WAM Strategy Note: May 16, 2024

WAM Strategy Note: May 16, 2024

Poor performance discussion, process enhancements, and current positioning.

Disclaimer: For informational purposes only.

Please see here for more information about The Weight of the Evidence (The WOTE) cross-asset market research platform. If you do not like The WOTE content, please unsubscribe. If you believe someone else might like the content, please feel free to pass along. Thank you.

Poor Performance Discussion

Since the SPX low last October this has been the worst stretch of portfolio management of my career. Which is really sad to me because A) I’ve done a good job of adjusting my thinking around the cross-asset market landscape, even if late to adjust at times, and B) I have all the tools necessary at my disposal to turn The WOTE into the Money Go Brrr machine I know it is capable of becoming. My core problem is three-fold: 1) aggressive portfolio management dictated by 2) a rigid positioning framework driven by a “well-constructed” cross-asset market thesis that is difficult to adjust in real time, and 3) ignoring my tools at pivotal inflection points.

My cross-asset market research style and aggressive portfolio management tactics have been developed over years of honing my own style against the backdrop of learning by observing Stan Druckenmiller and David Tepper. They are both incredibly flexible in their thinking, change their minds on a dime, and use aggressive portfolio management tactics to generate outsized returns over time. They’re not sitting there filling out their portfolio based on a positioning sizing matrix driven by a rigid cross-asset market thesis developed over days/weeks. They look for asymmetric return profiles by flexibly observing and weighing the cross-asset market evidence over time, and when a high-probability set-up emerges, they act quickly and in size.

I run five strategies through The WOTE:

WOTE US 60/40 (benchmark: 60/40 SPY/BIL)

WOTE US Core Equity (SPY)

WOTE US Long/Short Equity (SPY)

WOTE US Core FICC (BIL)

WOTE US Special Ops (SPY)

I launched these strategies in late 2023 as a way to better report on the performance of the cross-asset market research I journal via The WOTE. Prior to late 2023 I successfully ran my personal money using an undefined combination of these strategies, but unfortunately I didn’t document that track record prior to The WOTE and the incubation of these strategies in late 2023. So, day 1 performance is as of 12/31/2023. Performance so far is too embarrassing to actually put onto paper, so just assume that it’s ugly. Too much flip-flopping, too many stop-outs, etc, etc.

Process Enhancements

I texted a two close industry friends last night that this was the end of the road for The WOTE, as nobody would take my work seriously with performance this bad. But three things: 1) I’m the last person to quit at anything, let alone something that is a deeply, deeply ingrained passion (at a 17 handicap I am a good enough golfer to keep at it each season, but I’m bad enough and self-aware enough to know when it’s time to quit for the season lol); 2) after sleeping on it and mulling things over in great anguish, with a couple of small, yet powerful tweaks to the portfolio management process there is just far too much upside to The WOTE on all fronts to give up on this project; and 3) I need to separate the quality of my cross-asset market research and the quality of my portfolio management - those are two entirely different things, best summarized by the old market adage “do you want to be right, or do you want to make money?” For instance…

I’m letting yesterday’s decisively bullish equity market action affect my thinking around the direction of inflation and FED policy. I see the powerful breakout (i.e. on high volume) to new ATHs on SPX and think that I’m wrong about H4L rate policy and the likelihood the Fed will need to engineer a recession in 2025 in order to kill inflation ahead of Powell’s May 15, 2026 retirement date. But, while I was clearly wrong on the call to cling tight to cash and shorts, that bad portfolio management call should not influence my cross-asset market conclusion that a second inflation wave is firmly in train. But, but, the conclusion that a second inflation wave is in train should not influence how I position for a continuation of a powerful breakout in equities.

In short: research process GOOD, portfolio management process BAD. So, three small, yet powerful tweaks:

I’m no longer going to maintain a rigid three-duration outlook-driven positioning framework (i.e. the Structural, Cyclical, and Tactical outlook system). I will use those three durations to discuss the SPX market outlook across the platform, as they’re a useful way to frame the cross-asset market evidence across durations, but I’m going to use them more flexibly in my search for asymmetric return profiles.

My default positioning across four out of five strategies will be a neutral benchmark weight (WOTE Special Ops’ default position will be cash). Regardless of the macro backdrop, when there is an absence of asymmetric return opportunities, I will sit at neutral. When asymmetric return opportunities present themselves, I will act aggressively - in size and speed.

The best example of the need for this tweak is in WOTE US Core Equity. I’ve been whipped around all over the map YTD trying to position in various sectors using a combination of my cross-asset market outlook and relative strength analysis. There has been nothing in the way of decisive asymmetry (of course, with the benefit of hindsight someone could say Utilities were an opportunity at the lows, but that was not even remotely asymmetric in real time) available across the SPX sector map, and I’ve paid dearly for trying to manage exposures at the margin.

WOTE US Core Equity will retain its SPY benchmark, but I am broadening the mandate out to the global equity market in order to create more potential opportunity for asymmetry. Of course, I could simply change the benchmark to ACWI, but my background is in US equities so I prefer the clean benchmark of SPX, and if something outside the US is not in an asymmetric position to beat SPX, I won’t own it.

Current Positioning

As detailed via the Chat function (see here and here) this week, I stopped out of my short positioning in Special Ops ahead of CPI, and then in Long/Short the day of CPI (today I put Long/Short into neutral position via SPLG). Core Equity moved to a neutral position back on May 2, and on May 6 I took 60/40 to a neutral position.

WOTE US Core FICC is where I currently see the most asymmetry. On May 6 I took it to 50% short UST 20s via the TBF ETF, and today I took that to 100%. The long end of the UST curve will continue to act as the release valve for the second inflation wave FED policy currently seeks to engineer (for whatever reason), and if the economy happens to abruptly weaken from here and the Fed responds with cuts, the long end will simply continue to rise on the back of even more fiscal stimulus. In the unlikely event long-term UST yields continue moving lower, I will further increase short exposure via -2x UST ETFs.

After this move up in equities there is no durable asymmetry available to the upside outside of a short window here into EOM. I took a small May 31 SPY call position in Special Ops today to play upside into EOM, but to increase long exposure in 60/40 and/or Long/Short I would need to see SPX pullback to at least the 20dma if not the 50dma. For now, I need to take my performance lumps and sit in neutral while I wait for asymmetric set-ups. Unless something changes across my cross-asset market toolbox, I don’t see an asymmetric short set-up from now until Election Day unless SPX goes truly parabolic.

Exhibits

This breakout in SPX above a prior high into OPEX is akin to June of last year when SPX followed through with another 2.5% up before rolling over to the 20dma. Super short-term tactical set-up.

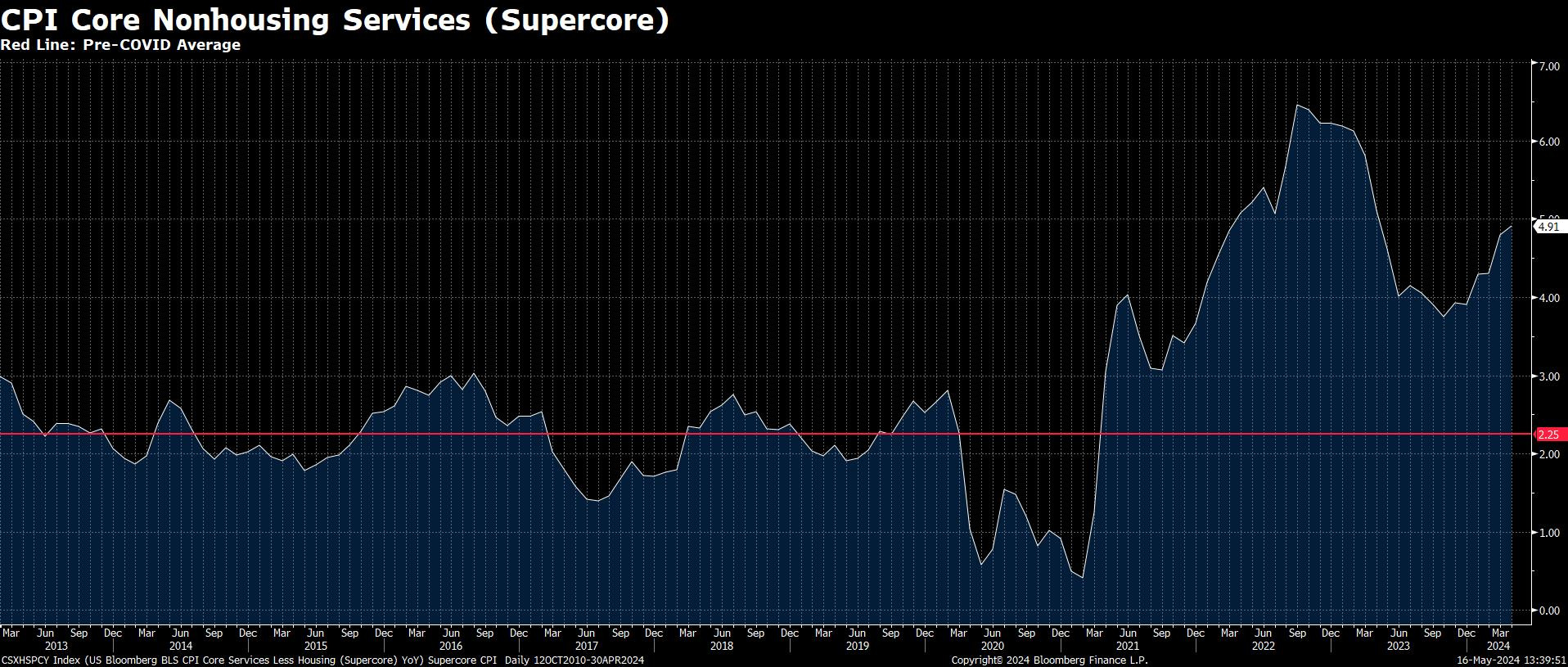

The reason I am confident a second inflation wave is underway is two-fold: 1) supercore inflation is moving decisively higher,

And 2) the BCOM commodities index is moving decisively above its 200dma, a key feature of a reacceleration in inflation in years past.

Please don't quit publishing your writings!

Yes, it's hard to put your thoughts out there, be wrong in real time in some ways when speaking with authority, and then be poo pooed by people who don't put any of their own thoughts or actions on the line

You've got good ideas and I love reading them. Though I think you could benefit more from technical analysis (just seeing rotations, widening breadth, breakouts, etc.) on key market indices and variables (like TLT) and from liquidity and Fed actions other than interest rate tidings. The Macro is dead substack gets at this - - macro is dead - - as do the stocktwits new charts newsletter and the rationale for it. Markets operating on larger scale. I like Avi Gilbert too for thinking of the larger picture. Yes, wacky Eliot Wave stuff. And Bogleheads for teaching me to tune out the noise.

Your talk of the Yellen put and the 6K SPY target you wrote about were spot on for instance. But I think your larger biases of valuing the strict macro and fundamentals view overrode those passing thoughts

Again, easy for me to say as a passive investing mostly bullish guy. But I like reading your stuff, John Hussman's, Jeremy Grantham's, and Howard Marks' alike. Valuable voices and opinions!