Market Journal: EOD Update

Market Journal: EOD Update

Defensive sector price action the key “tell” today.

Discussion

The intra-day reversal in equities was led by defensive sectors, XLV most powerfully, and HY CDX actually spiked EOD despite SPX and NDX closing close to their reversal highs. This looks like a textbook counter trend reversal destined to fail in short order.

There’s a reason it’s often said there’s nothing like price to change sentiment. Last week, the combination of the breakout in long rates and rising TIPS break-evens suggested the economy is more resilient than recession camp believes and/or a reaccelerating of long-term inflation expectations was becoming embedded in market psychology. This week, in the wake of a soft NFP last Friday, the reversal in rates appears to be pointing back in the direction of the 3/4Q23 recession start date so often discussed here. Frankly, I wouldn’t be surprised if both were true, as there is a very plausible path to the 3/4Q23 recession start date so often discussed by The Kitty, and a simultaneous breakout in long rates on the prospect of even greater fiscal expansion in response to said recession.

I don’t know what the trade is around Thursday’s CPI report. On one hand, the options guys are saying “event VOL” is elevated and that any good news that comes out of the report will be met with a collapse in elevated VOL, underwriting a squeeze rally driven by a buyback of options hedges by dealers. But on the other hand, with the Fed Funds futures market pricing in rate cuts starting in 1Q24 there is no room for the Fed to dovishly talk up rate cuts in response to a soft Core CPI print. Perhaps elevated VOL is hedging against an upside surprise in headline CPI, in which case a downside miss on headline would be a relief? If the market is defensively positioned for a hot headline CPI, I would fade that. I don’t think hot headline CPI matters until the entire TIPS BE curve starts moving up. But…

…I don’t think hot headline CPI is why VOL is elevated right now. I think something stinks beneath the surface of this soft landing squeeze, and the fact the market is weak in a “window of strength” is a major tell. IFF guided down and the stock got hammered; ZIP just withdrew guidance on labor market deterioration; AAPL got slammed EOW last week on little to no news; China is a problem - all with valuation and positioning very full.

I’m ready and waiting for an opportunity to buy a local low in advance of one last move higher before September/October. But I don’t think we’re there yet. I think we need a mini-washout before Powell on 8/25, then a rally on him softening his tone as he calmly lays out the Fed’s endgame for its War on Inflation. If today was the local low, defensives would not have led off the bottom and HY CDX would’ve gotten torched. Not there yet.

Exhibits

Defensive sectors outperformed smartly on the day and led off the bottom.

HY CDX came off as the market rallied, but move up into EOD even as SPX and NDX spiked into the close.

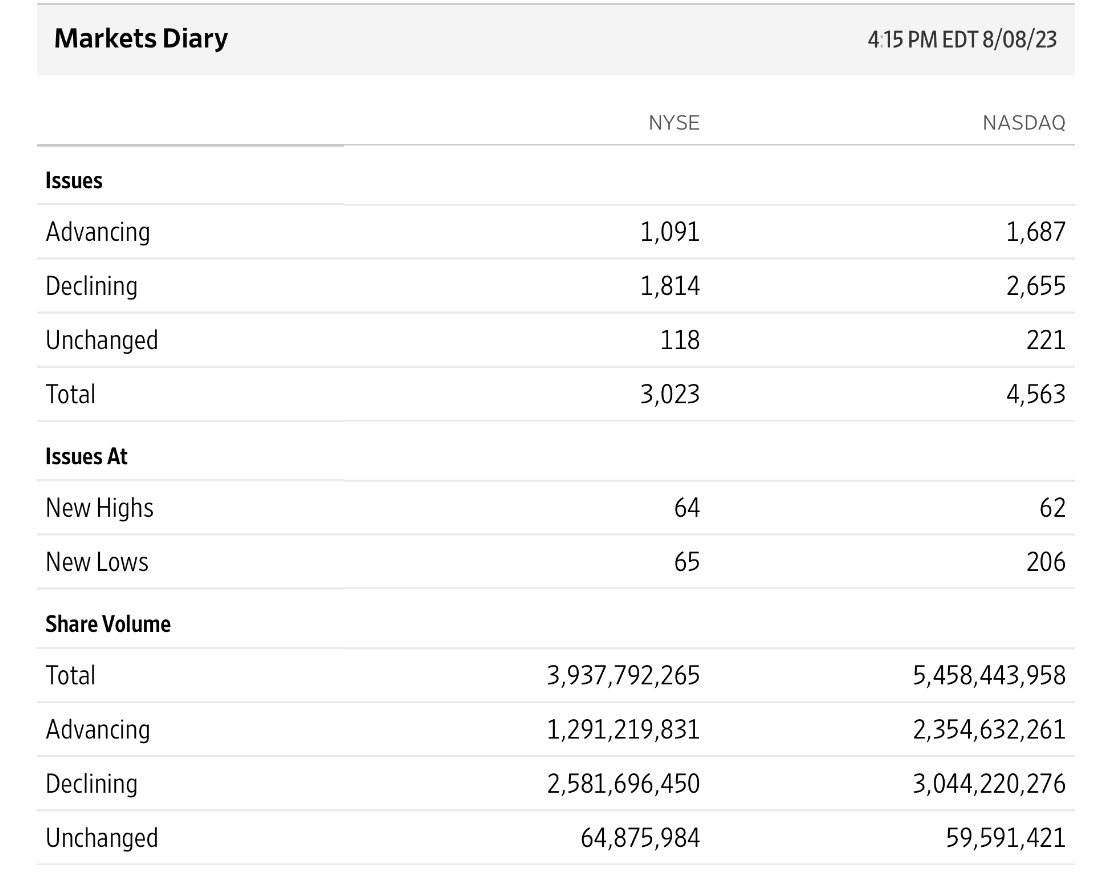

Breadth was poor, but not horrendous. NAZ new lows, however…

SPX BPI says we’re in the early stages of a pullback.

Mixed picture on inflation.

The Kitty continues to be key.