The Fed: Framing the “Arthur Burns Risk” to the S&P 500

The Fed: Framing the “Arthur Burns Risk” to the S&P 500

The Federal Reserve's steadfast commitment to not repeat the "stop and go" policy error of the Burns Fed in the 1970s is not yet priced into stocks.

Discussion

On July 5, 2022, WSJ chief economics correspondent Nick Timiraos wrote about the Fed’s determination to not repeat the “stop and go” monetary policy that underwrote the Great Inflation period of the 1970s. Theretofore the Fed had been focused on achieving a “soft landing”, so if Timiraos was writing on behalf of senior Fed officials then it signaled the first step in a much more hawkish policy direction with profound implications for the stock market. Not repeating “stop and go” means not easing monetary policy in response to an economic contraction. The history of equity bear markets is such that the major declines of at least -30% almost always occur in and around a US economic contractions; but most importantly, at the bottom of the bear the Fed is always easing monetary policy. Always. Easing monetary policy is the “mother’s milk” of bear market bottoms. The Fed committed to not easing policy in response to an economic contraction, with US equities coming off one of the great valuation bubbles of all time, is a jarring proposition.

5 days later on July 10 Timiraos again wrote about the Fed’s focus on not repeating “stop and go”. Given Timiraos’ reputation as well-sourced on Fed policy, the second column in 5 days underscored the seriousness of the hawkish shift. Clearly it was a signal from senior Fed officials, a fact rubber stamped 4 days later by former NY Fed President Bill Dudley, one of a handful of key former Fed officials known to speak on behalf of the Fed.

On July 14, Dudley outlined in detail what the Fed’s commitment to not repeating “stop and go” entails for monetary policy:

“Developments in the US economy have recently been going the Federal Reserve’s way, with price pressures peaking even as economic growth and strong payroll gains have been sustained. But don’t be fooled: The task of getting inflation back to the Fed’s 2% target remains extremely daunting, both practically and politically.”

“…energy prices have fallen, core inflation is decelerating, wage inflation might be declining and longer-term inflation expectations remain well-anchored. To some, this might look like the beginning of a soft landing and a potential triumph for the Fed. Far from it.”

“For one, the Fed hasn’t made much progress in curbing the excessive demand for workers. Second, the Fed needs to be confident that it has succeeded in pushing inflation back down on a sustainable basis. In the late 1960s and the 1970s, the central bank tightened monetary policy enough to push inflation lower at times, but it reversed course too soon. As a result, the peaks and the troughs for inflation kept moving higher…Given this history, officials will be hesitant to stop tightening until they’re highly confident (probability greater than 80%) that they’ve done enough — that the labor market has sufficient slack to keep inflation low and stable, and that easing financial conditions won’t lead to a inflation rebound.”

Just over a month later, starting with Fed Chair Jerome Powell’s August 26 speech at Jackson Hole, the commitment to not repeat “stop and go” became the official message of the FOMC and has remained so ever since.

At Jackson Hole Powell repeated Dudley’s July 14 message almost verbatim:

“Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.”

“Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century.”

“That brings me to the third lesson, which is that we must keep at it until the job is done. History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting.”

“We will keep at it until we are confident the job is done.”

On August 27, the day after Powell, ECB executive board member Isabel Schnabel hammered home Powell’s message in a powerful speech outlining the need for central banks to avoid the mistakes of the 1970s; and in speeches and media appearances subsequent to Jackson Hole, the FOMC has uniformly stated its determination to avoid the “stop and go” policy error of the Burns Fed in the 1970s. As recently as this week, San Francisco Fed President Mary Daly and Fed Governor Michelle Bowman warned against prematurely easing monetary policy. Here’s Bowman:

“From the late 1960s through the mid-1980s, the U.S. economy experienced high inflation, high unemployment, and declining living standards. During that time, policymakers prematurely eased monetary policy when the economy weakened, and inflation remained high. The FOMC was forced to return to tightening monetary policy, causing a deep recession in 1981 and 1982. This is an important lesson that guides my thinking about monetary policy and my continued support for policy actions that will continue to lower inflation.”

The Fed’s commitment to not prematurely easing monetary policy is crystal clear. And as evidenced by the deepest 3y/10y US Treasury curve inversion on record, the bond market appears to get it. But the stock market does not.

At its October 13, 2022 intra-day low of 3491.58 the S&P 500 traded for 16.9x trailing peak LTM EPS of $207. If that was THE low for this recessionary bear market, it would be the highest trough P/E going back to 1929 (15.7x at the 3/23/20 low is the highest).

For the 15 NBER-defined US recessions since 1929, the trimmed mean trough SPX P/E is 9.4x peak LTM EPS. If peak EPS for this cycle settles out at $210, 9.4x implies an SPX trough of 1974. It seems unlikely SPX will get there given the amount of liquidity in the system and the proclivity of FOMC rhetoric to veer dovish in response to tightening financial conditions, but it is certainly not outside the realm of possibility. A level that would more appropriately account for the “Arthur Burns Risk” is perhaps the 1970 trough P/E of 11.8x, which would imply an SPX trough of 2478.

The opening paragraph of this post touched at a high level why the “Arthur Burns Risk” is so acute. Below explores the risk in more detail, and fleshes out why SPX 2478 might in fact be too bullish for a final bear market trough.

The Arthur Burns Risk

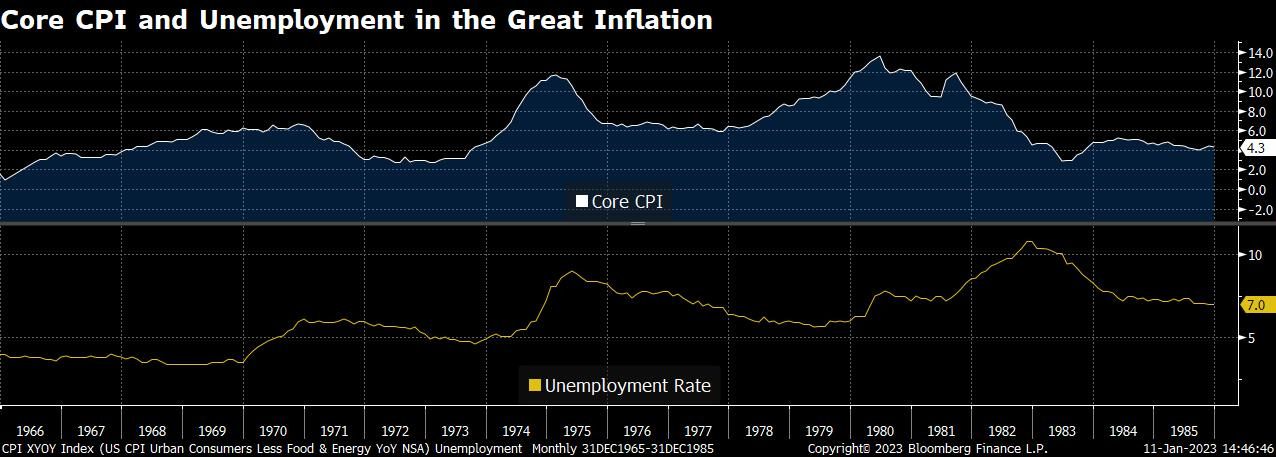

As illustrated below, once Core CPI inflation broke out above 4% in 1968 it went on to make a series of higher lows and higher highs, peaking at 6.6% in 1970, falling to 2.8% in 1973, rising to 11.7% in 1975, falling to 5.9% in 1977, and then ultimately peaking at 13.6% in 1980.

The Burns Fed began easing policy in the first half of 1970 with Core CPI running at around 6% YoY. Inflation went on to fall to 3.1% by December 1971 and stayed right around 3% for all of 1972 and the bulk of 1973.

Step back and think about that. The Burns Fed successfully brought core inflation down to the 2-3% level, where it stayed for almost two years. THE BURNS FED BEAT INFLATION by any sensible real-time definition. The “stop and go” policy error of the Burns Fed is only known with the benefit of hindsight. Whatever mistakes the Burns Fed made in 1972 and 1973 to set the stage for the rise to 12% in 1975, every single member of the current FOMC would have made them. Every single one.

Because the Powell Fed is terrified of declaring victory with inflation at 2-3% as the Burns Fed did in 1972 and 1973, it is virtually guaranteed to dramatically overtighten monetary policy from the standpoint of asset prices and nominal economic activity. However, if inflation is as entrenched as it was in the 1970s, then said “overtightening” is not overtightening from the standpoint of bringing inflation back to 2-3% once and for all via a resetting of supply and demand in the labor market.

What is mission critical for equity market participants to understand is this: The Fed’s reaction function, rightly or wrongly, will continue to be driven by the assumption inflation is as entrenched as it was in the 1970s. A recent New York Times interview with Minneapolis Fed President Neel Kashkari underscores this point well:

“If inflation were to fall to 3 percent with unemployment increasing to 6%, things could get tricky.”

The Fed debating whether or not to ease monetary policy with the unemployment rate at 6% is not something factored into current equity market psychology. It’s just not. But the Fed is going to force the issue whether market participants like it or not, because the Burns Fed “prematurely eased” policy with the unemployment rate over 6%.

In conclusion: buckle up for the possibility of an even lower trough P/E than 11.8x.