The Fed: Back to Basics

The Fed: Back to Basics

While the path for the economy and S&P 500 is unclear, an analysis of ‘first principles’ suggests the ultimate destination of Fed policy, and therefore the economy and S&P 500, is quite clear.

Discussion

On Friday January 20, in the last Fed appearance before the Fed’s self-induced official blackout period ahead of the January 31-February 1 FOMC meeting, Governor Christopher Waller had the following to say in response to a question about what he would need to see to start cutting interest rates:

“If the market’s view of inflation comes true - this very rapid disinflation - that’s great news. I’m happy for that. My concern is that we have to guard against in six months it looks great, then something takes off. Then we would have to raising rates again if we were thinking about starting to cut. That’s a thing we can’t do. So, this risk management idea where we have to guard against the upside risk of inflation jumping up ties us to staying higher for longer than the market would typically want you to do. So, that’s the best explanation I can say.”

Max hawkish right? Validation of The WOTE1 thesis that the Fed is laser-focused on avoiding the Burns Fed “stop and go” policy error of the 1970s, right? Not so fast. Waller immediately followed up with:

“We’ve got to wait and see through the summer how inflation is going. If the markets are right, and inflation is coming down, wages are falling into line, that’s great news. I’ve got no problem saying ‘you know, we should think about changing policy.’”

In the mind of a stock market addicted to the drug of easy Fed policy, that last sentence was just another hit. Waller is widely known to speak on behalf of Powell, so the appearance of opening the door to 2H23 rate cuts was viewed as Powell winking at the market that he really has its back and it’s just a matter of time before he “pivots”.

This weekend The WOTE posited that perhaps Powell no longer cares about keeping financial conditions tight because he is sufficiently confident that inflation and wage growth are headed back down to target. But after subsequently zooming out and getting ‘back to basics’, that thesis doesn’t hold water from a strategic nor a tactical perspective. This post focuses on the strategic reasons why the Fed’s inflation fight is far from over, but tactically, Powell allowing financial conditions ease doesn’t add up, just a month after explicitly stating in the post-December FOMC meeting press conference that “…it is important that, over time, they [financial conditions] reflect the policy restraint that we are putting in place to return inflation to 2 percent.”

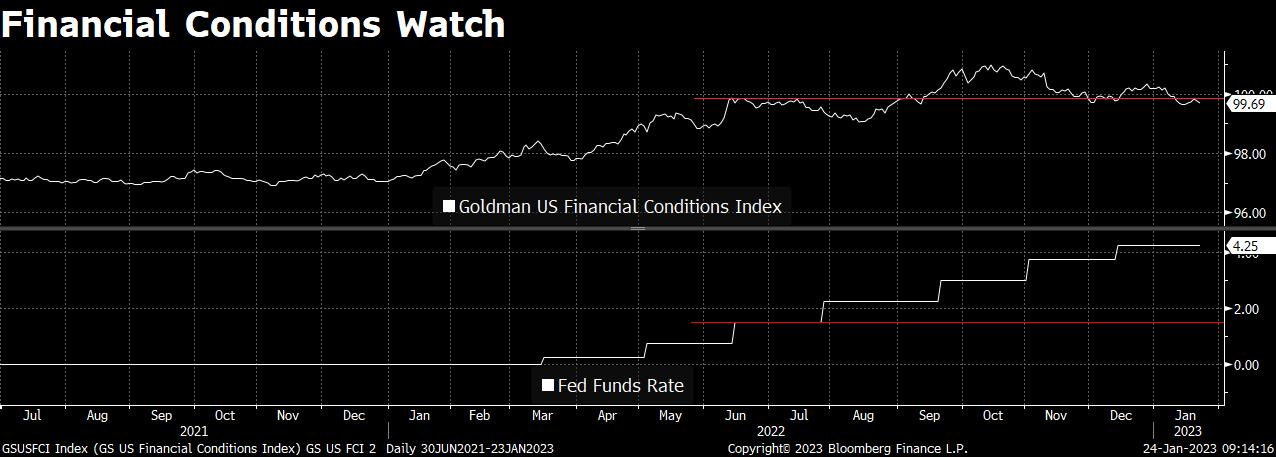

The Goldman Sachs US Financial Conditions Index is just one of many such indicators, but directionally it demonstrates just how out of line financial conditions are with the “policy restraint” that has been put in place. The Index is now below the mid-June 2022 highs despite the Fed hiking its policy rate by 275 basis points since then.

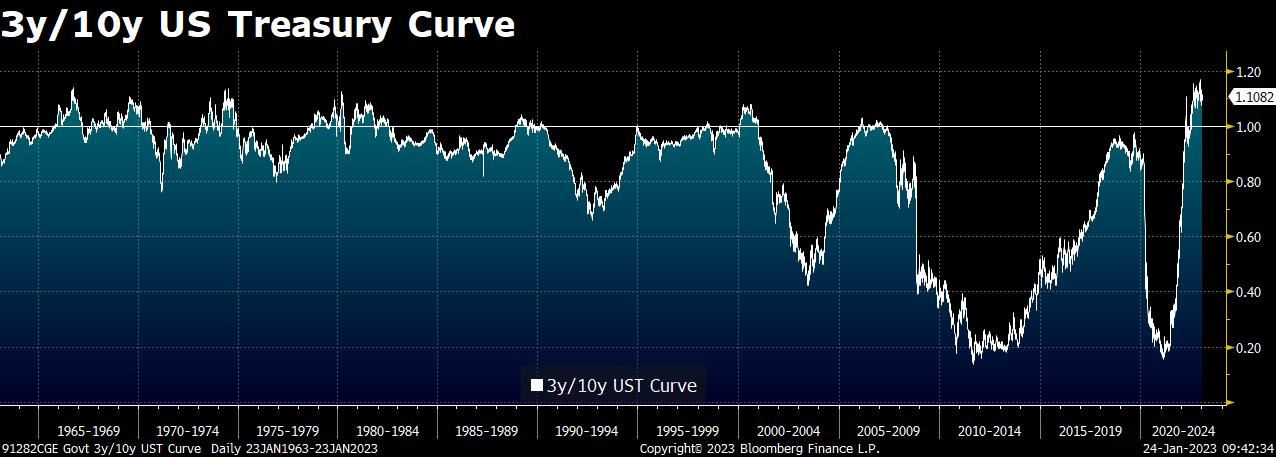

The WOTE thesis is that Waller’s rate cut comments were not intended to be dovish, as evidenced by his heavy emphasis throughout the interview on the Fed keeping rates higher for longer for “risk management” purposes and the Fed’s concerted effort since the beginning of the year to reinforce its intention to continue its Quantitative Tightening program well into the future. The Fed wants tighter financial conditions, and tighter financial conditions they will get. Don’t believe The WOTE? Believe the curve.

Don’t fight the Fed.

Now, let’s zoom out and get back to the basics of what will determine the ultimate destination of Fed policy, and in turn the economy and S&P 500.

Back to Basics

First Principles

Inflation is not transitory. It is the result of far too much demand created by the potent mix of aggressive fiscal and monetary policy in response to the COVID-19 pandemic. Therefore,

Demand must be destroyed via an economic contraction (i.e. recession) to bring inflation back to 2%. The question is: Does the Federal Reserve have the resolve to contract the economy enough for long enough to bring inflation back to 2%?

Federal Reserve Chair Jerome Powell’s legacy is on the line, therefore he will lead the Fed to contract the economy enough for long enough to bring inflation back to 2%. Powell’s words and actions strongly suggest that he is ruthlessly committed to not repeating the mistakes of the Burns Fed in the 1970s. It is no accident that an oft-repeated line of his is “we will keep at it until the job is done” - straight from the title of former Fed Chair Paul Volcker’s book “Keeping At It”.

More on this in a bit.

The Destination

If the economic destination was a “soft landing” - where inflation disinflates back to the Fed’s 2% target while the economy keeps growing and corporate margins remain high - the S&P 500 is arguably in the early stages of a new bull market. But the soft landing destination, by definition, requires inflation to be “transitory”: As the effects of the COVID-19 pandemic and the Russia-Ukraine war fade, inflation falls back to 2% on its own, no economic contraction required. But we know from first principles that an economic contraction is mathematically necessary to bring inflation back to 2%.

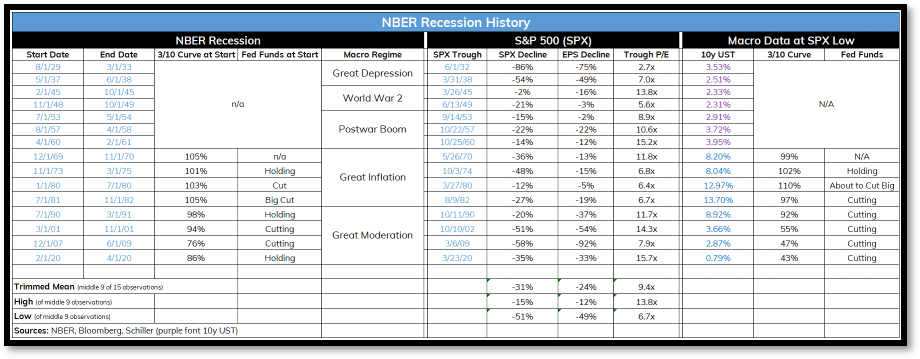

To home in on the likely destination of the S&P 500 in an economic contraction, the historical record is helpful. Since 1929 there have been 15 NBER2-defined US recessions, and on average (using a trimmed mean methodology) the S&P 500 falls -31%. A -31% decline from its January 4, 2022 ATH (4818.62) would put the ultimate trough around SPX 3325. That’s one way to look at it.

The other way is through the lens of valuation. Over the 15 NBER-defined recessions, on average the SPX troughs at 9.4 times peak EPS, which would put the trough for this bear market at around SPX 1974 assuming peak EPS of $210. But that’s likely (hopefully) too punitive.

A more nuanced approach to valuation, as outlined in “The Bear is Just Waking Up”, pegs the ultimate SPX trough around 2263.

The Path

The WOTE thesis is that the NBER will ultimately declare that a US recession began in 4Q22. Three reasons, as outlined in “The Bear is Just Waking Up”:

A deep, and persistent inversion of the 3y/10y US Treasury curve indicates economic activity is under heavy monetary policy-induced stress. Only once the curve steepens to at least parity can we begin to consider the possibility the stress is beginning to lift.

The OIS3 market’s refusal to price out 2H23 rate cuts, despite the Fed's insistence it will not repeat the "stop and go" policy error of the Burns Fed in the 1970s (reiterated since by Waller's repeated reference to keeping rates higher for longer for "risk management" purposes), indicates the Fed is likely to cut rates in response to a much deeper-than-anticipated economic downturn (or perhaps a dramatic tightening of financial conditions that the Fed wants to moderate - but such a tightening is unlikely to occur without a concurrent obvious decline in economic activity).

Still-robust Conference Board YoY Lagging Index growth of +7.4% masks the “real” deterioration beneath the surface of still-high nominal activity, as evidenced by the Leading Index at -7.4% YoY. This divergence is eerily similar to the Great Inflation period, where there was much debate in real-time4 about the state of the economy despite a crumbling 'real' foundation beneath the nominal surface.

Equity market bulls should hope that The WOTE is right. The sooner the US economy contracts and brings inflation back to 2%, the sooner the S&P 500 can move into a new bull market.

If The WOTE is wrong about the current state of the US economy - as strong equity market breadth, weak defensive sector relative strength, and healthier credit market conditions suggest could be the case - then the Fed will ultimately have to raise rates even more than expected in order to tighten financial conditions enough to contract the economy enough to bring inflation back to 2%.

But, but, but…what if there is a “soft landing”? There is no possibility of a soft landing without the Fed capitulating on its 2% target, because inflation is not transitory.

Here’s why.

Inflation is Not Transitory

This may come as a surprise to those who only know The WOTE as a raging bear, but all the way back in 2021 it was a raging bull on the economy and markets with an outside-consensus SPX target of 5000 by early 2022. Over the course of 2021 The WOTE did what it’s doing now - it took in as much evidence as possible from as many different sources as possible, and updated its then-bullish economic, market, and sector theses in real-time via writing. In that process it came across an October 19, 2021 research note from Bridgewater (BW) titled “It’s Mostly a Demand Shock, Not a Supply Shock, and It’s Everywhere.” Given BW’s longstanding expertise on the “economic machine” built up over decades of research, this “it’s not transitory” conclusion immediately took an out-sized weight in The WOTE’s thinking.

Fast forward to November 30, 2021 when Chair Powell retired “transitory” in front of Congress. Based on Wall Street’s muted reaction to Powell’s hawkish pivot due to its belief inflation was principally the result of “transitory” supply factors (and therefore the Fed would not have to hike rates all that aggressively), The WOTE knew immediately that it had an edge on the market by simply understanding that inflation is not transitory, as outlined by BW on October 19. It was that simple. And, shockingly, it remains that simple even today.

Here is BW on what it will take for the Fed to bring inflation back to a sustained 2% in its most recent public research note:

“…restoring equilibrium conditions will require an extended adjustment period of low nominal spending growth, negative real growth, and rising unemployment…[implying] at least a 2% rise in unemployment sustained over a long enough period of time to adjust the supply/demand balance for labor, a 2% decline in real GDP, and about a 20% decline in operating earnings as an inducement for the necessary layoffs.”

The bottom line: Because inflation is principally due to excess demand, and elevated wage growth underpins excess demand over time, the unemployment rate must rise to ensure inflation is brought back to a sustained 2%.

The best evidence available that “transitory inflation” (and in turn the potential for a “soft landing”) is still a commonly-held belief is from Fed Vice Chair Lael Brainard. In a January 19, 2023 speech she said:

“There are a range of views on what it will take to bring down this [nonhousing services] component of inflation to pre-pandemic levels. Since wages constitute a significant fraction of costs for most firms in nonhousing services, one possible channel is through a weakening in labor demand. That said, to the extent that inputs other than wages may have been responsible in part for important price increases for some nonhousing service sectors, an unwinding of these factors could help bring down nonhousing services inflation.”

Brainard believes it is still up for debate whether the unemployment rate needs to rise in order to ensure inflation is brought back to a sustained 2%. If you understand the BW “it’s not transitory” thesis, you know that Brainard is wildly off base if she is committed to the 2% target.

A few days later on January 23, Nick Timiraos of the Wall Street Journal cited Brainard’s speech as indicative of the debate within the Fed about how much it needs to weaken the labor market. In short, the Fed is looking to “feel its way” to the terminal rate in order to assess whether it really needs to drive the unemployment rate up to bring wage growth back down to levels consistent with 2% inflation.

If the economy is currently in recession as The WOTE believes, then the Fed has likely done enough and the economic contraction underway will take spending down and the unemployment rate up to levels consistent with what Bridgewater outlined is necessary to bring inflation back to a sustained 2%. But if the economy is not in recession (i.e. the Fed hasn’t done enough to crack the economy), then the Fed “feeling its way” to the terminal rate will underpin an easing of financial conditions that pushes inflation right back up alongside an acceleration in economic growth.

In either case the S&P 500 ultimately loses: recession now, significant near-term downside lies ahead; recession later, perhaps even more downside due to the need for the Fed to raise rates even higher.

Stop fighting the Fed. It’s making it worse.

(P.S. For a detailed write-up on the Powell Fed’s commitment to bringing inflation back to 2%, please see “Framing the ‘Arthur Burns Risk’ to the S&P 500” here.)

WOTE = Weight of the Evidence

NBER = National Bureau of Economic Research

OIS = Overnight Indexed Swaps