The CASP: December 13, 2023

The CASP: December 13, 2023

Well-anchored break-evens keep further FED tightening at bay. But sticky supercore, overly aggressive cuts pricing, and rising asset prices promises a hawkish Powell. Buy the dip into 12/22.

Analysis

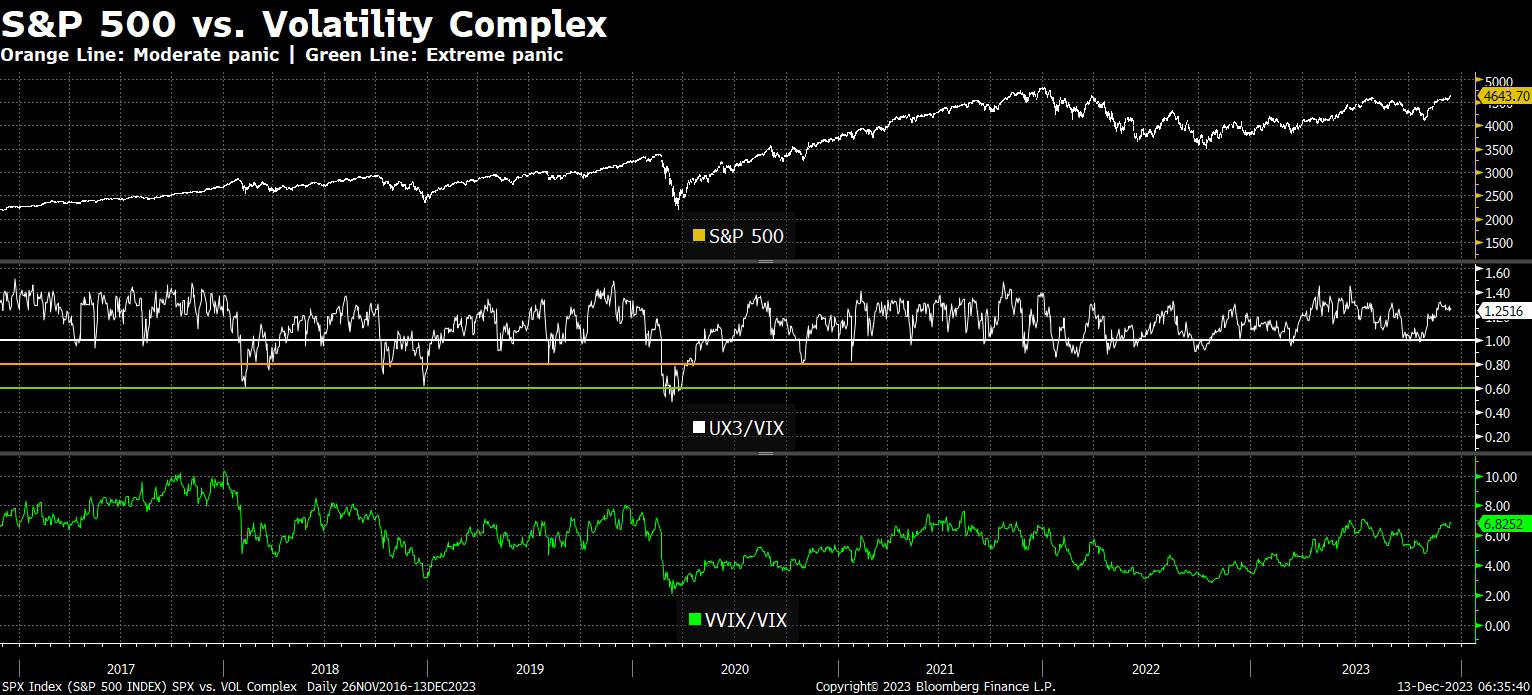

VOL: Bullish configuration with little to no sign of impending sustained market weakness. The only bearish signal in the last few trading days came right into the close yesterday when VVIX ripped alongside equities into EOD. This action speaks to the likelihood of a pullback on Powell today and post-12/15 OPEX, but a very buyable pullback ahead of a January/February 2024 parabola.

CDX: Full-blast risk-on. No divergences. And with IG CDX breaking down to new multi-year lows, one is forced to consider that perhaps a new business cycle upturn is in the works.

Breadth: A modest bearish divergence between SPX and NYSE 50dma breadth has emerged, and defensive sector relative strength has not made new relative strength lows alongside new SPX highs. Nothing major yet, but these divergences do support the prospect of consolidation in the very near-term. However…

The Banks/Utilities and Discretionary/Staples pairs have broken out, supporting the prospect equities continuing higher into early 2024.

FICC: The big UST 30s auction failure last month came with 30s above 450. Yesterday the auction went great with yields below 450. That’s a big tell that the bond market is more focused on growth and inflation than it is on sustained deficit spending, creating a Goldilocks backdrop for equities as growth and inflation slow just enough to contain the long end, but not enough to break the labor market.

But the big thing to focus on right now in FICC is the TIPS break-evens curve, which is very well-anchored right at 2% across the curve. FED messaging heading into today’s FOMC meeting suggests Powell is likely to be hawkish in order to halt runaway asset prices, at least for a time, but the fact break-evens are so well-anchored means the Fed can relax at a 533 Fed Funds and let the economy evolve as it will. As such, any hawkishness from Powell today is unlikely to underwrite more than a -3% pullback in SPOOZ.

Market Character: Extremely bullish. SPX is a runaway freight train right now, blowing through the 4515 JPM 12/31 pin and bullishly consolidating above YTD highs.

Flows Windows: OPEX is 12/15, after which there is a tiny window in which equities can pull back. No more than -3% though down to circa 4505.

SPX Tactical Analysis: Roger Ferguson’s interview this week (below) combined with FED messaging via Timiraos (see here and here) suggests Powell is going to push rate cut pricing into 2H24. How he does that is unlikely to be friendly to equities after having moved sharply higher into his speech. Given the animal spirits in place, I expect a stern Powell at 2:30PM EST. With July OIS Fed Funds priced for 473, Powell has his work cut out for him to get that back above 500.

The key problem for bulls and doves is that supercore inflation is not cooperating with the disinflationary path, and the Fed made it clear via Timiraos that it was not overly pleased with yesterday’s CPI report.

In short, break-evens keep the Fed relaxed about further rate hikes, but sticky supercore inflation and rising asset prices keep the Fed from cutting rates.

I’m looking for a buyable 1-3% pullback in SPX into Friday 12/22 catalyzed by a hawkish Powell and OPEX flows going away. That pullback will likely be the last opportunity to load up ahead of a January/February SPX parabola.