WAM Strategy Note: US Core Equity

WAM Strategy Note: US Core Equity

An assessment of the RSP/XLI trade and whether continued underperformance is part of a new leg down or part of a durable bottoming process.

Disclaimer: For informational purposes only.

Please see here for more information about The Weight of the Evidence.

Discussion

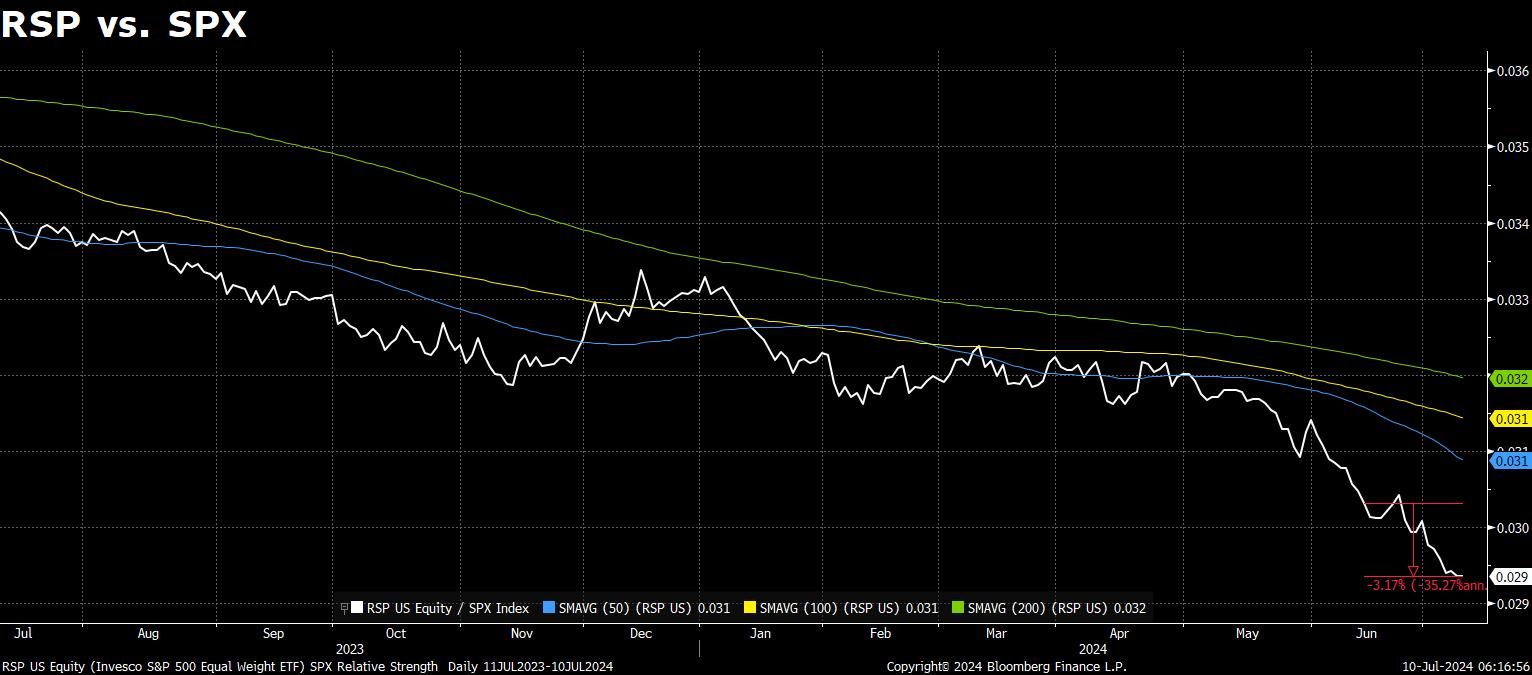

Since putting on the RSP/XLI position in my WOTE US Core Equity strategy on June 13 and June 14, RSP and XLI have underperformed SPX by more than -3%. The trade worked for a couple of days as Tech/Semis relative strength consolidated, but has since resumed its descent. Now the question is whether this is the start of yet another sizeable leg down to new lows or part of a durable bottoming process.

Analysis

Even if another leg down has begun, with non-Tech/Semis this oversold and the guts of the market gyrating wildly beneath the surface of placid equity indices there is highly likely to be an oversold bounce here soon that would allow me to stop out of the position.

My strong hunch is that this is a durable bottoming process that could take some time to play out. This is classic capitulative bottom price action…including my own psychology around it. Historically, I have had an extremely good knack for finding the bottoming zone across a wide range of situations. But I have had an equally good knack at talking myself out of holding positions through the entirety of the bottoming process, as I allow the choppy bottoming price action to influence my thinking. The fact I’m questioning myself here is a very, very good sign a durable bottom is at hand.

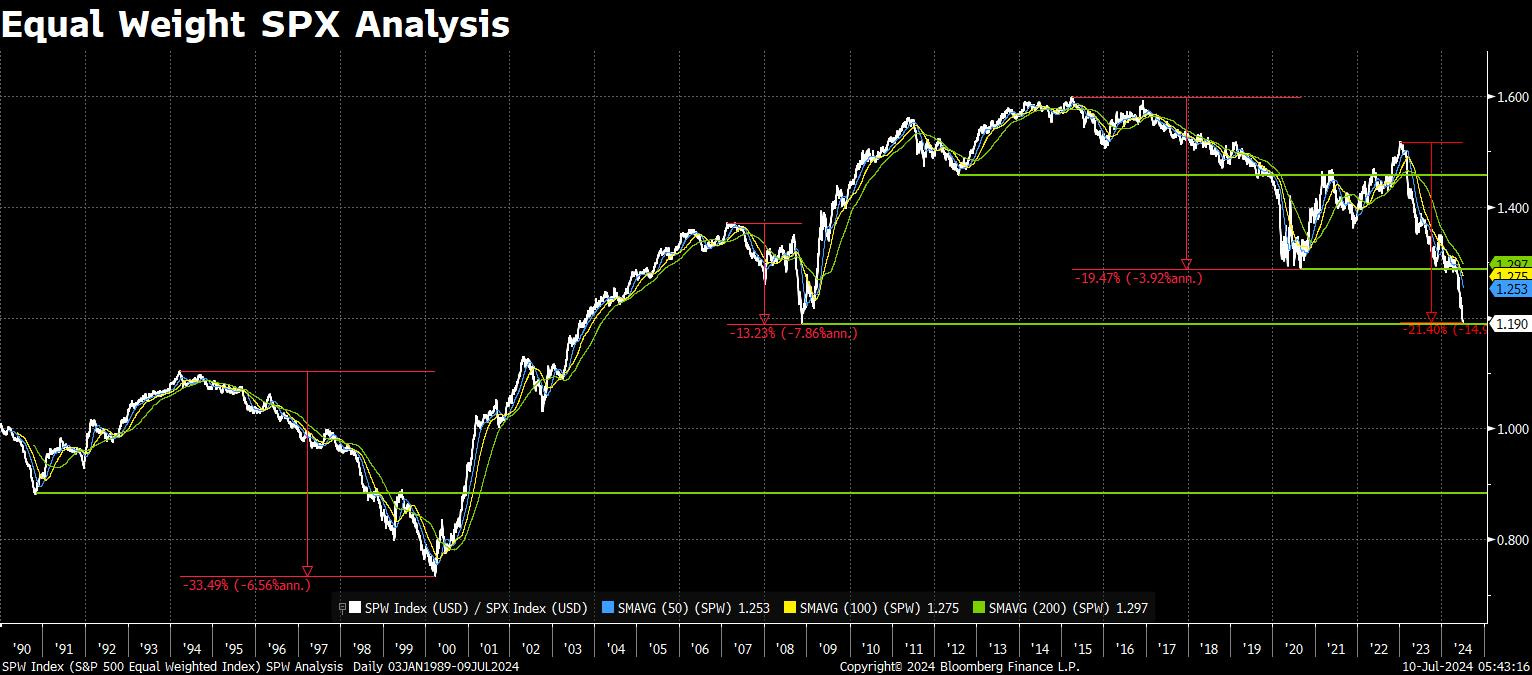

The bottom fell out of RSP once it broke 2020 relative strength support, and is now down -21% versus SPX since its peak in 2022, the second worst relative performance period since the 1994-2000 period. RSP now sits bang on 15-year support going all the way back to 2008/2009. It would not surprise me to see this support broken before all is said and done, but right here and now…

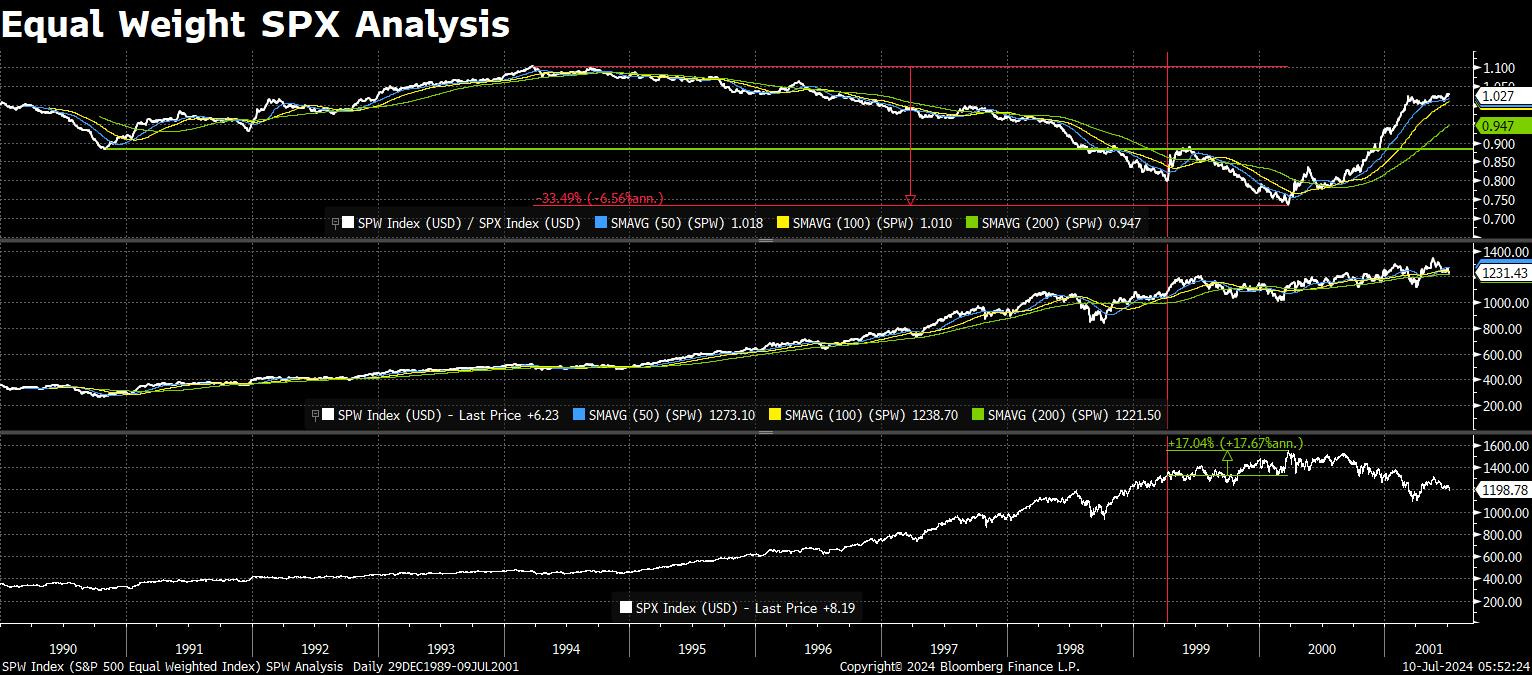

…I believe this current oversold condition is akin to the 1999 episode when the equal weight SPX (SPW) broke 1990 support, sold off hard, and then bounced back to test 1990 support before going down to make its ultimate low in early 2000. This episode stands out to me for two reasons: 1) As SPW broke 1990 support in early/mid-1999, the SPW itself held up well - it was the cap-weighted SPX that drove the underperformance (similar to today); 2) SPX still had room to run before reaching its cycle peak 17% higher from the early/mid-1999 SPW low…again, similar to today where the set-up is in place for SPX 6000+.

Lastly: On the Industrials front, equal weight Industrials vs. RSP is keeping me in this trade right now. While the cap weight is moving lower, the equal weight relationship has only very modestly broken support in a now-longstanding uptrend. This is not abnormal behavior for this sector (2017 is instructive), and more often than not it pays well to take the other side, even if only for a tactical trade. If and when RSP gets going to the upside in coming weeks/months, I think Industrials are highly likely to not only lead, but “surprise” everyone with their relative strength and lead the typical macro momentum strategists to upgrade their view of the sector…at which point I will be looking elsewhere.