The SPX Sector Report: November 21, 2023

The SPX Sector Report: November 21, 2023

Discussion

This report is focused on sector relative strength trends within the S&P 500, and it directly feeds the WOTE US 60 strategy, as discussed yesterday. The report will continue to evolve as I find more efficient and effective ways to weave it into my process, but for the most part it should look quite similar over time as I’ve been conducting this analysis outside The WOTE for some time now.

I break the analysis down into three groups - NDX, Cyclicals, and Defensives - and below are the summary conclusions of the analysis:

NDX Group. The bulk of the NDX group is running up against stiff overhead multi-year resistance, and with the dog piling into Tech running full steam ahead into the January/February blow-off top zone I am exercising caution in deploying fresh active share into this area. Software and cap weight Communication are the most interesting areas within the group that could be safely bought regardless of the outlook.

Cyclicals Group. Oncoming macro weakness is reflected broadly across the Cyclicals group. I am waiting for a durable bear market low in equities to form, or a decisive improvement in relative strength trends, before becoming aggressive in this area - though Banks could be interesting for a trade heading into 2024.

Defensives Group. Unlike the Cyclicals group, oncoming macro weakness has yet to be reflected in Defensives very likely as a result of the investment community viewing the NDX group as the preferred “defensive” soft landing play. I strongly suspect a hand-off will be made from NDX to Defensives in Q1 2024 as economic weakness becomes more obviously pronounced.

Relative Strength Analysis

NDX Group: Overhead Resistance & Selectivity

Stiff multi-year overhead resistance plagues most of Tech as the market dog piles into the best performing names into EOY. A decisive breakout above resistance followed by a successful retest of prior resistance would provide an all-clear sign for a continued run higher; but caution is demanded until then while selectively taking advantage of under-the-radar potential upside in Software and cap weight Communication.

Cap weight Tech, dominated by AAPL and MSFT, with a big breakout above summer resistance and consolidating all fall. But this is not a breakout to buy as everyone and their brother dog piles into Tech into EOY. The set-up heading into a January/February 2024 blow-off top in equities is to own everything but large cap Tech, most simply expressed via the SPX equal weight ETF RSP.

The fragility of the cap weight breakout is illustrated well by the rangebound relative strength of equal weight Tech.

NDX itself is battling over three years of relative strength resistance overhead. A breakout followed by a successful backtest or prior multi-year resistance would be an interesting set-up to explore, but patience is required to allow that set-up to play out into January/February 2024.

Semis have the best long-term fundamental story in the NDX Group, but like NDX itself it too is battling stiff multi-year overhead resistance.

Software and cap weight Communication have the best charts of the NDX group, still sitting well below the resistance dogging the rest of the group. Software would be attractive on a bit of a pullback while Communication is attractive here after consolidating its recent move to new highs.

And to round out the group, equal weight Communication remains a mess with a lot of work to become an attractive long candidate, while cap weight Discretionary (dominated by AMZN and TSLA) is in no man’s land.

Cyclicals Group: Macro Weakness

Broad macro weakness is reflected well across the Cyclicals group, with perhaps a buyable oversold condition developing in Financials/Banks as we head into a new trading year.

Industrials are perhaps a bit oversold in the short-term, but to make a durable bet on the space looking out 1-3+ months this chart needs to first move back above key moving average lines and then come back and retest those lines. Not there yet. And given what the Fed needs to do to bring inflation durably back to 2%, patience is hugely important.

Financials broadly, and Banks specifically, have been consolidating since SVB. Despite my bearish macro bias, I can’t help but think Financials/Banks rip in early 2024 for at least a trade.

Equal weight Discretionary is in hideously rough shape, trying to consolidate around the lows of 2022 while in a clear downtrend after making a series of lower highs. I want nothing to do with this area of the market until we get into the zone of a durable bear market trough in equities.

I’ve been surprised at Energy’s breakdown given the still-robust capital discipline and FCF generation from these entities, and frankly I think it speaks to the underlying weakness of the broader macro. Tough to be constructive on the space after a decisive failure at a lower high.

Materials look even worse, having underperformed for much of 2023. No interest here until a durable low in equities or relative strength reestablishes itself over key MAs.

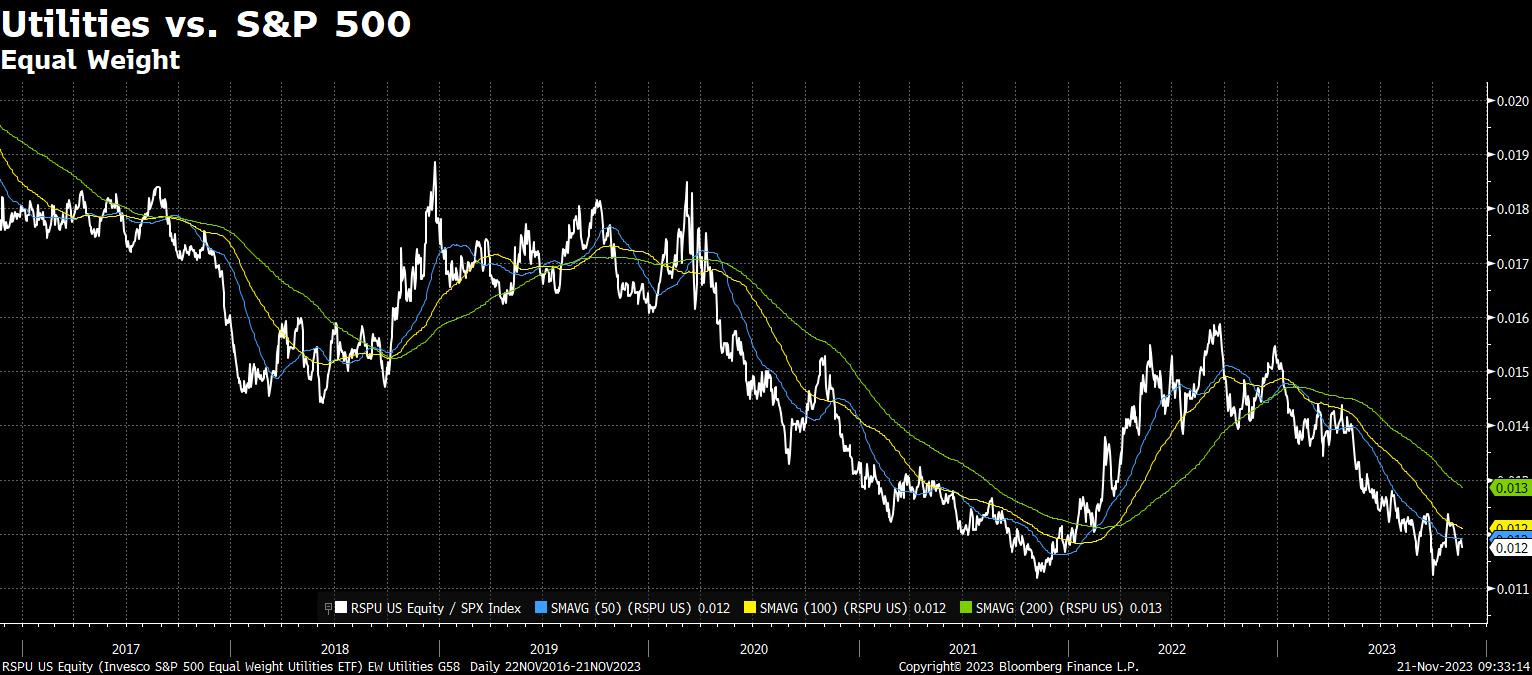

Defensives Group: Wen Defensive?

As discussed above, the Cyclicals group reflect oncoming macro weakness. But this oncoming weakness has yet to be reflected across the Defensives group of Healthcare, Staples, Utilities, and Real Estate (though to be fair, Real Estate is not a great defensive proxy in this cycle). My strong hunch is that the relative strength hand-off from the NDX Group to the Defensives Group will be made in Q1 2024 once economic weakness becomes more obviously pervasive, as reflected in the YoY rate of change in initial jobless claims moving decisively above 20%. For now, at most defensives should be averaged into as the market blows off into January/February, if not avoided altogether for the time being.

If the NDX Group does mean revert in 2024 as I suspect it will, I believe equal weight Healthcare will be the primary recipient of NDX $$$, as Tech and Healthcare tend to be viewed by Tech investors as two sides of the same coin - Tech for offense, Healthcare for defense.