The Market: Soft Landing Trees in a Burning Forest

The Market: Soft Landing Trees in a Burning Forest

Discussion

Just step back, zoom out, and think about what’s going on right now:

The developed market manufacturing sector is in recession, and arguably getting worse

Eurozone manufacturing and services PMI data surprised to the downside this morning (and we’ll see at 9:45am EST what S&P Global reports for US data)

The Fed and ECB are still raising raising rates and at best will maybe pause after hiking this week

The 3y/10y UST curve is already deeply inverted, has been deeply inverted for months now, and is again re-inverting after its early-July steepening on softer than expected inflation data

Meanwhile…

Equity market valuation has materially decoupled from interest rates

Equity market sentiment and positioning are behaving as if a new economic upswing is underway

The long end of the TIPS break-evens curve is starting to move

And negative divergences across the cross-asset spectrum are beginning to pop up

Prominent contrarian trader Jason Shapiro was out recently in two videos mocking (rightfully so, mind you) those who have been bearish all year, saying macro doesn’t matter, he doesn’t expect a recession, and the rally in equities is unlikely to stop until the fundamental bears capitulate. He is likely correct, as I have a tough time seeing this SPX squeeze formally end without a move to the 4818.62 ATH, but the vitriol toward the ultimate importance of a decidedly bearish macro outlook is a very, very, very important tell looking out 6-18 months.

The bottom line: MACRO MATTERS. Continued rate hikes into a deeply inverted curve with economic conditions deteriorating and equity market investors getting rapidly and increasingly more bullish at valuations decoupled from the 4-5.5% available risk-free is perhaps a set-up we are unlikely to ever see again. Mission critical to not miss the burning macro and market forest from the soft landing trees.

The biggest question equity market participants need to answer (and why it’s so important to bob and weave throughout this topping process) is how long structured product “pinning” of the S&P 500 can insulate the Index from the burning forest.

Exhibits

Ugly set of data from the Eurozone this morning.

FED is set to hike this week with a tightening bias.

The 3y/10y UST curve is re-inverting (again).

Fed Funds futures contracts are pricing out rate cuts later on faster than in the near-term (higher for longer).

The long-end of the TIPS break-evens curve is starting to move. Once the entire curve starts to go the Fed WILL react in force.

SPX valuation has materially de-coupled from real rates.

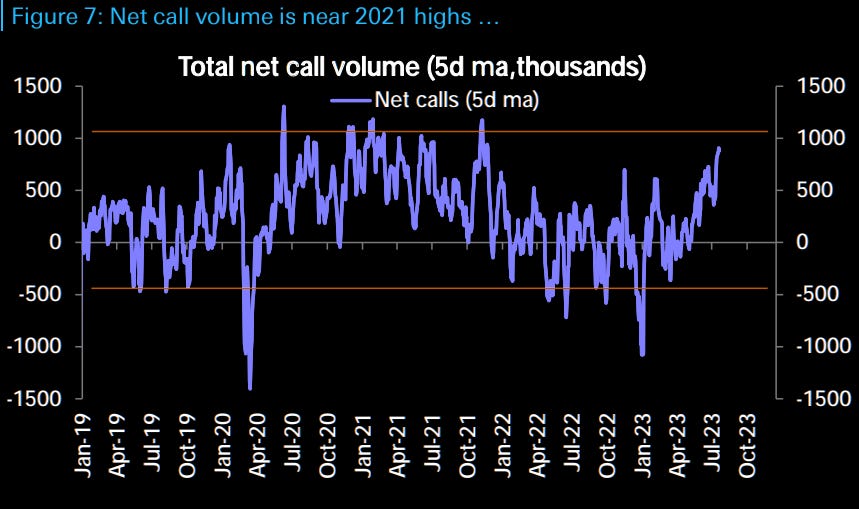

Positioning and sentiment have blown out to the upside despite all of the above.

And last but far from least, a whole host of negative divergences have begun to pop up across the cross-asset spectrum.