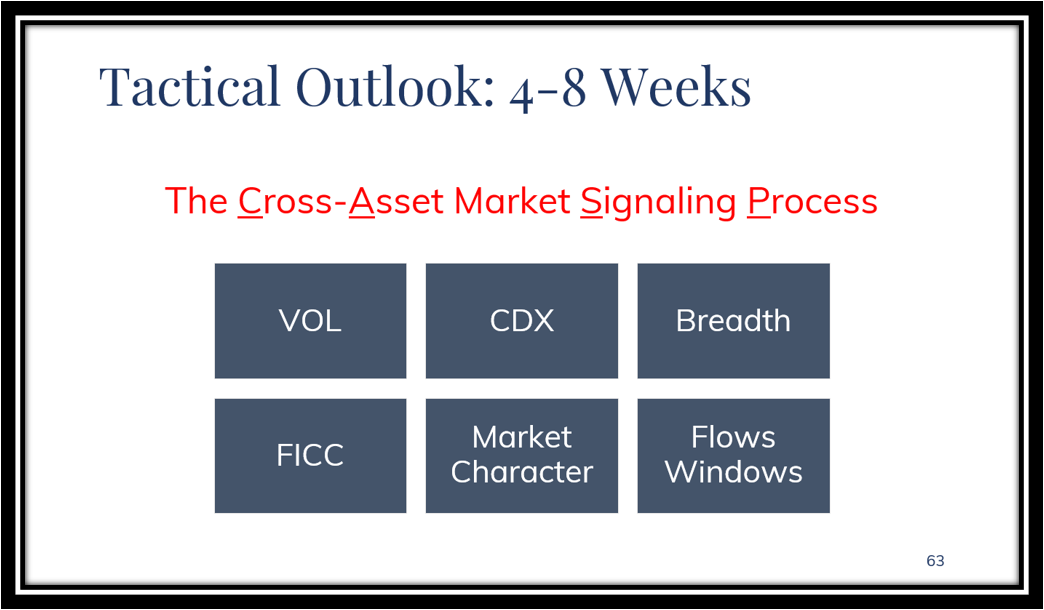

The CASP: January 4, 2024

The CASP: January 4, 2024

A post-breadth thrust overbought condition meets FED re-hawking, rising rates, and the rising probability Treasury re-hawks via the January 31 QRA. Downgrade tactical outlook to neutral (at best).

Analysis

VOL: The VOL complex could be in the early stages of signaling that equity market weakness lies ahead, but it’s not quite there yet. VVIX in particular has not reacted to this opening year equity market weakness with the standard sticky move higher that we would expect to see before a more material correction in equities.

Now, this could change in a matter of a single trading day. Given the emerging stickiness of the CDX complex and increasingly strong relative strength from defensive equities, we need to be on high alert. But looking at the VOL complex in a vacuum, this is unlikely the start of a material correction. More likely, in our opinion, this is the opening volley of downside volatility, and after a bearishly divergent rally back up close to the December highs if not a bit higher, then a more material correction can commence.

CDX: IG CDX is a concern here, as it is increasingly sticky and homing in on levels from August/September when SPY was circa $450 ($470 currently), UST 30s were over 430 (415 currently), and RSP was circa $150 ($156 currently). It’s still trading solidly below its 50dma, but once it crosses up above the 50dma the market tends to already be in correction. For larger 15-20% corrections the 50dma is a helpful tool, but if looking to tactically short a 5-10% pullback in equities then the 50dma tends to be a bit late. So close monitoring of IG CDX on a multi-day basis is key here, especially vis-a-vis the rest of the cross-asset market complex.

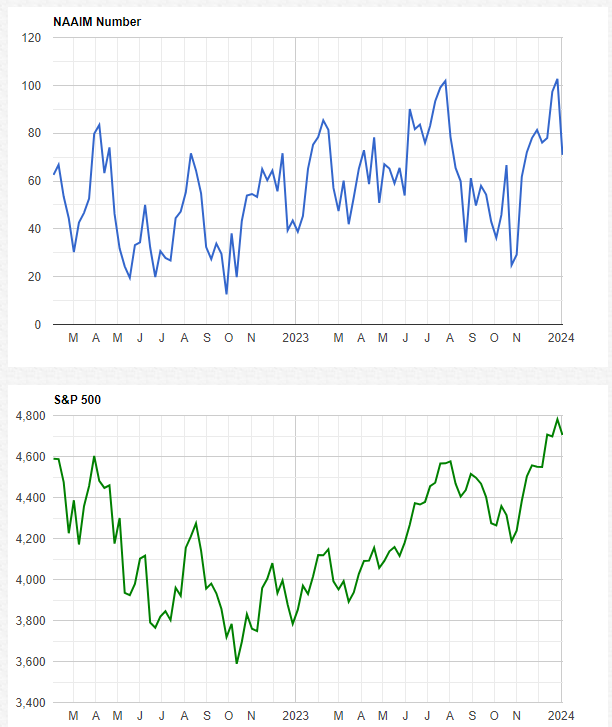

Breadth: The bottom line here is that defensive equity sector relative strength is starting to pick up, and while it is still very early days from a broad equity market signaling perspective, this needs to be watched very closely. The decisive downtrend in this area of the market in 4Q23 was strong confirmation that equities were headed higher, so if this dynamic flips into a new decisive uptrend, that has broad implications for not only equities but the economy itself. In new economic expansions defensive sectors lag, and in major bear markets defensive sectors lead. Bottom line. This area was a hugely important tell for us to pivot defensively in late 2021/early 2022, as it continued trending higher alongside CDXs while SPX tried to rally back in January 2022.

However, as we will discuss in an upcoming Cyclical CASP report, the recent series of breadth thrust signals that fired over the course of November/December MUST be respected. A -10% pullback following a 50dma thrust signal is par for the course, especially if the Fed is going to re-hawk here in response to overly loose financial conditions, but the series of thrust signals says that dip must be aggressively bought, likely ahead of large-scale economic/market intervention ahead of Election Day by Yellen and Brainard.

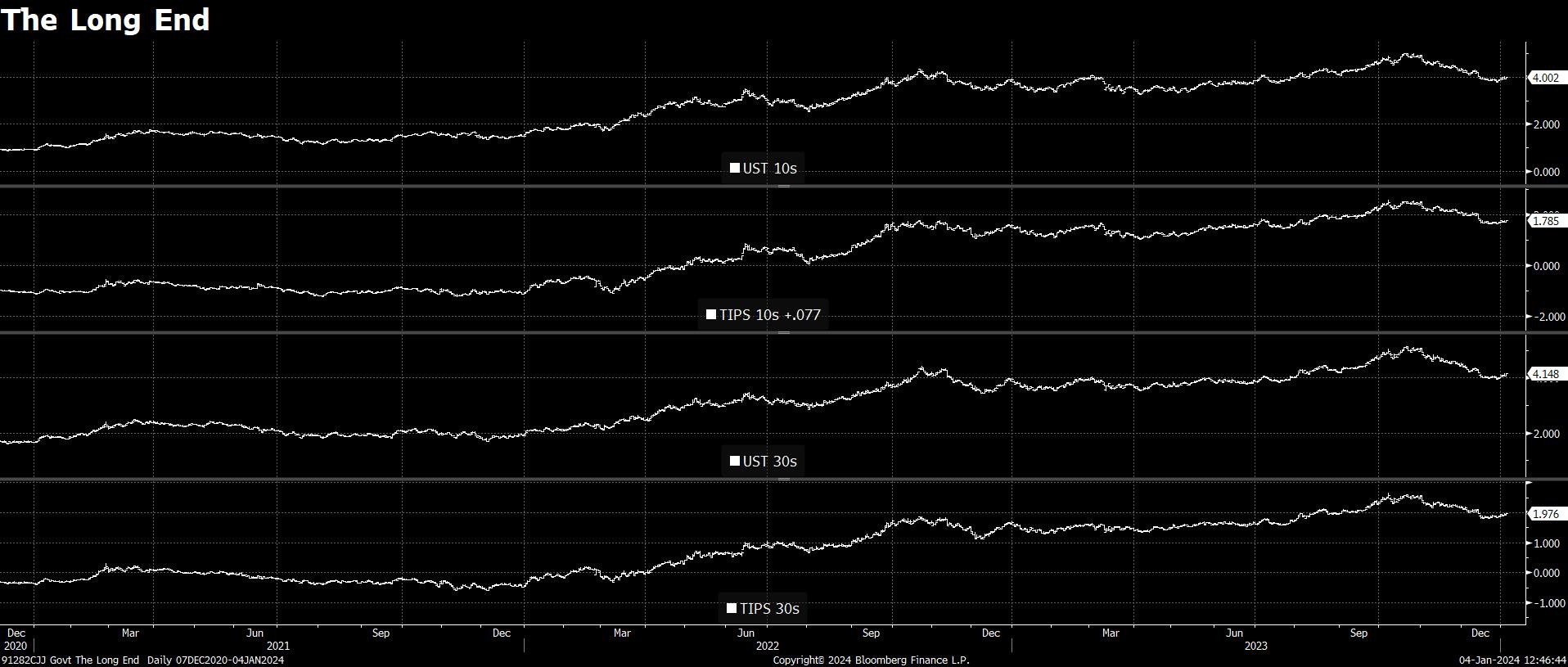

FICC: The direction of UST 10s and 30s remains critically important to the direction of equities, as since the FED/Treasury pivot in November/December stocks and bonds have been moving in lockstep. On December 29 via private Xwitter I flagged rates as critically important to watch and that if there is even a hint that Treasury/Yellen want to take advantage of lower rates to ramp coupon issuance on January 31 then the move back up in rates could be powerful. Unfortunately for our January/February SPX parabola thesis, equities are reacting very quickly to a so-far-modest move up in long rates. This is not good equity market character, since the recent easing of financial conditions very likely means the economy will not slowdown anywhere near enough in 2024 to warrant rate cuts, let alone the 6 that were priced in just days ago. If UST 30s in particular move back up to 450, there is very little chance SPX makes a new ATH anytime soon.

Key to the Fed’s reaction function to rising long rates is the TIPS break-evens curve. The curve remains well-anchored, so it’s unlikely FED will allow another sharp move up in long rates to the 450-500 range. But we’ll see. We were very surprised at the specific hawkishness of FRB Richmond President Barkin’s speech yesterday, which combined with the FOMC minutes suggests the Fed is not as amenable to a new economic upturn as it appeared in December.

Market Character: Correcting right out of the gate in a new year is no bueno, especially when BOY flows are supposedly so strong. Not good at all. Folks can poo-poo the “January effect” all they want because of its small sample size, but the fact of the fact of the matter is historically a weak January is not good for the rest of the year. So, adding it all up - bullish breadth thrust signals, Yellen/Brainard economic/market intervention ahead of Election Day, a hawkish FED despite well-anchored break-evens, and now a weak January - we may have to consider the possibility 2024 is a year of extreme chop ahead of a major bear market in 2025 when Powell will likely need to engineer a deep recession to take care of inflation ahead of his May 15, 2026 sell-by date.

In an extreme chop scenario it will be mission critical to not chase anything in either direction. Extreme patience and extreme selectivity on entry points for longs and shorts.

S&P 500

NASDAQ 100

Russell 2000

Flows Windows: As Cem Karsan flagged over the course of November and December, January 17 is a key date to watch for the end of BOY flows. So, the fact equities are so weak (not just down, that’s normal - it’s the cross-asset market action that’s notable) in this window of strength is a major red flag, at minimum for the 1Q24.

What’s interesting is that the market is following the seasonality path of an incumbent POTUS that fails to win reelection. Weakness right out of the gate before bottoming in March and finishing the year almost exactly flat. This path fits with the aforementioned “extreme chop” scenario.

Tactical Analysis: Negative price action in a window of strength, rates moving up, FED re-hawking, increasingly sticky CDXs (albeit from the lowest levels since December 2021), rising defensive equity sector relative strength, and negative election year seasonality all points to limited upside for stocks from here. The path for a parabolic blow-off into Jan/Feb was there, but with rates rising and the Fed re-hawking, the Goldilocks path to that blow-off has been blocked, especially with the market overbought following a powerful breadth thrust move. BUT…

Breadth thrust signals are critically important. Since 1970, when the 50dma thrust signal fires SPX has never been lower 12 months later on a price-only basis. This time could very well be different because of the Fed not allowing a new business cycle upturn to emerge without a FED policy response, but what we think is more likely is that the thrust signal is anticipating powerful economic/market support by Yellen and Brainard ahead of Election Day. So, whatever correction is coming most likely should be bought once an oversold sentiment/positioning condition emerges.

Looking out 4-8 weeks over the tactical time horizon, the outlook is at best neutral if not leaning bearish. It’s not yet outright bearish because positioning and sentiment has come in very quickly on not that big of a move lower. This is typical of a topping process, where the initial leg down is met with aggressive de-grossing followed by a bearishly divergent leg higher that either tests the prior high or makes a minor new high. On that December high retest, if the signals align we would quickly downgrade the tactical outlook to outright bearish.