The Market: Take 1987 Seriously, Not Literally

The Market: Take 1987 Seriously, Not Literally

Discussion

Gazing at historical market analogues is a favorite pastime of all students of market history. You can’t help it, as human nature is ruthlessly consistent across time. But the key is to not become a slave to analogues, as history tends to rhyme, not repeat.

Once rates began to really move back in early August I wrote about the potential for a 1987 event if rates continued moving higher, but I actually wrote it to dispel the notion in my own head that higher rates is near-term bearish for equities, as in 1987 SPX kept moving higher alongside rates and didn’t really crack until rates accelerated to new highs. Last week I expanded on the analog by looking at how 200dma breadth evolved in the lead-up to the 1987 crash, and concluded that SPX was likely closer to an “event” than originally thought.

Unfortunately, the 1987 analog gained a fair amount of traction across “FinXwit” over the weekend, which is almost always the death knell of an analog. Andy Constan wrote about the “silliness” of it, highlighting a past Xwitter thread he penned about the mechanics behind the 1987 crash.

However, I think there is a happy medium here. I think the combination of a fully valued SPX at best, an overvalued SPX at worst, weak breadth, quickly rising rates, and an aggressive FED demands that we at least take the analog seriously, if not literally.

Cross-asset market action so far this week is almost precisely in line with the lead-up to the 1987 crash as discussed last week: breadth is breaking down, rates are breaking out, and just today SPX closed below its 50dma while its MACD is topping out. Rates have yet to make decisive new highs, but the fact both UST and TIPS 10s and 30s are knocking on the door of new highs despite a “helluva a week of [soft landing] data” last week says rates want to move higher.

The seemingly benign action in SPX this week despite cross-asset market stress beneath the hood is not simply a function of VOL markets controlling the action. This is how markets work. This is precisely how SPX traded in the lead-up to the 87 crash, meandering along in a deceptive fashion before the bottom fell out.

As Andy Constan discussed this weekend, the structure of today’s equity market is unlikely to allow for an 87-style crash; but something along the lines of a -20% move in a week is absolutely in the cards. Just in case, for reference, below is the current circuit breaker structure of the US equity market:

1987 Analog Exhibits

As discussed last week, SPX did exactly what it needed to do today to keep the 87 crash analog in play.

In eerie symmetry to 1987, 200dma breadth is breaking down sharply following an ominous lower high (the snapshot below does not include today’s further breakdown).

UST and TIPS 10s and 30s are behaving as if they want to accelerate to new highs, which would cement the 1987 analog.

Today’s Cross-Asset Market Exhibits

SPX continues to bearishly diverge from HY CDX on a short- and long-term basis…

…As well as NYSE 50dma breadth.

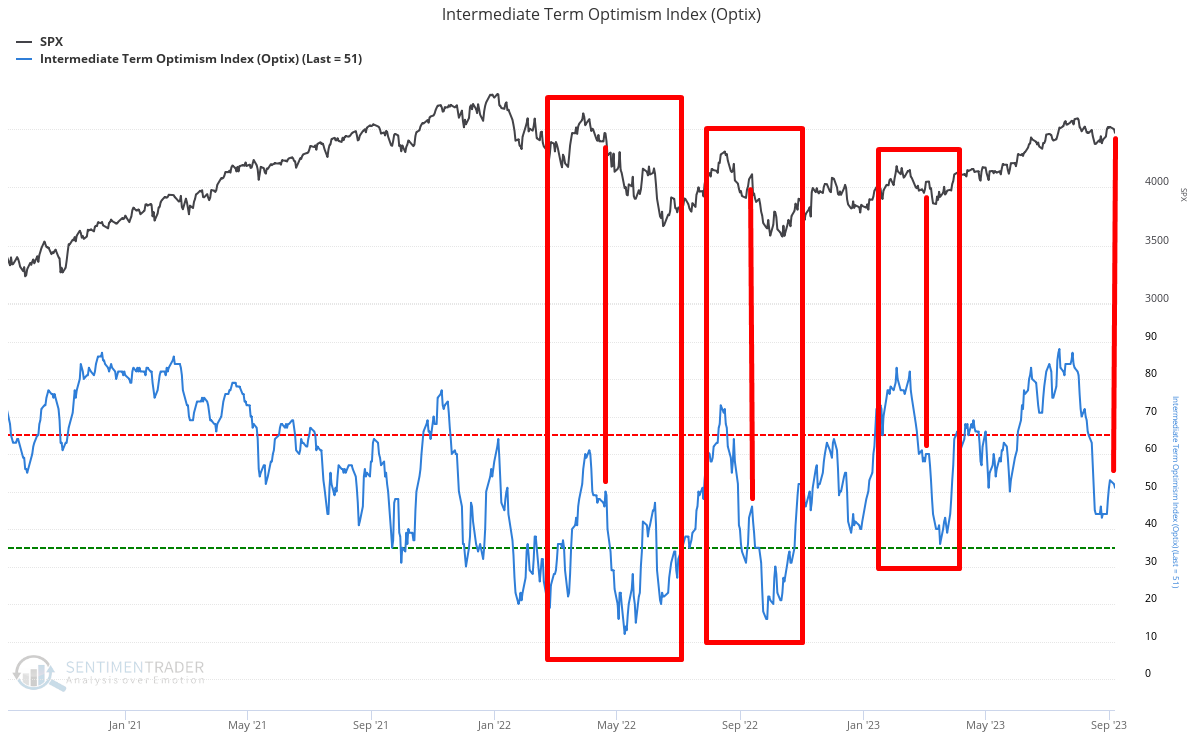

Medium-term sentiment is behaving precisely in line with mid-correction periods since December 2021.

And lastly, on a micro time frame basis defensive sectors did not confirm today’s afternoon reversal in SPX.