The Fed: John Williams NYT Interview

The Fed: John Williams NYT Interview

The good (dovish), the bad (hawkish), and the ugly (bearish).

Discussion

FRB New York President John Williams, a key member of the “holy trinity” (Powell and Jefferson being the other two), sat for a comprehensive interview with The New York Times last week, and of course the headline takeaways from the interview were skewed dovish (below are the title and subtitle of the article itself, as well as the “breaking news” tweets about the interview).

But as to be expected from a comprehensive interview there was something for everyone. Let’s let the doves fly first…

The Good (Dovish)

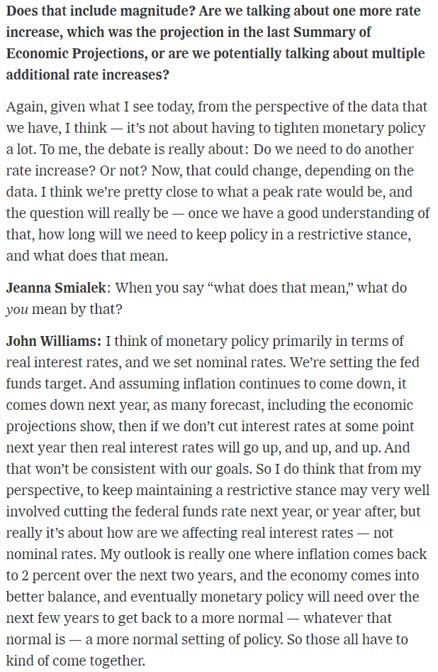

Maybe one more hike.

Wide open to cuts if inflation falls in order to keep the real Fed Funds Rate from becoming too restrictive.

Also open to cuts for non-inflation reasons.

PCE likely to end 2023 at 3% versus the 3.2% in the June SEP, and underlying inflation is on the descent.

Wage growth is less of a target of monetary policy than it is an indicator.

Risks are two-sided at this point (probably the most dovish part of the interview given how tight the labor market is on paper).

Economic reacceleration doesn’t bother the Fed until inflation expectations start moving up.

Long-term neutral rate likely hasn’t risen beyond where it was pre-Pandemic.

The Bad (Hawkish)

Whenever a key FED official is given the opportunity to share what’s on their mind, it pays to pay attention. The NYT interview led off with such an opportunity, and Williams jumped right into the necessity of bringing supply and demand back into balance in order to ensure inflation is brought down to 2% on a sustained basis. The money quote was:

“…I know the inflation data, absolutely critically important, but I think it’s also making sure that the fundamentals of our economy are in balance to get this sustained achievement of re-anchoring, or not re-anchoring (Freudian slip there?), but restoring price stability, getting 2 percent inflation on a sustained basis.”

While on one hand Williams talking about cutting rates is dovish on paper, the fact of the matter is he is talking about cuts in the context of maintaining restrictive policy for an extended period of time to keep inflation at 2% through the cycle. Whether a “real” Fed Funds Rate of 2% at 2.5% inflation (4.5% nominal) is enough to keep inflation at 2% remains to be seen, but with the Fed clearly determined to keep inflation at 2% through the cycle, the commitment to maintaining whatever level of real FFR is necessary to keep inflation at 2% is just not dovish. Simple as that. And further…

…Later on in the interview Williams says he believes the current level of the real FFR is “moderately above any reasonable estimate of neutral.” This is a very sneaky way of backing what Powell said at the July press conference: no consideration of cuts until a “full year from now.”

Williams’ openness to the unemployment rate shooting above 4-4.5% was striking. A distinct change in tone from his comments in July when he went out of his way to paint the soft landing picture.

And lastly for the hawkish camp, Williams reiterates that the end of QT is “well off in the future.”

The Ugly (Bearish)

#1: Williams nuked the bull case of an economic reacceleration. The Fed WILL respond to an economic reacceleration. This is the “B side” of a highly data-dependent Fed. Can’t have it both ways. What makes this so bearish is that the better the economy does, the more harm the Fed ultimately imparts by either raising higher than it otherwise would, or by holding for longer than they otherwise would.

#2: Far and away the most bearish part of the interview was Williams’ repeated insistence that the Fed will drive inflation back to 2% on a sustained basis. And like it pays to pay attention to answers to open-ended questions, it pays to pay attention to how key FED officials close interviews. In this case Williams closed with a discussion about how the 2% target is intimately entwined with the full employment side of the mandate and the Fed’s commitment to AVERAGING 2% inflation over time:

“…we actually have the tools to manage a 2 percent inflation target and achieve our goals over time.”

“I personally felt comfortable that a 2 percent target, along with a commitment to achieving 2 percent inflation on average over time, positioned us well to achieve those goals.”

The Ugly (Bearish) Exhibits