The FED: Kashkari Goes Full Volcker

The FED: Kashkari Goes Full Volcker

In an interview at Milken, FRB Minneapolis President Neel Kashkari lowers the bar for rate hikes, tells market participants to "Sell All Assets", and raises the unemployment rate bar for cuts.

Discussion

Long-time followers of The WOTE will know how closely I have followed Kashkari since the Fed’s tightening program began in earnest in early 2022. People have regularly challenged me on following Kashkari, as he is often viewed as a political actor, but I think my view that he is far and away the most data-dependent FOMC member has been proven correct in spades over this tightening cycle. No need to go into detail about that view here now, but suffice it to say, starting with his first essay in May 2022 focusing on TIPS 10s as the key policy tool for reining in inflation, he has been a guiding light for where FED policy is headed, regardless of Chair Powell’s 4D chess match with financial markets at each press conference.

Today at Milken, Kashkari reiterated exactly what Powell said, but per usual did so with more specificity than the Chair did, since if Powell went into excessive detail about where policy is headed financial markets would become too unhinged for the Fed’s comfort.

Let’s dive in.

Three Scenarios for Policy

Base Case: Higher for Longer

I think the most likely scenario is where we are right now - we stay put for an extended period of time until we get clarity on is disinflation in fact continuing, or has it in fact stalled out. I don’t think we know the answer to that, so I would say the most likely scenario is we sit here for an extended period of time.

The Case for Cuts

If disinflation starts to come again, and inflation starts to tick back down, or we saw some weakening, marked weakening in the labor market, then that might lead us to cut back on interest rates.

The Case for Hikes

Or, if we got convinced, eventually, that inflation is embedded or entrenched now at 3% and that we need to go higher, we would do that if we needed to. I think that’s not my most likely scenario, but I also can’t rule it out.

Kashkari’s guidance on the need for hikes if inflation becomes embedded at 3% is brand new specificity from the Fed, and it is VERY MUCH intentional. In the press conference last week, Powell was unequivocal about the fact the Fed will not tolerate structural 3% inflation - but he did even come close to tying rate hikes to that scenario.

I’m just beating a dead horse here, but WE ALL KNOW that inflation is stuck at 3%. The Fed knows inflation is stuck at 3%. They’re just going to continue playing this game of slow-walking markets to the inevitability of higher rates (whether that’s through a higher Fed Funds or higher long-term UST rates is really the debate).

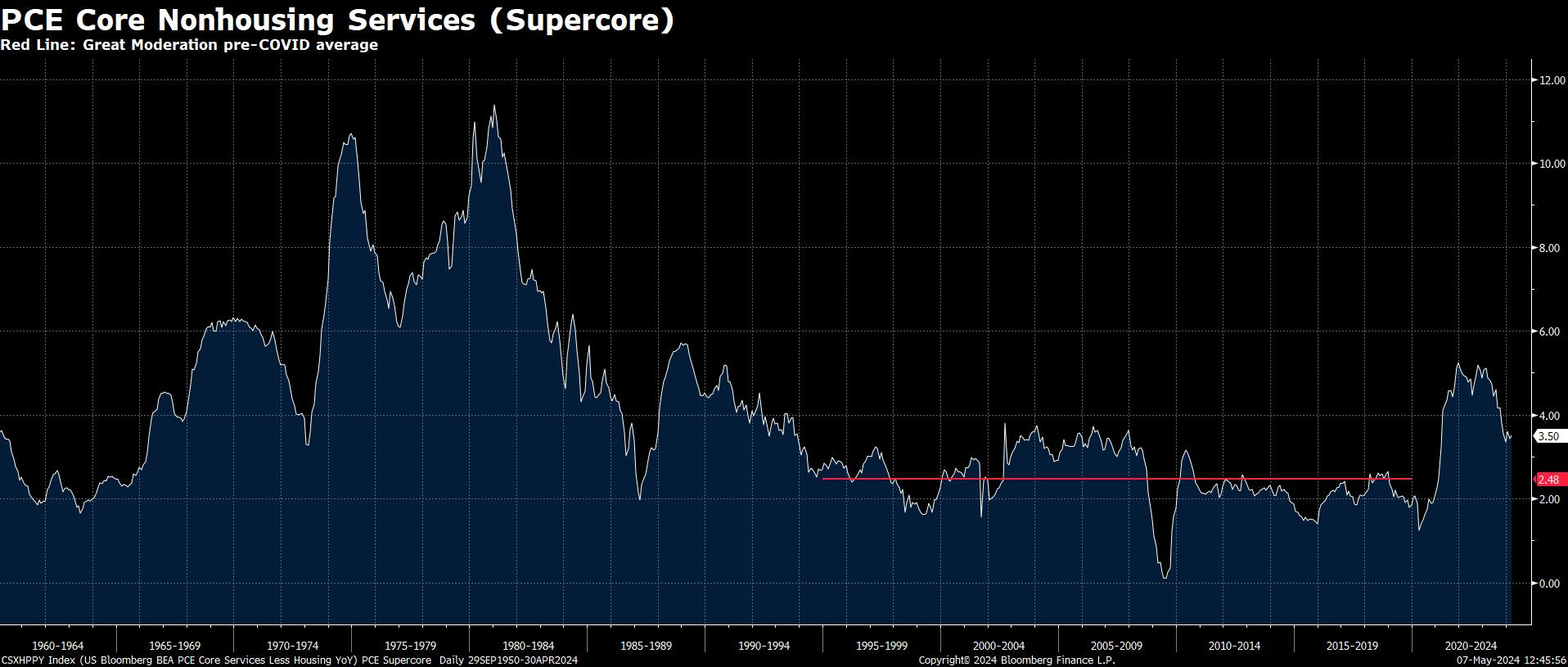

Last August, FRB San Francisco President Mary Daly specifically noted that the Fed would not cut rates until “supercore” inflation is back to pre-pandemic levels. Not only is supercore inflation not back to those levels, it’s reaccelerating - less so on a PCE basis, but decisively so on a CPI basis. Inflation is stuck at 3%, bottom line.

The Housing “Tell”

After outlining the three scenarios for FED policy, Kashkari was then asked what signals he would look for to conclude that the rate hike scenario is most likely.

One is of course the actual inflation data. I think we’re all appropriately data dependent. We have different outlooks for where the economy might be going, but we’re all very focused on what the actual inflation data is telling us. So, first and foremost what’s happening to inflation.

We have a dual mandate, of course. What’s happening to the labor market. The jobs report on Friday was a little bit softer than expected, but not a soft job report.

One of the things I’m looking at is the housing market. I’m looking at new leases. We know there’ s a mathematical relationship between new lease rates and then over the course of the next year or two those roll over into actual inflation data, housing inflation data. Curiously, the new lease rates seem to have ticked up in the last month or two. That’s a little bit concerning to me. I wonder why that is? If we’re putting so much downward pressure on real estate, why are new lease rates ticking up right now? That’s a place that I’m focused on.

I’ve noted in recent FED write-ups that 3Fourteen Research’s work on housing inflation suggests it is picking back up, but only recently did founder Warren Pies make the data public via his X account. Again, in his press conference last week Chair Powell went into an awkwardly long diatribe about how the lags in housing data are longer than originally thought, but he never said anything about housing inflation ticking back up. Enter: Kashkari. He noted precisely what 3Fourteen recently flagged. No bueno.

On the Other Hand

What I outlined above were clearly the key signals the Fed wanted to send to the market through Kashkari. But the doves in the audience also have takeaways from the interview that suggest the bar for hikes is higher than implied by the signals discussed above:

Kashkari said his June SEP won’t have more than 2 rate cuts but could have 0. One could argue that this is dovish because he’s still contemplating cuts with inflation embedded at 3%.

He then went into some history of the Volcker tightening regime, where it took a few years for the mortgage rate embedded in the economy to rise in response to higher rates. So, perhaps the Fed can just sit at the current policy rate until rates finally bite.

He also says monetary policy is weighing on the economy, as evidenced by rising delinquency rates, but just not overall as much as he thought it would have ex ante.

And he reiterates the “art” of monetary policy is bringing inflation down to 2% while preserving labor market strength.

Sell All Assets

Andy Constan of Damped Spring often illustrates on X when it’s time to “sell all assets” - toward the end of his interview at Milken Kashkari all but said to market participants: “Sell All Assets” in response to a question about financial conditions.

One of the transmission mechanisms of monetary policy is through financial markets. And financial markets are so wired for exuberance. You know, I look at this: you have three negative inflation prints in a row, and markets started to take that on board and get a little bit concerned. And then you had one somewhat positive jobs report and it’s back to the races again - exuberance has returned. That’s a pretty strong disposition to exuberance in financial markets. So that does give me concern.

And again, what are the financial markets telling us about the stance of monetary policy? If the financial markets are this exuberant, are they behaving in a manner consistent with monetary policy that is tamping down demand in the economy? That’s a little bit of a head scratcher.

He then goes on to say that perhaps the Fed itself is keeping financial markets’ view of the neutral rate low by projecting too low of a neutral rate.

Ignore the green on your screens today: This is exceedingly hawkish FED guidance.

The Dual Mandate

My gosh. I’m typing this write-up out as I watch the interview, and I can’t keep up with the hawkishness.

Kashkari caveats this with “this isn’t necessarily how we think about it,” but when asked about the dual mandate he says that a case could be made that with inflation at 3% and thus 50% off its 2% objective, policy wouldn’t come into balance until the unemployment rate is at 6% and 50% above a 4% objective.

WOW. Of course, Powell will NEVER say that. But Kashkari’s very specific guidance was no accident.

Follow-On Milken Interview

After the fireside chat discussed above earlier this afternoon, Kashkari sat down with Bloomberg for a follow-on interview. He repeated, verbatim, the message to financial market participants: Sell All Assets. But not only that…

He bemoaned the fact high rates are hurting the lower income segment of the economy while Wall Street booms at the first sign of favorable data.

And he failed to answer definitively whether the Fed should have continued hiking last year.

This is August 2022-style pushback against financial markets. Trade accordingly.