The Market: The Ketchup is Finally Out

The Market: The Ketchup is Finally Out

Nick Timiraos recently compared monetary policy to hitting a glass ketchup bottle. Well, the ketchup (US recession) is finally out - Powell's appearance in front of Congress was the final hit.

Discussion

On Wednesday March 8 The WOTE wrote the following post titled “Powell Just Napalmed Financial Markets” (And the S&P 500 still doesn’t get it. Yet.):

This will be short. Yesterday and today in front of Congress Fed Chair Jerome Powell:

Guided to a higher terminal rate

Opened the door to a faster hiking pace (50 bps versus 25) starting on March 22

Publicly accepted the historical fact that at least 7% unemployment is required to bring inflation down to 2%

And, most critically, guided to a higher long-run neutral rate

And the S&P 500 barely budged.

The stock market is a strange animal. Large institutional investors knew full well in January 2020 that COVID was a big risk to markets, yet the SPX didn’t react until the middle of February. In early 2008, after the US economy had entered recession with credit markets on fire, economically sensitive industrial stocks went vertical. We all know what happened just months later.

It is The WOTE’s suspicion there is a lot of “long-term oriented” lazy stock market money fast asleep while Powell’s napalm barrels toward it.

As always, economic gravity will win in the end.

24 hours later Silicon Valley Bank’s stock was halted. Another 24 hours later SVB went into FDIC receivership. It’s now March 19 and the entire global financial system is embroiled in a banking crisis. NONE of this is a coincidence. Powell’s appearance in front of Congress was the final hit of the proverbial glass ketchup bottle, and now the ketchup (a US recession) is finally out.

The Real “Big Flip”

Starting around the time of the January NFP report that blew away consensus expectations, the #biglip hashtag became popular on “Finance Twitter”. It was a great call by the hashtag originator, as evidenced by the fact the 2-Year US Treasury Note yield rose from 411 basis points to 507 in just over a month. But in less than 2 weeks it has since fallen to below 400. THAT is a big flip, and it didn’t happen simply because market participants were out of position and forced to cover their 2-Year Note shorts. Something broke.

Mind the Data, Please - Part 2

In “The Bear is Just Waking Up” on January 18 The WOTE said:

“The Overnight Indexed Swaps (OIS) market currently has the Fed hiking the Fed Funds Rate (FFR) to 489 bps by June (another 50 bps of hikes) and then cutting to 436 by December (right back to current levels of around 433 bps).

“Given the Fed’s steadfast commitment to not repeat the ‘stop and go’ policy error of the Burns Fed in the 1970s, it is highly unlikely the Fed will cut rates so soon after terminating the hiking cycle and risk fatally wounding its 5-10 year inflation-fighting credibility. The Weight of the Evidence (WOTE) thesis is that these cuts imply something more sinister is at work, that being: The economy is much weaker than the Fed believes…”

The dramatic repricing of rates from early February to early March made it look like the above analysis from January 18 was a complete misread of the message from the bond market. And perhaps it was. But given the speed of the downward repricing of rates to levels below where they were on January 18, The WOTE has a strong hunch that on January 18 the bond market was sniffing out “something more sinister” along the lines of the current banking crisis, not simply inflation melting back to 2% and allowing the Fed to cut rates.

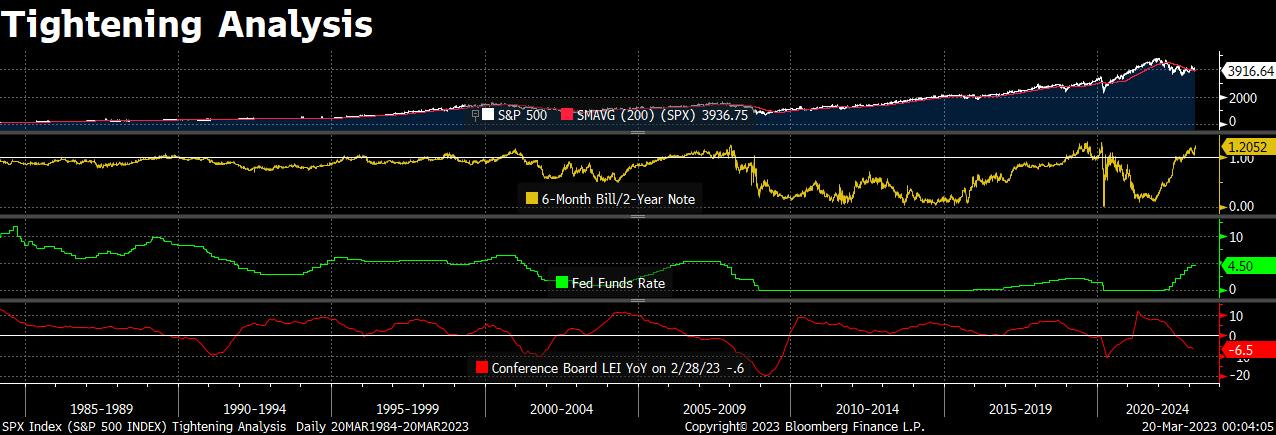

At present, the 6-Month US Treasury Bill yield is 20% above the 2-Year Note yield, historically a sign of material financial system stress that is likely to be relieved soon via rate cuts and/or balance sheet operations. Most recently, in 2019 the Fed launched its Bill purchase program to inject liquidity into the repo market and the spread moved back to parity, propelling SPX higher; likewise, in 1998 the Fed cut rates in response to the fallout from LTCM, and the SPX rocketed higher alongside a collapse in the spread. But in both 2019 and 1998 the economy was in decent shape, as represented by the YoY change in the Conference Board Leading Index sitting above 0%.

In 2001 and 2008, however, when the 6-Month Bill/2-Year Note ratio spiked to 120% the Conference Board Leading Index was negative YoY. As it is today.

Have you ever tried to clean up a spilled bottle of ketchup (a recession) without a paper towel (rate cuts)? It’s ugly.

It’s a Trap

The speed of the government response to the banking crisis probably makes Helicopter Ben blush. But for two reasons it’s the wrong response. 1) Forced mergers of banking institutions, on questionable terms, by definition cannot restore financial market confidence in the banking system. In the wake of last week’s deposit injection into FRB by a consortium of US banks and tonight’s UBS/Credit Suisse deal, the first question market participants are going to ask is “Who’s next?”, followed quickly by “Why are central banks panic-injecting liquidity into the banking system - what’s really going on?” 2) Forced mergers and liquidity injections do not address the underlying issue that nobody is really talking about: deposits are underpriced relative to short-term government securities, and regardless of the safety of deposits consumers are going to continue to pull money out of banks in search of much higher risk-free rates.

The data below are a bit dated due to their lagged release, but as of 12/31/22 the Fed Funds Rate was 369 basis points above the average cost of funds for an FDIC-insured US bank, far above the long-term average of 39 bps, and well above the 150-200 it typically peaks at toward the end of a hiking cycle. In short, banks have dragged their feet on raising deposit rates in order to enjoy a now-not-so-free lunch of rising net interest margins. This banking crisis has acted as a giant spotlight on deposits, leading consumers to not only question their safety but also their efficacy.

Banks are in a trap. If they raise their deposits rate to retain customers, their net interest margin will compress without an offsetting rise in lending rates. But if they raise rates on loans, demand for loans will fall, economic activity will slow, and defaults will rise, further compressing bank profitability and capital ratios.

The Fed is also in a trap. Liquidity injections at market rates are dilutive to bank net interest margins, which as explained above slows economic activity. But if the Fed seeks to bolster bank net interest margins with rate cuts and “quantitative easing” (a no-cost liquidity injection), the economy will turn higher and keep inflation above the Fed’s 2% target.

The Bottom Line

The WOTE believes the “crack” Bridgewater’s Greg Jensen discussed last November is upon us. Once the economy begins heading south in earnest, the full weight of the Fed’s anti-Burns reaction function will be felt. Stay buckled.