The Fed: Dreaming of the Perfect Landing

The Fed: Dreaming of the Perfect Landing

Riding Powell's Maestro fantasy to SPX 5500-6000 in 2024. Volcker returns in 2025, but that's an issue for post-Election Day. Until then, party on.

Burns Posture

Financial market participants are all aflutter about whether FED Chair Powell meant to underwrite a large-scale easing of financial conditions by hinting that the FOMC formally launched discussions about 2024 rate cuts. This is very simple: Powell knew exactly what he was doing, as evidenced by the fact Governor Waller previewed the pivot two weeks earlier ahead of blackout.

In my note about Waller’s comments I suggested that the Fed was not actually pivoting to a dovish posture, but rather was simply trying to stabilize inflation expectations so they are not “forced” to cut later to arrest deflationary forces. But I closed the note with the following:

…I need to wide open to the possibility Powell is in fact Burns, because the fact the Powell Fed gets this skittish with break-evens at 2% means there is still a decent chance Powell really goes for the soft landing instead of cementing an anti-Burns legacy.

Turns out my concerns were very well founded. Powell is Burns.

Powell is going all out for the soft landing, as articulated by his key messenger Nick Timiraos…

…and illustrated by his key Soft Landing lieutenant Jan Hatzius of Goldman Sachs in a note out this morning titled “The Great Disinflation”:

This pivot to a Burns policy posture is critically important to the outlook for risk assets because it means that in a high-pressure, demand-driven inflation macro nominal growth will remain higher than it otherwise would, underpinning stable corporate earnings power and strong pricing power. So for instance, at 4700 SPX is trading at a 4.3% earnings yield assuming normalized EPS of $200 for easy math versus a 4.1% UST 30s yield. That 30y rate will not grow, but the 4.3% SPX yield will, especially in a high nominal growth regime.

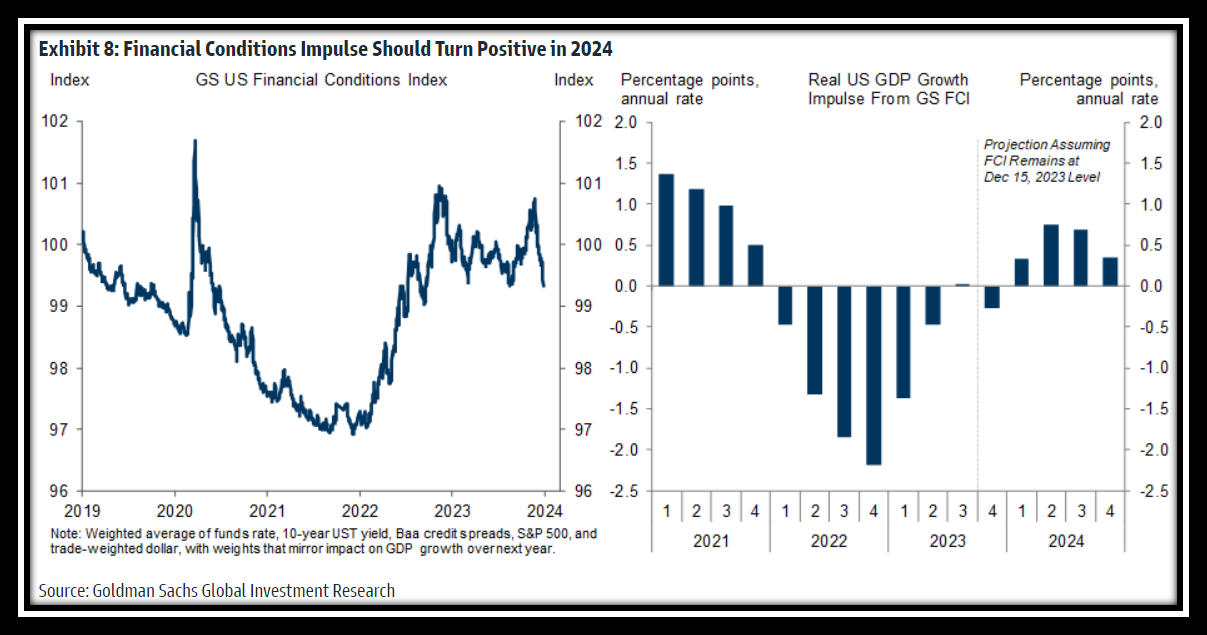

Until realized inflation data and/or the TIPS break-evens turn back up, risk assets are in a “Fed Put” regime where the Fed will likely cut rates to “normalize” Fed Funds even if economic growth is above trend and the labor market is tight, and will absolutely cut rates if the labor market deteriorates from here. Whether the Fed ends up cutting rates is irrelevant - the mere threat of this asymmetric cuts framework is enough to manage economic growth via broader financial conditions (as illustrated by Goldman above).

Rate Cut Framework

What has financial market participants in a tizzy is that it appears as though FOMC members are trying to walk back Powell’s dovishness. They’re not. They’re simply adding color to what Powell said at the press conference, which was: the Fed is starting to think about the framework for cutting rates.

As detailed by FRB Atlanta President Bostic and Cleveland President Mester, that framework currently has two components (I’m sure more components of the framework will be disclosed in the coming days and weeks):

No rate cuts until 3Q24, so the July 30-31 meeting at the earliest

The real Fed Funds rate, defined as Fed Funds minus one-year forward inflation expectations, will determine the timing and pace of cuts

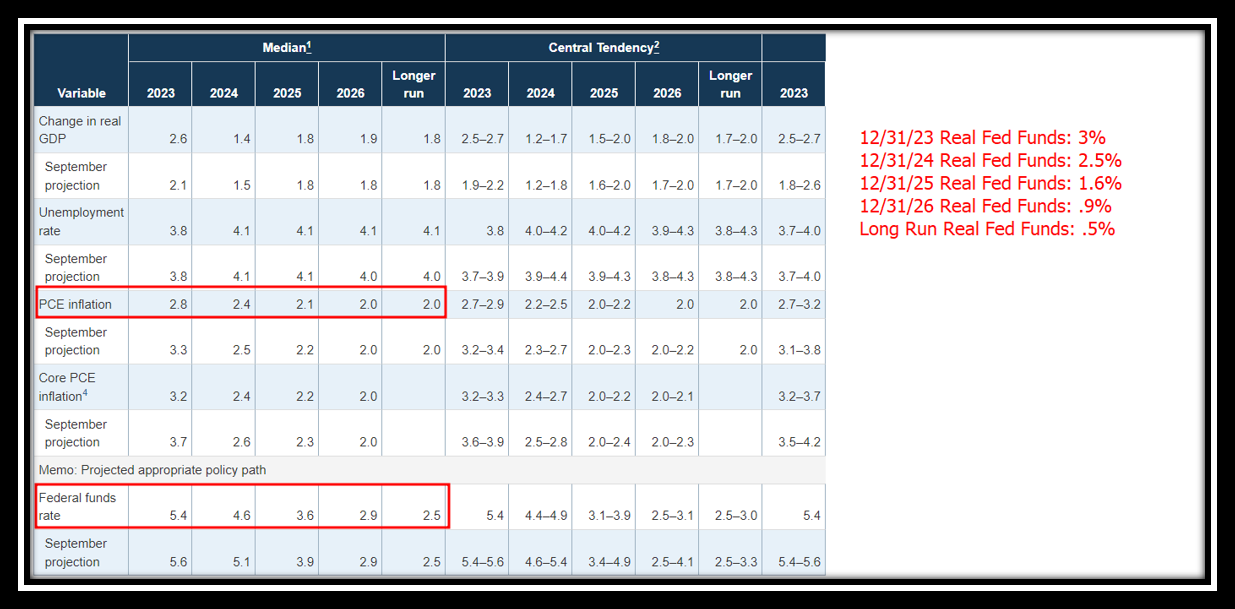

According to the December SEP, assuming the unemployment rate doesn’t shoot above 4.1% the Fed plans to exit 2024 with a real Fed Funds rate of 2.5%, calculated as 4.6% nominal Fed Funds minus 2025E core PCE inflation of 2.1%. (FED officials like to say that the SEP is not an FOMC “decision or plan”, but we all know that’s a lie - they mechanically set the projected real Fed Funds rate and then back into who needs to project what to get there.) Using the same formula for the December 2023 FOMC meeting, the Fed is exiting 2023 with a 3% real rate.

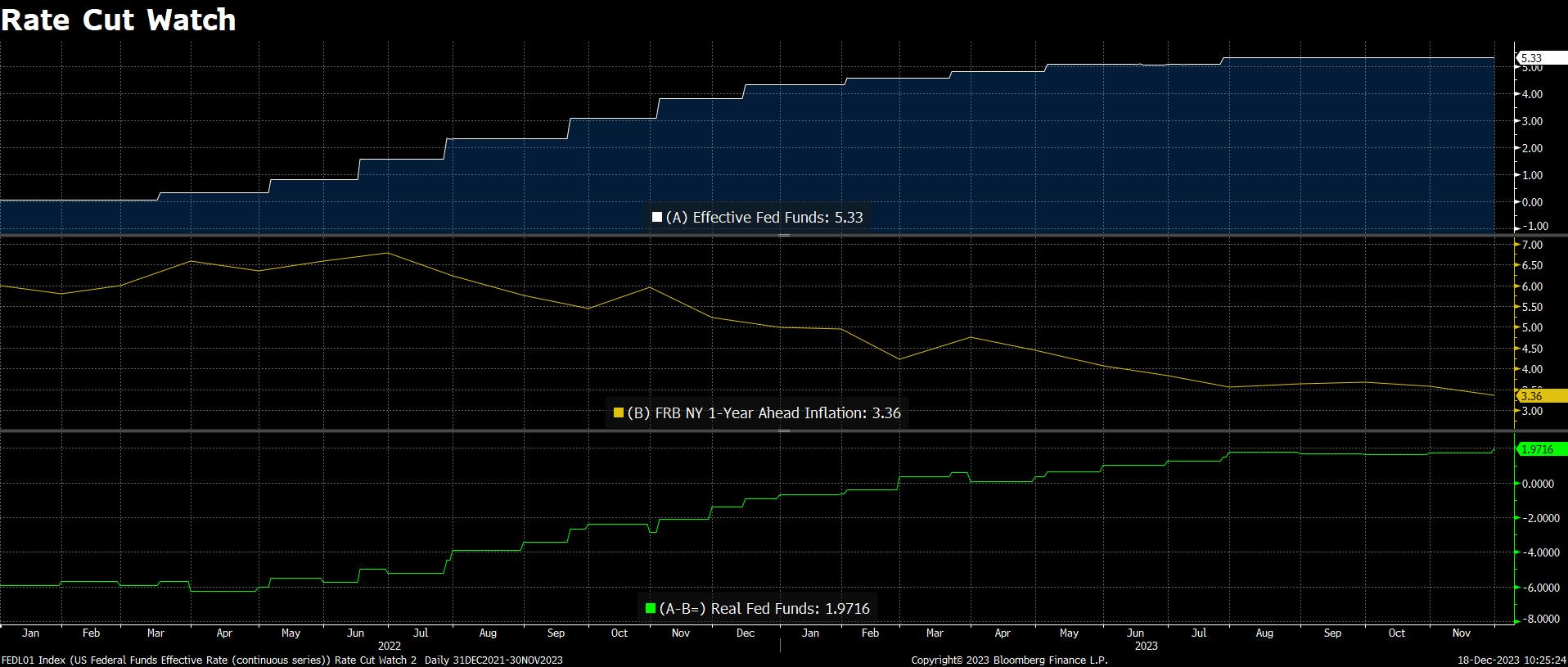

In the FT interview cited above Loretta Mester said that one-year forward inflation expectations will determine timing and extent of rate cuts. Using the 11/30/23 FRB New York median one-year forward inflation expectation the current 533 nominal effective Funds Rate is 197 bps on a real basis. Triangulating the current real Fed Funds of 197 with the Fed’s projection for a 250 real Fed Funds by 12/31/24 and the current exit rate target of 300, it’s likely that the Fed will start guiding to cuts once the FRB NY gauge falls to around 283 (this would yield a 250 real Fed Funds with a 533 nominal in place), and then start cutting once it falls to around 233 in order to keep real Fed Funds from rising above 300.

The next FRB NY inflation expectations report release is January 8. Given the move in TIPS break-evens, it would not at all be a surprise to see the one-year forward expectations fall from a current 336 down close to 300 if not slightly below, yet again ramping rate cut speculation as the critical 283 level comes into view. By January 8 equities should be right in the middle of a parabolic blow-off formation, so a cool report could very well catalyze a high-velocity leg higher in SPOOZ to at least 5000 (equity markets love big, fat round numbers regardless of fundamental justification).

2024 Burns —> 2025 Volcker

As stated above, until realized inflation data and/or inflation expectations turn back up the “Fed Put” will be sitting beneath the labor market, economic growth, and financial markets. But that’s not the only “put” sitting beneath labor, growth, and markets: The US government is running a 5-10% fiscal deficit, providing dollar for dollar stimulus to private sector net worth - a huge “put” beneath labor and growth; and then you have Treasury Secretary Janet Yellen and National Economic Council Director Lael Brainard sitting on over $1 trillion of pipelined QE in RRP/TGA, as well as a Treasury buyback program ready to be deployed in 2024 - the combination of which acts as a concrete floor beneath financial markets.

The economic and risky assets set-up heading into 2024 is extraordinarily bullish as a result of this triumvirate of government policy “puts”, and based on the statistics around various equity market breadth thrust signals, an SPX level of 5500-6000 sometime in 2024 is base case. But there’s a nasty “B side” to this Arthur Burns approach to government policy: Volcker cometh in 2025.

The soft landing path the US economy appears to be on has conjured up financial market fantasies of the Greenspan era in the late 90s, where he contained inflation with preemptive rate cuts, and then cut just in time to head off recession, launching the US economy and stock market into half a decade of booming growth and wealth creation while inflation remained tame. The perfect landing.

Ah, the Maestro. An American hero that only underwrote gargantuan bubbles in equities and housing that ushered in over a decade of Main Street pain in the wake of the GFC. What a guy.

The problem for Powell’s dream of the perfect landing is that he is pursuing it with a 5-10% fiscal deficit running in the background, unlike Greenspan who had a shrinking budget deficit in place to contain inflation while he eased the stance of monetary policy.

What’s going on right now is very straight forward: Inflation is going to come roaring back in the back half of 2024 and Powell will be forced to go full Volcker in 2025 in an attempt to retain some semblance of legacy by the time he is escorted stage left on May 15, 2026.

The Powell Fed has this idea that it can specifically and narrowly target and bring down inflation via a particular level of real Fed Funds while it maintains financial stability via balance sheet expansion (ala SVB) and keeps a floor under economic growth via FCI management (ala FCI easing since late October). But this will ultimately prove false…

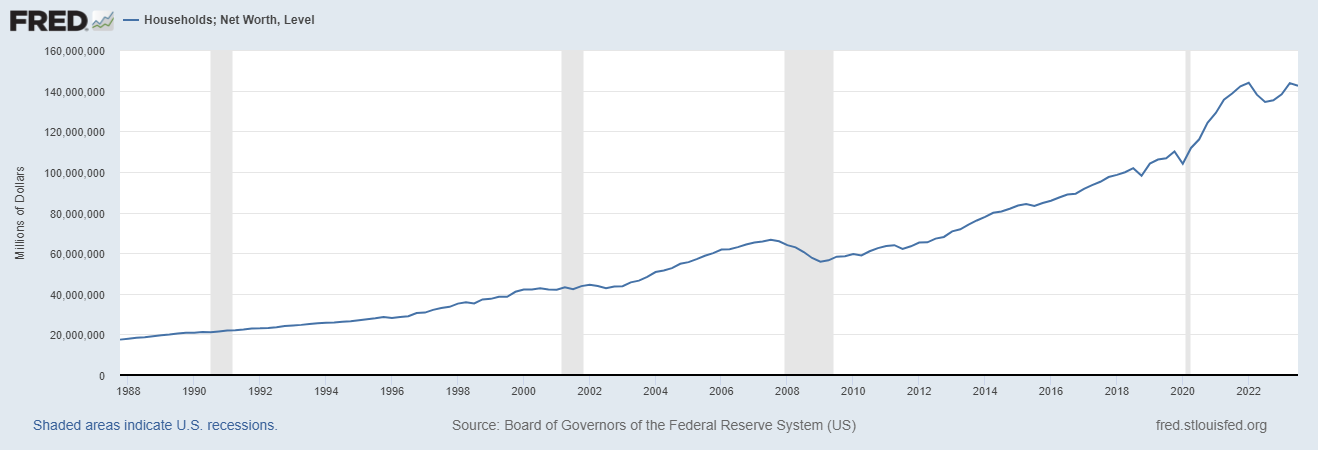

Not only is there far too much stimulus in the system as a result of the policy response to COVID (see net worth chart below), more stimulus is being added every single day the US government runs a fiscal deficit.

In short, Powell will wake up from his dream of a Maestro-like perfect landing staring into the Burns abyss and be forced to go full Volcker in 2025. Until then, we stay bullish of SPOOZ until circa 5500-6000.

love this