest of the year?

“Of course, we’re not satisfied with 3% inflation. 3% can’t be in a sentence with satisfied. We will return inflation to 2% over time - over time. And we think our policy stance is appropriate to do that. If we were to conclude that our policy is not sufficiently restrictive to bring inflation sustainably down to 2%, then that would be what it take for us to increase rates. We don’t see that. We don’t see evidence for that.”

Follow-up question: “But in the discussion, was there a discussion about a rate hike at all?”

“The policy focus has been on holding the current level of restriction. That’s where the policy discussion was at the meeting.”

Follow-up question: “Is there a time frame on the persistence of inflation that would trigger a rate hike?”

“There isn’t any rule. It would be a judgment call. Clearly restrictive monetary policy needs more time to do its job. That is pretty clear based on what we’re seeing. How long that will take and how patient we should be, it’s going to depend on the totality of the data, how the outlook evolves.

Question 13: Does Election Day matter for policy? And is there a significant difference between cutting in September versus December?

It’s hard enough to get the economics right. If you start to mix in politics, where do you stop?

“There’s a significant difference between an institution that takes into account all sorts of political events, and one that doesn’t. We just don’t do that.”

Question 14: Wage growth hasn’t normalized. Why do you think that’s happened?

Wage growth has fallen from peak but is still roughly 1pp above pre-pandemic levels

“We don’t target wage growth, but in the long run if you have wage growth running above levels warranted by productivity then there will be inflationary pressures.”

Question 15: What would you say to consumers struggling with higher rates?

“The thing that hurts everyone, particular the lower income brackets, is inflation.”

Question 16: How do you explain the substantial lags in real-time housing data and reported inflation? And how confident are you that rents will be helpful on inflation in the coming months?

Market rents take years to get into the data

As long as market rents stay low, it will ultimately feed through to the reported data

Question 17: Divergent monetary policy around the world?

Biggest difference between the US and ROW is stronger economic growth.

“We’ll be careful as we approach the decision to cut rates.”

Question 18: Can inflation continue to fall without so-called “pain”?

The unwinding of supply-side distortions helped bring inflation down without a significant dislocation in the economy or labor market. And I’m not giving up on that continuing to play out. But we can’t be sure that’s what will happen, so we’re trying to use our tools in a way that keeps the economy strong while bringing inflation down.

Question 19 (43:52): If the unemployment rate were to tick up above 4%, but with inflation still above target, would that catch your attention?

“I said an unexpected weakening [would warrant rate cuts]. It would have to be meaningful and get our attention. A couple of tenths in the unemployment rate probably wouldn’t do that. It would be a broader thing that would suggest it would be appropriate to consider cutting. Whether you decide to cut would depend on all the facts and circumstances, not just that one [the unemployment rate].”

That was one of my “eggs”

did you see that he removed this phrase from his prepared remarks: "we believe that our policy rate is likely at its peak for this tightening cycle" at the beginning of the press conference? This is another bone to the hawks