"The Loop" - by Danny D of Macro Musings

"The Loop" - by Danny D of Macro Musings

Excellent overview by Danny Dayan of the financial conditions loop the US economy has been in since early 2022.

The Loop

I believe Danny Dayan is the only other financial market participant in my circle that believes it’s more likely that the next move by the FOMC is a rate hike. So, naturally I agree with his excellent analysis in the post below (I would also encourage folks to listen to his recent podcast - also below).

Discussion

I would add three things:

(1) This FCI loop is a feature, not a bug of the FOMC’s current battle with inflation. They are seeking to engineer a “soft landing”, so anytime the data look to be turning down they pivot in some fashion.

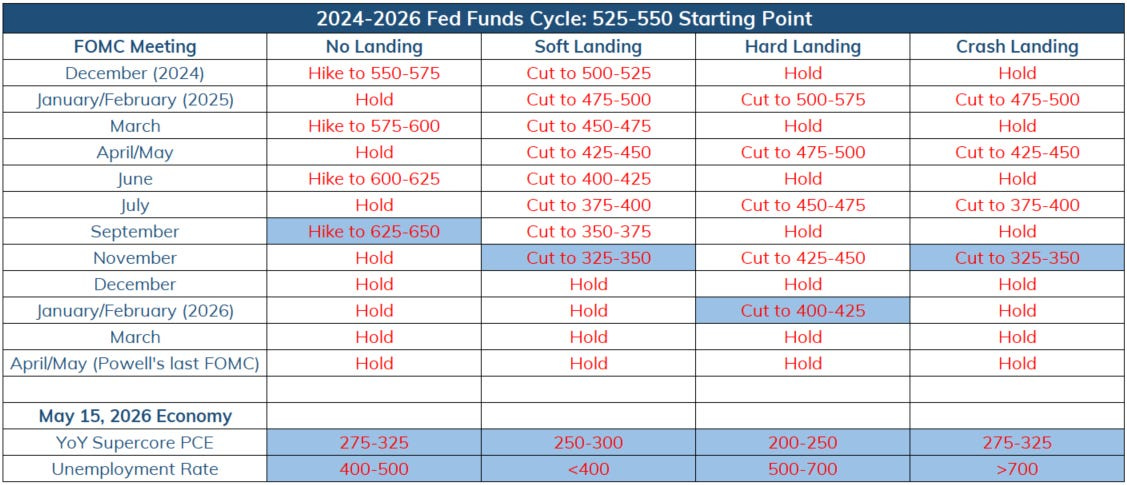

(2) If the Powell Fed truly believed inflation was “long transitory”, they would have started cutting by now. The fact they haven’t - despite their dovish management of FCI - says a lot about how seriously they take the risk of an Arthur Burns-like “stop & go” policy mistake. Powell’s term as Chair is up in May 2026 - odds are high he will ditch the soft landing attempt in 2025 in an effort to bring inflation durably back to 2% ahead of his May 15, 2026 due date. This depends on the path of inflation, which brings me to point #3.

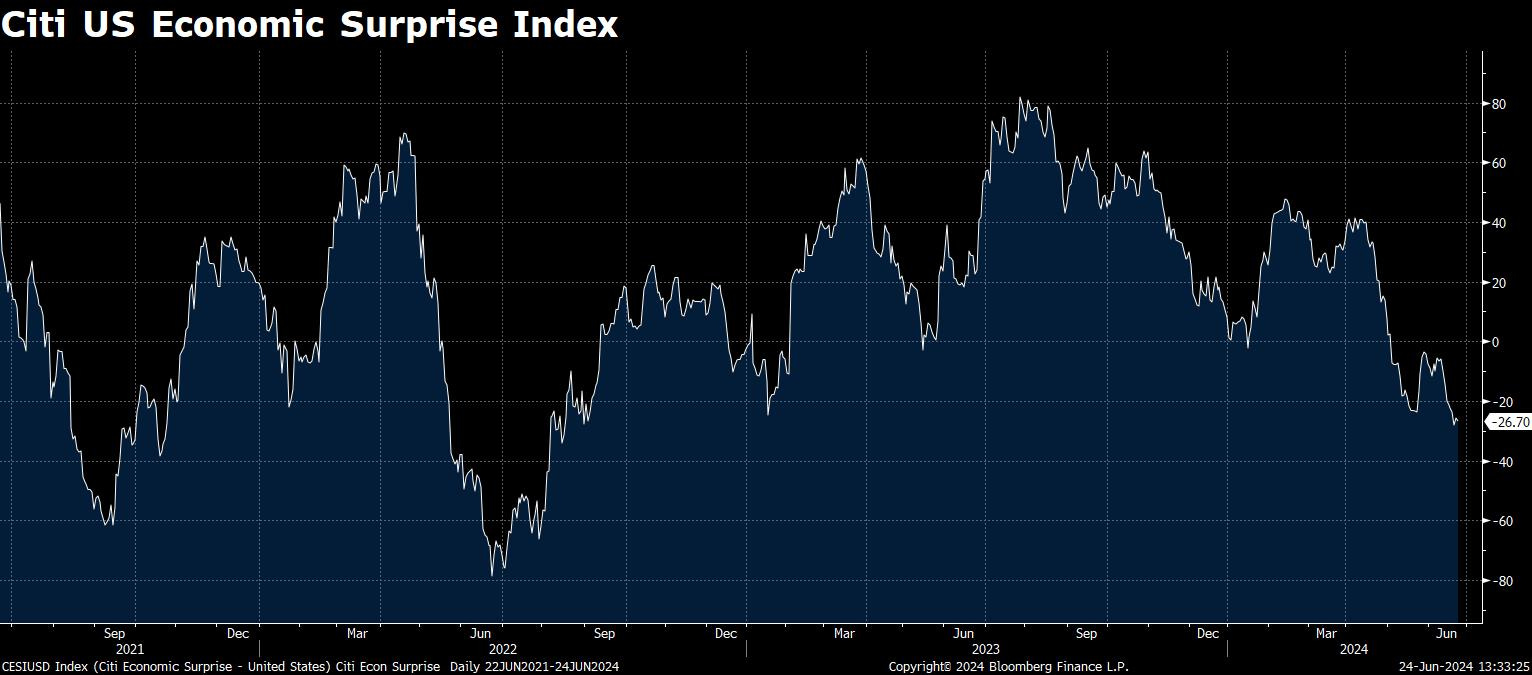

(3) Danny ends his piece asking the question of whether this latest FCI easing will lead to yet another acceleration in growth and inflation. As Druckenmiller likes to say, the “guts of the stock market” is the best economist. Right now, the three key macro pairs (Discretionary vs. Staples, Transports vs. Utilities, Banks vs. Utilities) in the aggregate point firmly against a sustained downtrend in economic activity, with the Discretionary vs. Staples pair pointing rather decisively toward a reacceleration, at least in data prints versus expectations with the Citi US Economic Surprise Index quite low here. As such, it is this analyst’s belief that the growth and inflation data are likely to be in the process of reaccelerating right into the key December FOMC meeting, a constellation of inputs that will lead the FOMC to resume rate hikes.

Exhibits

Key Macro Pairs vs. Low Expectations

Projected Fed Funds Cycle