Market Journal: TLT Not Confirming

Market Journal: TLT Not Confirming

Please see here for more information about The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along. Thank you.

Discussion

The April 2022 analog I’ve discussed has failed to play out, but since this is the fourth term premium-driven correction, the other three analogs remain firmly in play, specifically the August-October 2023 correction.

This TLT-driven bounce in SPOOZ looks precisely like the late August/early September 2023 bounce, with TLT’s limp rally above its 20dma not confirming the move in stocks…unlike the November 2023 rally in the wake of the Fed/Treasury pivot when TLT ripped above the 20dma toward its 50dma.

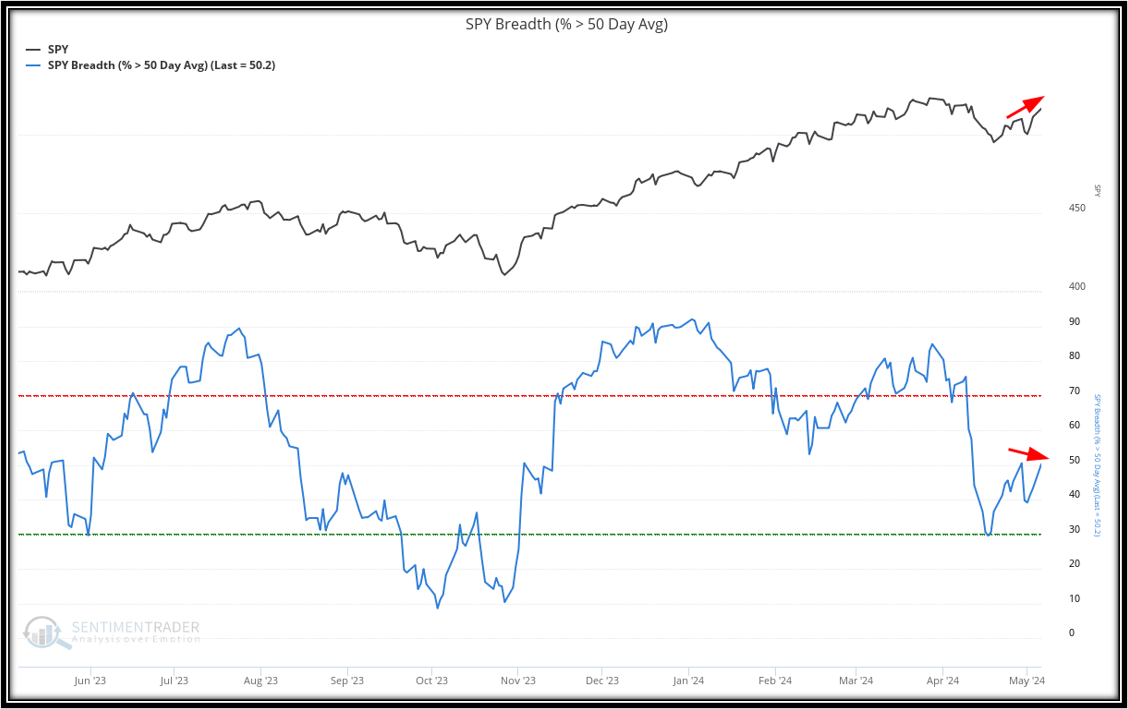

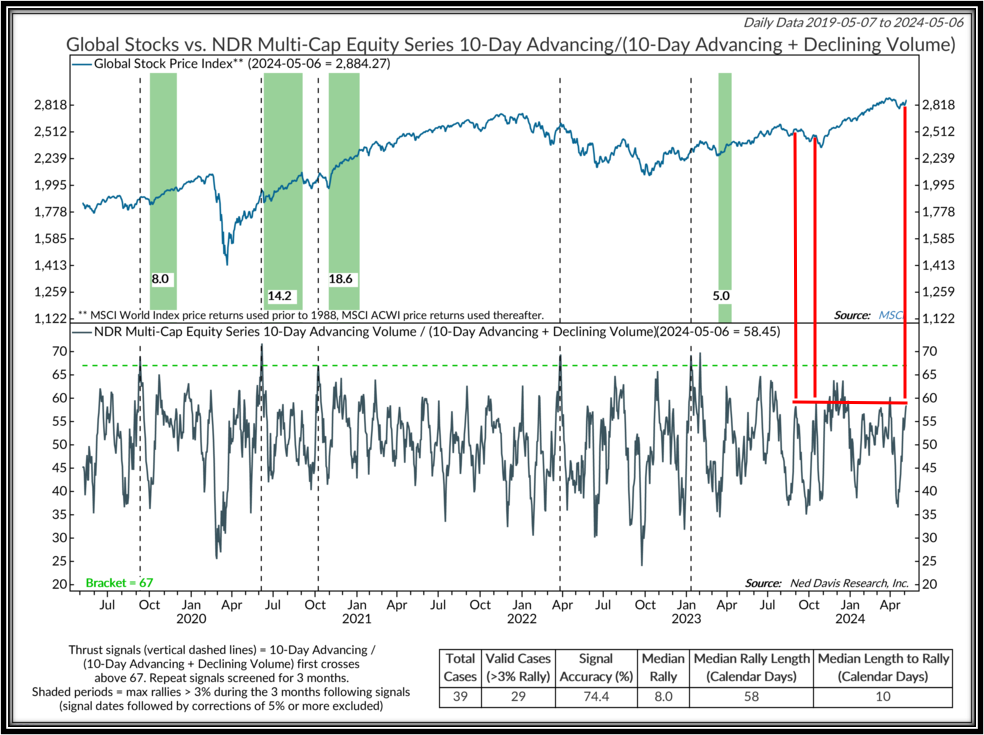

Further confirming the lack of rally oomph, SPY 50dma breadth is negatively diverging from the Index and advancing volume sits almost exactly at the level that marked the top of the late August/early September 2023 mid-correction rally.