Market Journal: EOD Update and Other Musings

Market Journal: EOD Update and Other Musings

AAPL and AMZN represent upside “gap risk”? Really? Focus on NFP.

Discussion

Since the mid-day update, cross-asset evidence shifted in a modestly bullish direction with defensive sector relative strength flagging, NDX relative strength firming, VVIX selling off a bit, and rates consolidating. But this bullish shift was nothing like the early July intra-day move in the wake of a stronger than expected ADP report. Today was a relatively flaccid attempt by bulls to engineer their patented late day 0DTE squeeze.

There’s chatter across “FinTwit” that AAPL and AMZN earnings tomorrow represent upside “gap risk” for shorts, hence the stabilization of indices toward EOD. If that’s the bull case, I’m happy to take the other side of that.

AMZN is likely to gap up in response to better than expected earnings, as it is in a classic post-multi year underperformance recovery pattern, but AAPL is overpriced (absurdly so?) and directly in the cross hairs of the discretionary spending slowdown likely to hit with a lag on the back of the fastest rate hike cycle in modern financial market history. Setting aside the fact two stocks worth 10.63% of SPX (as of the August 1 close) are highly unlikely to prop up a market littered with overvalued stocks selling off in response to solid earnings reports (a 10% spike in both names means SPX would gap up by 1.063%, ceteris paribus), at best AMZN gaps up by 5% and AAPL is flat, for a grand total of 15.3 bps of “gap risk”.

Enough of that.

The real fun this week comes via NFP on Friday. Ya, Claims tomorrow would be a big deal if they spiked well above 227k consensus, but that seems unlikely given how sticky rates have been, the spike in YoY tax receipts referenced in the mid-day update, and today’s strong ADP report; but NFP is the big kahuna. Consensus is 200k on jobs and 4.2% on AHE, and if those come in at 150k and 4%, the soft landing narrative would dominate the narrative and SPX would truly gap up; but Goldman has NFP at 250k!!! Goldman is in line with consensus on AHE, but 250k NFP would rubber stamp the move in rates, IMO.

Bottom line: I think the window is open for a sell-off down to the 50dma circa SPX 4400 ahead of the August 10 (next Thursday) CPI report, catalyzed by a strong to very strong NFP this Friday. From there (probably by next Monday, since markets “never bottom on a Friday,” per Jeff Saut), SPX should stabilize in anticipation of another soft Core CPI report next Thursday, and if CPI cooperates, a rally should occur into the August 16-18 OPEX window.

FED Chair Powell speaks at Jackson Hole the Friday after OPEX (August 25), so it’s tough to see high velocity downside occurring ahead of that; but once we get Powell’s dovish musings out of the way, the door to retest of the October 2022 SPX low of 3490 sometime in the September/October danger zone is WIDE open.

Whatever SPX wants to use as an excuse for a retest of 3490 by September/October is fine by me. Better than expected economic data that underwrites an upward breach of 500 on UST 30s? Go for it. The long and variable lags of the fastest rate hike cycle in modern financial market history coming off perhaps the longest period of ZIRP in modern financial market history hitting all at once in September/October, leading to an unraveling of the labor market? Fine.

Bear markets end with the 3y/10y UST curve below 100% and/or 90% of stocks moving above their 50dma. Neither has happened since October 2022.

So, very simply, until then we look down, not up.

Exhibits

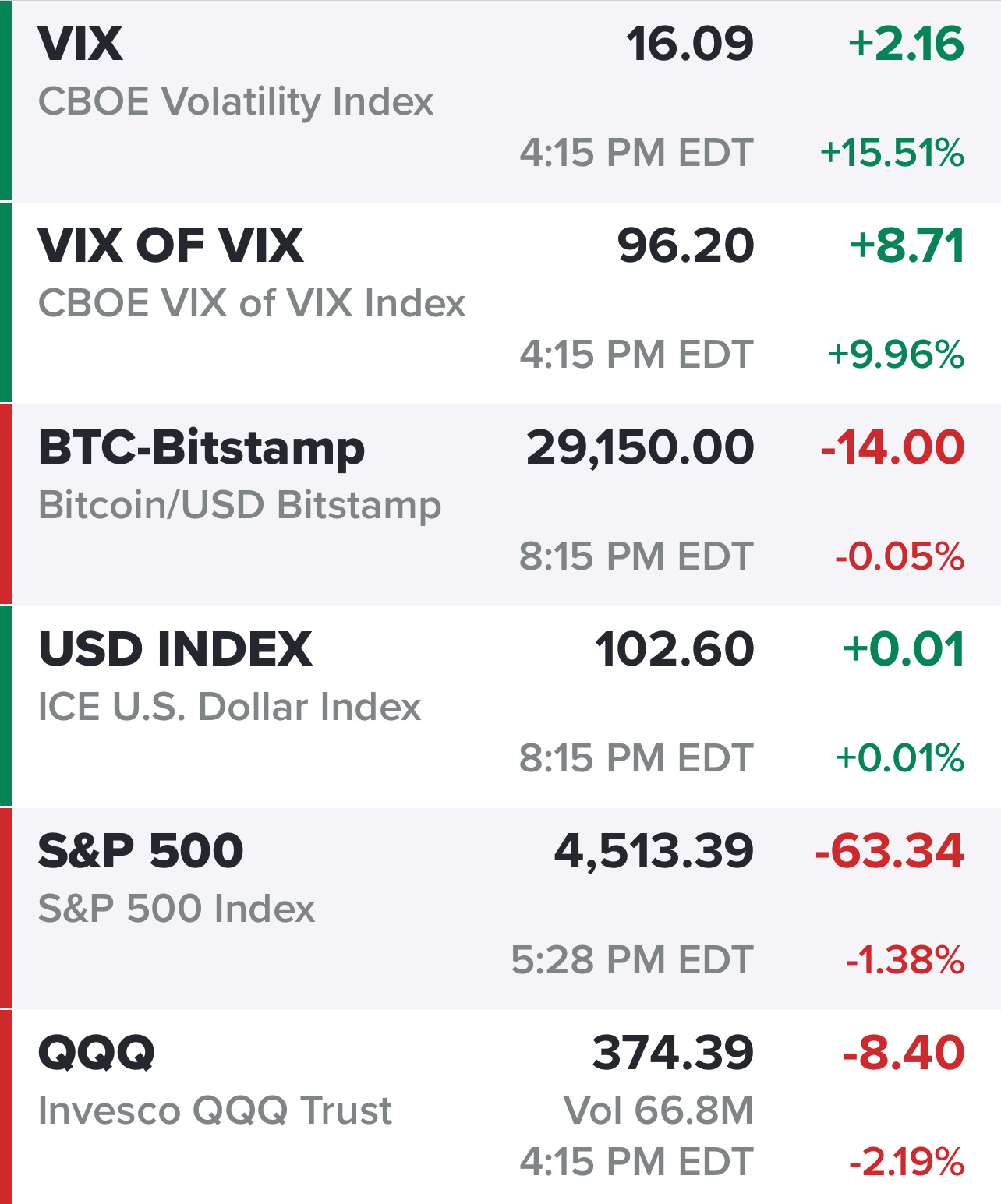

VOL sold off a bit throughout the afternoon, a modestly bullish development. But nothing like most BTFD days since April.

Defensive sectors outperformed on the day, but relative strength did come in a bit through the afternoon.

Rates consolidated through the day, contributing to the improvement in NDX relative strength in the afternoon.

Thursday is important for Claims data.

But NFP is huge. If Goldman is right on 250k, look for the rate rip to continue.