Market Journal: Topping Process Extended Not Ended

Market Journal: Topping Process Extended Not Ended

Topping process still very much underway, but more "vol unpinning" is required to clear the path for downside.

Discussion

I received more color around the structure of the volatility market this morning, and basically the market is back to being very pinned, which explains the lackluster velocity of the sell-off since June 15. Based on my read of the more fundamental factors underpinning the market - breadth, sentiment, credit - the big sell-off the S&P 500 is lumbering toward has just been pushed out, not canceled. Even if the SPX doesn’t really go anywhere for the next month, a month is a long time in vol premium land, so the set-up is there to take a major swing at September/October puts later this month.

Exhibits

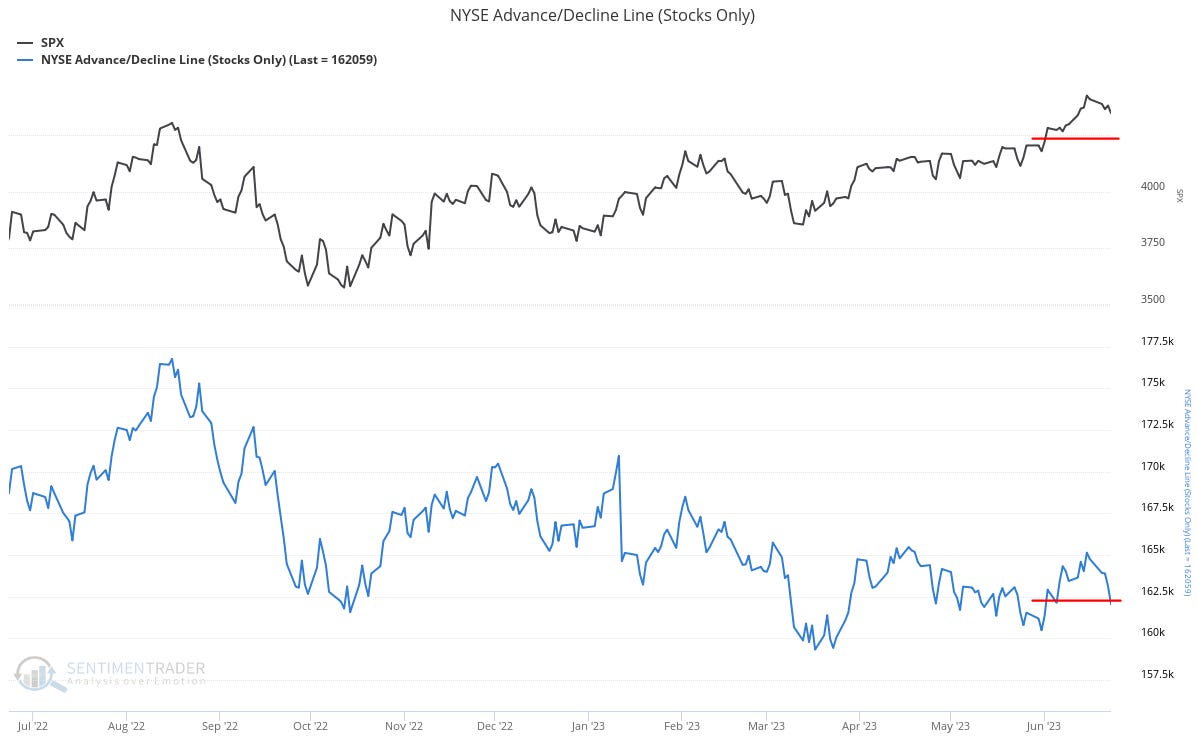

NYSE equity breadth says the SPX should be in the mid-4200s today versus mid-4300s. A material negative divergence on top of the already huge one that’s developed over the last 6 months. Really ugly market structure 8 months into a supposed new bull market.

HY CDX is negatively diverging from SPX as well. Not as badly as breadth, but a divergence nonetheless.

The most bullish dynamic for equities in the near-term is the severe underperformance of defensive sectors, specifically XLU and XLP (XLV is starting to perk up a bit). As the market headed into its August 2022 peak, XLU and XLP had starting to pick up relative performance steam, unlike today. This underperformance combined with action in the volatility space tells me there is more topping process left ahead of what is likely to be a very, very ugly September/October.

Lastly, as I referenced in today’s Fed Watch note, the 3y/10y UST curve is really starting to move again, back up to 116% this morning. Who knows how Fed policy is likely to unfold from here, but regardless of the realized path of policy this 3y/10y curve action tells me that realized path of Fed policy will be tight. For instance, if equity and credit risk premiums start to blow out, the Fed won’t need to hike anymore - but merely holding Fed Funds where it is means policy will remain quite tight.