The Market: BTFD

The Market: BTFD

And quantitative thoughts on tomorrow's CPI report.

Discussion

The S&P 500 has corrected just -2.26% peak-to-trough since its April 1 high, but from an anecdotal read of broad market sentiment many if not most market participants believe the high is in for the year due to reaccelerating inflation, rising rates, and a liquidity squeeze from tax payments into the TGA.

This negativity toward equities has reset sentiment and positioned the market for new ATHs in the coming weeks (if not days, depending on how CPI is absorbed by the market and Yellen/Brainard manage the liquidity withdrawal from tax payments).

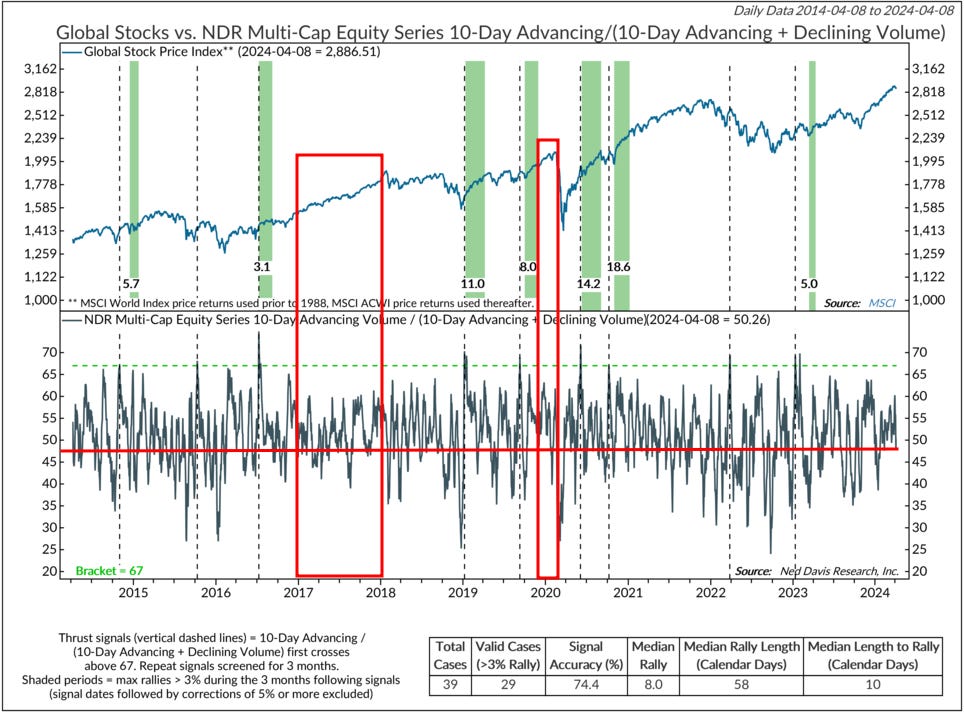

As illustrated in the chart below, strong market rallies tend to see sentiment make a series of lower highs alongside the rally as the market climbs the so-called “wall of worry”. As equities move to new heights that seems uncomfortable to market participants, it’s natural to doubt the sustainability of the rally - that is exactly what is going on here.

2017 and 2021 are great examples. Sentiment stair-stepped lower over the course of the rally before reaching overly pessimistic levels that launched the final rally to the peak of the bull market.

This market is still in the early stages of working sentiment lower, but before a new low in sentiment is reached I believe the broader weight of the cross-asset market evidence suggests another sharp leg higher is upon us.

For one, as SPX has stair-stepped lower this month, IG CDX has made a series of lower highs, and just today barely reacted to equity market weakness. This is a tell-tale sign of a market gearing up for a run higher.

Second, 10-day advancing volume as a % of total volume is right in the oversold zone that sets the market up for a fresh leg higher. The market could consolidate and move a bit lower here in the near-term, dragging this indicator down to even lower levels, but we are very close to the next up-leg here. However…

…Given SPX has already corrected -2.2% from its high - within the -2.54% range that Yellen/Brainard will allow, as discussed in The WOTE Report - it’s unlikely SPY will correct much below $513 before the next up-leg.

April 10 CPI Report

Tomorrow’s CPI is viewed as make or break for the rate cut psychology that has supposedly underpinned the equity market rally YTD. The thinking goes, if CPI comes in hot enough to validate the high readings of Jan/Feb, market sentiment will shift to “no cuts in 2024” and equities will enter the “inevitable” correction we have all been calling for this year.

I have been very clear that the “no landing” scenario we are currently in would result in no rate cuts this year and a resumption of hikes starting at the December FOMC meeting. We’re running a 5-10% of GDP fiscal deficit - no self-respecting market participant actually believes even an intrinsically dovish Powell will cut rates in this no-landing environment. But even with that said, I don’t think tomorrow’s report can be hot enough to shift the market conversation toward the hikes I believe are coming post-Election Day, which in my opinion is critical to catalyzing a 5-10% correction in equities. It’s too early, because…

…For all of the hype around the move up in commodities broadly and oil specifically, commodities are still in a downtrend and at best just starting to break out above their downward-sloping 200-day moving average. CPI is very likely going to be in a new YoY uptrend in the second half of this year, but based on the still-nascent rally in commodities, it’s too early for that YoY uptrend to commence from here. Commodities need to bottom out above the 200dma, the 200dma line needs to start moving back up, and then YoY CPI readings can accelerate to the upside.

Tomorrow’s report likely affirms the existence of the gap between rate cut hope and rate hike reality, allowing equities to resume their uptrend on the back of Yellen/Brainard liquidity, fiscal stimulus, and the international bid for US-based AI equity exposure.