The Fed: Reacceleration Will Not Be Tolerated

The Fed: Reacceleration Will Not Be Tolerated

Discussion

As discussed in The WOTE Report this weekend, the Fed is pleased with the long-end-led tightening of financial conditions since late July…

…as evidenced by key pieces of communication via Nick Timiraos at the Wall Street Journal on October 10 and October 12.

But since the beginning of October, in an attempt to smooth out the tightening of financial conditions the Fed has talked down the need to hike again as a result of the rise in long-end rates. The problem with this “controlled demolition” approach is that financial market participants - equity investors in particular - take any sign of the Fed attempting to smooth out the tightening of financial conditions as a sign they’re really not that serious about bringing down inflation, which just eases financial conditions and reinvigorates animal spirits and economic activity, which in turn forces the Fed to do even more.

It’s clear the Fed is not going to stop its “controlled demolition” approach anytime soon, as they really do not want to oversee a true crash in asset prices. But from the standpoint of financial market participants immediately jumping to dovish conclusions I believe there is a good chance last week’s September CPI report marked a critical inflection point.

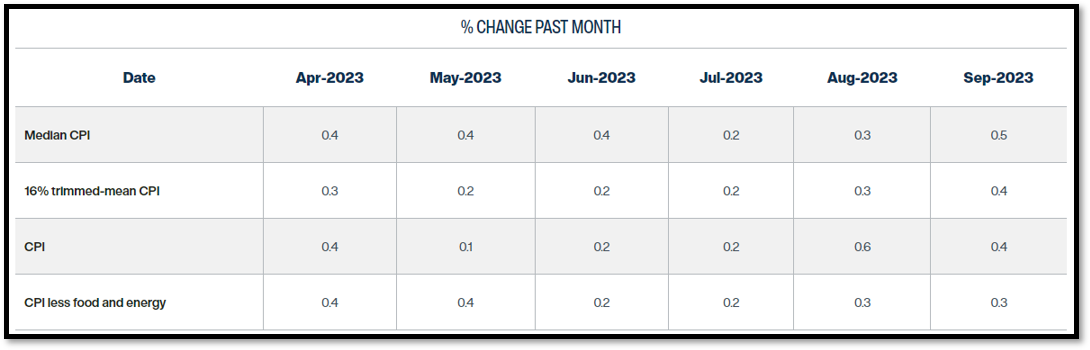

Critical Inflection

Inflation has been in a steady downtrend since its 2022 peak, but over the last two months it has ticked back up on a MoM basis. All along the Fed said that the journey back to 2% is going to be bumpy and that they are not going to overreact to said bumps - but after last week’s September CPI report the Fed came out in force to underscore the fact they “will not tolerate a reacceleration in prices” and that it looks like inflation is beginning to settle out around an unacceptably high level relative to its 2% target at 3%. Even I was surprised at the forcefulness of the response.

With Israel-Hamas at minimum putting a floor under the price of oil, University of Michigan inflation expectations ticking higher, and TIPS break-evens solidly above December 2021 levels, the set-up here for those looking for a dovish Fed is exceedingly poor.

Inflation has begun to tick higher.

As have inflation expectations.

But it’s clear the Fed will absolutely not tolerate above 2% inflation.