The Market: Internal Correction

The Market: Internal Correction

H4L Rates & Stocks policy means stocks can only correct internally to account for higher inflation and more hawkish monetary policy, while Yellen's liquidity bazooka supports indices. BTFD, soon.

Disclaimer: For informational purposes only.

Discussion

Back in April I started writing about the concept of FEDeral policymakers seeking to keep both interest rates and stocks prices high in order to combat inflation while keeping the labor market strong. I dubbed it “H4L Rates & Stocks” monetary policy. SPX went on to correct almost -7%, beyond the maximum -2.54% I believed FEDeral government policymakers would tolerate ahead of Election Day; but I do not believe I was as wrong as it appears, as the Israel-Iran conflict temporarily placed financial conditions outside of policymakers’ control.

The April correction in equities provided a critical window into policymakers’ thinking: Yellen sold a put via coordinated currency intervention, the Fed tapered QT by more than expected, and Yellen conducted an aggressive $243 billion TGA QE program from April 24 to May 24.

TIPS 30s are now back to the 240 level that stressed markets back in mid-April, yet SPX is barely off its ATH and IG CDX is below where it was in April with TIPS 30s at current levels.

SPOOZ should be down 2-3% today, at least, and IG CDX should be gapping higher. But they’re not. In short, H4L Rates & Stocks policy remains firmly in place, and will remain so until Election Day.

Breadth Thrust

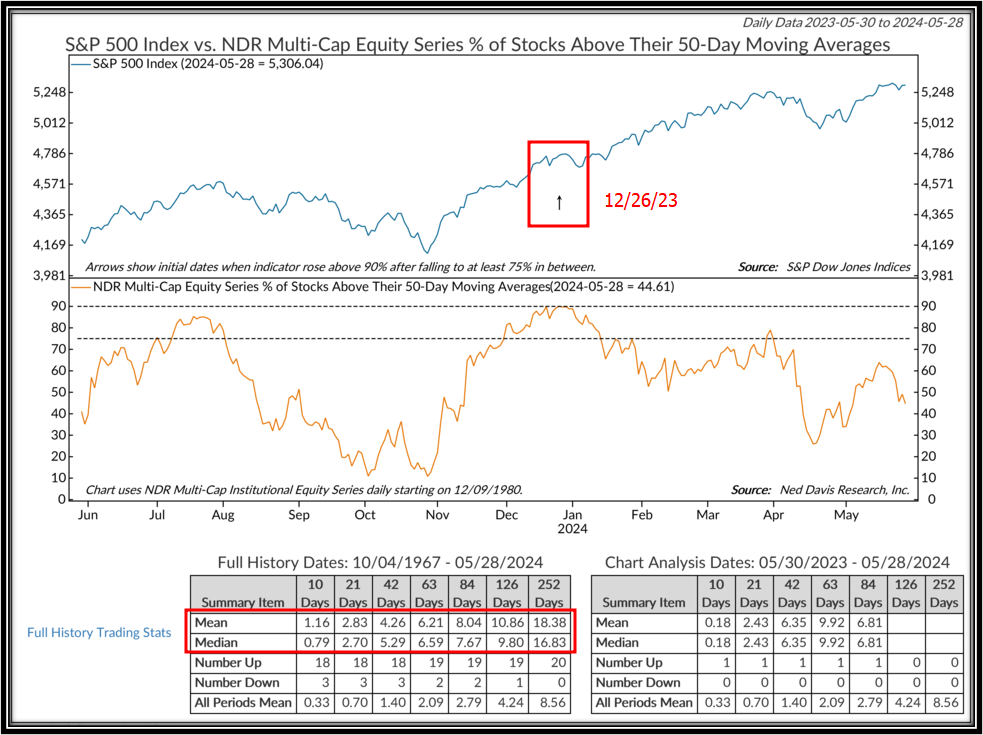

Last December 26 the % of US stocks above their 50dma breached the 90% level that has historically pointed to a 17.61% price-only gain in SPX over the NTM. From SPX 4775 on December 26, a 17.61% return implies SPX 5616 by December, 6% above SPX 5300.

This key breadth thrust signal continues to point the way higher for equities, and when combined with election year incentives for policymakers to keep asset prices elevated, the risk/reward for equities from here remains exceptional: at least 6% up versus at most -2.54% down, and very little volatility despite an exceptionally complicated macro backdrop (with today’s price action being case in point).

Yellen’s Liquidity Bazooka

With the case for a second inflation wave building by the day, the Fed laying the groundwork for rate hikes later this year (see here and here), and relative strength weakness proliferating across cyclical segments of the US equity market, one could be forgiven for taking umbrage at the statement above that the risk/reward for equities here is “exceptional”. But liquidity reigns supreme.

With a well-timed/targeted TGA QE program, Yellen ramped equities back to ATHs in a month. All it took was $243 billion (as discussed above). Even after a $243 billion QE program, with almost $700 billion sitting in the TGA and over $400 billion in the RRP Yellen still has $1.1 trillion left in her liquidity bazooka with just five months left to go to Election Day. That’s $220 billion/month.

Internal Correction

It would take a truly exogenous event (think: China invades Taiwan) for equities to fall through this $1.1 trillion liquidity floor between now and Election Day. What’s more likely to happen is what we’re seeing right now: the equity market corrects via internal rotation to account for rising inflation and more hawkish interest rate policy (I discussed this last week via The WOTE Quant).

The internal correction currently underway has resulted in a seemingly bearish divergence between headline equity prices and the % of NYSE stocks above their 50dma…

…But given the liquidity backdrop, much like the liquidity/policymaker-driven rallies of 2017 and 2021 this bearish divergence is best viewed as an internal correction that resets the overall market for more rallying in the coming weeks and months.

Portfolio Management

As discussed last week, I continue to sit in a neutral equity position in my 60/40 and Long/Short strategies as I wait for SPX’s 20/50dmas to catch up to the Index (currently $522/$516 and rising on SPY), a set-up that will likely support aggressive dip-buying as it did in 2017 and 2021. In my Core Equity strategy I am also at neutral, as I do not see the case for chasing this breakout in the NDX Group, nor playing contrarian in the Defensive and Cyclical groups; and in my FICC strategy I remain comfortably -100% buy & hold short UST 20s via the TBF ETF, as that is where I see the most asymmetry across the cross-asset market landscape today.