The Market: S&P 500 Crash Watch

The Trapdoor

Discussion

What a start to the year. The S&P 500 has done almost everything in its power to lead investors to believe a new bull market is underway: cyclical sectors have outperformed defensive, credit spreads have tightened, key breadth thrust signals have fired, and, most critically, Fed Chair Jerome Powell appeared to endorse a new bull market in his February 1 press conference. But it’s a trapdoor:

The yield curve has not once moved out of inversion since the S&P 500 bottomed at 3492 on October 13. The historical record is clear: new bull markets are always accompanied by an easing of monetary policy, as indicated by an already-steep yield curve or a sharp steepening of the yield curve that more often than not takes it out of inversion.

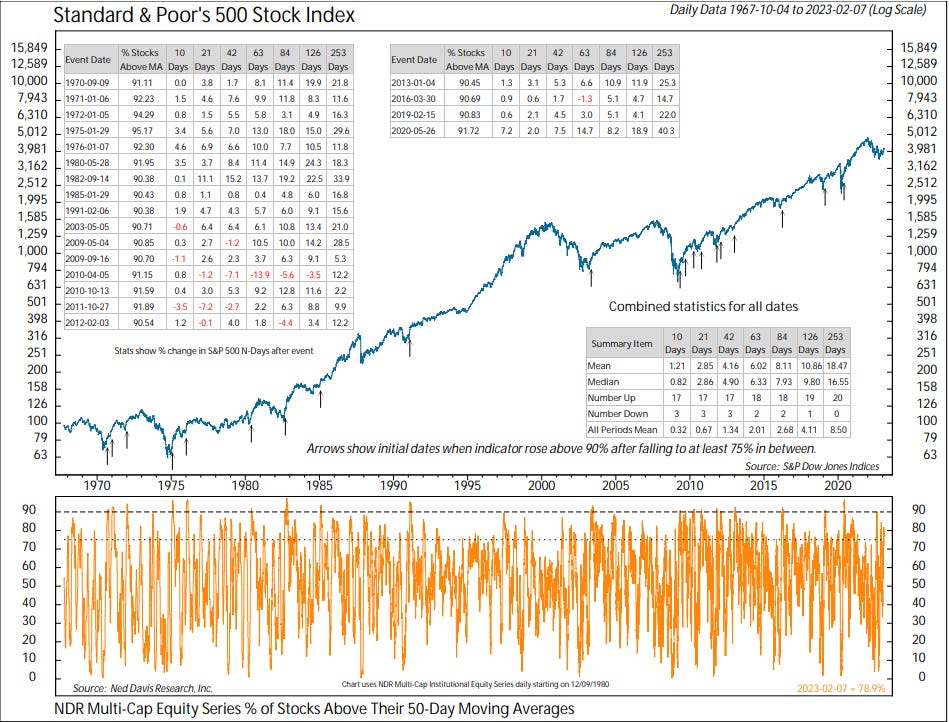

The % of stocks trading above their 50-day moving average has yet to breach the 90% “breadth thrust” threshold that has marked the end of all recessionary bear markets since 1970. Historically, the 50dma thrust signal takes about 3 months1 to trigger following a major market bottom. It’s been 4 months since the October 13 S&P 500 low, so not an unprecedented amount of time but it’s pushing it. Going back to the yield curve, it cannot be overstated how difficult it is for the equity market to reach escape velocity without monetary policy at its back. As recent example, two months prior to the October 13 SPX low the 50dma indicator reached 89%, just a hair under the 90% threshold. At the time, the 3y/10y US Treasury curve was over 110%, indicative of a still-hawkish Federal Reserve despite widespread market speculation of an impending “Fed pivot”. The set-up today is even worse: not only is the curve over 110%, but the 50dma indicator barely got above 80% in the January/February rally despite a raft of other breadth thrust signals.

The Fed’s war on inflation has entered a new and bloodier phase. Subsequent to Powell’s dovish presser conference on February 1, signs of reacceleration in economic growth and inflation data have not only led to a sharp repricing of the terminal Fed Funds Rate (FFR) in the Overnight Indexed Swaps (OIS) market, but also yet another “hawkish pivot” in Fed rhetoric. Despite one of the most aggressive rate hike cycles of all time, lingering thoughts that inflation might still be “transitory” have kept the Fed behind the curve for much of the last 12 months - backing off when financial markets get volatile, and ramping up when the data moves against them, all in an attempt to “gently” lower inflation without contracting the economy. But as evidenced by close Fed contact Larry Summer’s February 10 interview2 on Wall Street Week, it appears the Fed is settling in to the view that inflation is not transitory, a view that by definition (assuming the Fed is still committed to its 2% inflation target) requires the Fed to get ahead of the curve.

The next two sections explore how far and how fast the SPX could fall through the trapdoor.

Exhibits

The most basic “cyclical vs. defensive” sector relationship, Consumer Discretionary vs. Staples, has broken out.

The cost of credit protection, as measured by the High Yield CDX index, has fallen sharply.

And the key 10-day advance/decline breadth thrust signal has fired for the third time since this the S&P 500 peaked on January 4, 2022.

But the 3y/10y US Treasury curve has remained deeply and persistently inverted, a sharp repudiation of the bullish evidence above.

And the critical 50dma thrust signal has yet to fire.

Meanwhile, the OIS market’s estimate of the terminal FFR has risen sharply, to 520 basis points by July…

…up from 494 bps by June back in January. Most importantly, the OIS market’s estimate of the December FFR is almost 50 bps higher than it was in January, indicative of the market coming around to the view that persistent inflation will require the Fed to keep interest rates “higher for longer”.

The Floor

Key to framing the downside potential for the S&P 500 is the outlook for the US economy. Because we know that inflation is not “transitory” and thus requires a contraction in the economy to bring it back to 2%, as long as the Fed does not abandon its 2% target (which appears very unlikely) we can safely project that the US economy will start to contract sometime in the next 12 months3.

There have been 15 NBER4-defined recessions since 1929, and on average the SPX bottoms at a trough P/E of 9.4 times peak LTM EPS (as reported). For this cycle EPS peaked at $198 for the LTM ending 3/31/22, and applying the 9.4x average trough P/E yields a downside SPX target of 1861. This may seem too punitive, and it very well may be as it is heavily path dependent, but given what the Fed needs to do to bring inflation back to 2% it is very much in the cards.

For now, at minimum the SPX needs to fall to a valuation that more appropriately accounts for continued Fed tightening, recession, margin compression, and a generally higher cost of capital. As a rough framework, the upper end of the recessionary trough P/E dataset seems appropriate: in 1960, 2002, and 2020 the SPX troughed at a P/E of 15.2x, 14.3x, and 15.7x, the average of which is 15.1x.

15.1 times $198 peak LTM EPS = SPX 2990. Call it 3000 for easy math.

SPX 3000 is the floor.

The Crash

Discussion

Everything has lined up for a market crash by June 30:

Equity market sentiment has blown out to the upside and positioning is now elevated on hopes of a “Goldilocks” soft landing scenario, just as…

…the Fed went back on the warpath to re-tighten financial conditions5 in response to a reacceleration in economic data6.

Bond managers have called “time” on the credit spread tightening that has buoyed asset prices since last October.

CTA trend followers are positioned to aggressively sell down equity exposure if the market turns lower.

And most importantly, the post-options expiration window for broad market weakness opens around February 157, just as points 1-4 have coalesced.

It is a perfect storm. Perhaps one more rally attempt on a “lower than expected” CPI print on February 14, then the downside opens up.

But the downside potential doesn’t matter. What matters is the extreme asymmetry of the current market set-up.

The bottom line is this: Unless the Fed abandons its 2% inflation target, there is no durable upside to the S&P 500 from its February 2 peak of 4195.

The commonly cited case for equity market upside from here is a combination of China’s reopening, Europe’s warm winter, an end to the Russia-Ukraine war, and US disinflation boosting consumer confidence and real income serve to reaccelerate economic growth. But by definition a reacceleration in economic growth means inflation settles out above the Fed’s 2% target. So, unless the Fed abandons its 2% inflation target, a reacceleration is intolerable and thus demands an even higher terminal FFR held for even longer.

What’s incredible about the current market set-up is that even if bullish market participants get their bull case, it’s already accounted for with the SPX priced for perfection…into a deeply inverted curve, no less!!

At its February 2 peak of 4195 SPX traded for 21.2 times peak $198 peak LTM EPS (discussed above). If it holds, a 21.2x peak P/E would be the third highest pre-recessionary bear market peak on record going back to 1929 (and the SPX is already down -13% from its official ATH set on January 4, 2022). But here’s the problem: $198 EPS was generated on sales per share of $1616 for a net margin of 12.24%, 239 basis points higher than the 9.86% net margin at the pre-COVID EPS peak. At a 9.86% net margin the P/E rises to 26.4x, the second highest on record next to the 30.6x at the March 2000 peak, and one could argue that even 9.86% is too high given the outlook for persistently elevated cost pressures.

To close, the extreme asymmetry of the current SPX set-up is not unlike what Stan Druckenmiller described last September as a “one-way risk-reward bet” in regard to his famous British Pound short:

“30 years ago we shorted the Pound in the Quantum Fund. I didn’t know whether the pound was going to devalue. What I did know was, if they didn’t devalue in the next six months, my fund was going to lose 50 basis points; if they did devalue, I was going to make 2,000 basis points. So it was a 40-1 one-way risk-reward bet.”

Let’s go.

Exhibits

Sentiment has blown out to the upside.

Positioning is elevated.

And CTAs are primed to sell.

Risk Happens Fast: 2020 | -35% in 6 weeks

Risk Happens Fast: 2018 | -20% in 3 months

Risk Happens Fast: 2011 | -22% in 5 months

Risk Happens Fast: 2008 | -20% in 5 months

Risk Happens Fast: 2008 | -44% in 3 months

Risk Happens Fast: 1987 | -36% in 2 months

Risk Happens Fast: 1929 | -45% in 2 months

9/9/1970: 3.5 months off the low. 1/29/75: 4 months. 5/28/80: 2 months. 9/14/82: 1 month. 2/6/91: 4 months. 5/5/03: 7 months. 5/4/09: 2 months. 5/26/20: 2 months.

At 38:18 he says: “…the prospect that we are not on a trajectory now where inflation is going to get to the target level, and therefore this tightening cycle is not just about one more, two more, three more 25 basis point increases, but something more fundamental. That’s a substantial probability in this environment.”

NBER = National Bureau of Economic Research

See former NY FRB President Bill Dudley’s commentary on February 8 and Larry Summers’ commentary on February 10. (Because the Fed is a political institution, it relies on “unofficial” communication channels such as former Fed officials and others close to the Fed to communicate its true thinking.)