Market Journal: 1987 Still on the Mind

Market Journal: 1987 Still on the Mind

Discussion

Bulls can take heart that it appears central banks are working over time to prevent the fundamental collapse in equities that fundamentals say should occur. This weekend the Fed coordinated with the BOJ to smooth out the on-going adjustment in BOJ monetary policy, and equities responded by gapping higher this morning and largely holding their gains alongside a fall in credit default swaps.

The problem for bulls is that negative divergences continue to pile up across the cross-asset spectrum, TIPS break-evens are moving higher on the back of a weakening USD, and the 1987 analog continues to hold.

As discussed this morning, in my read of the evidence the playbook is for a sell-off on CPI this week perhaps into Thursday, followed by a relief rally into Powell next Wednesday. Once we get through Powell and September OPEX, the decks should be cleared for a major correction into October…as long as the long end of the curve breaks out to new highs, ala 1987. If rates stay where they are and economic data just sort of hangs in, choppy range-bound action is likely in place until the economy finally cracks.

Exhibits

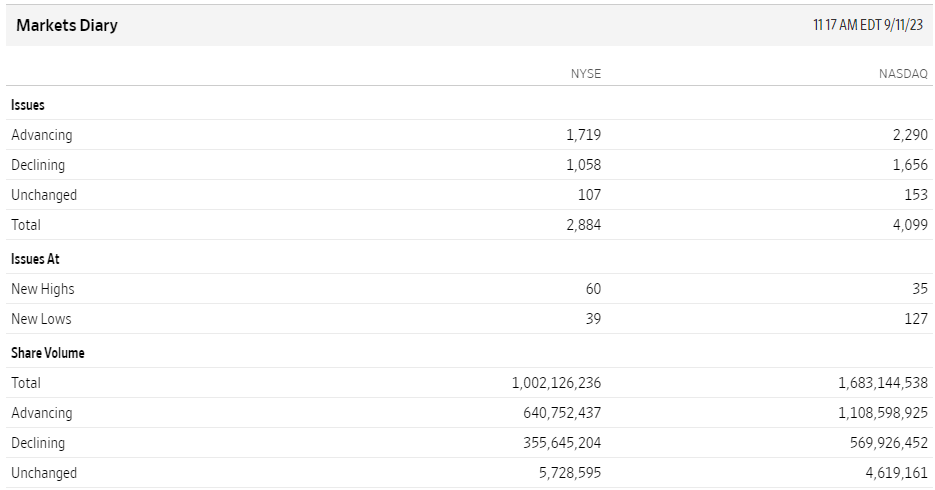

HY CDX is down today alongside higher equities, but defensives are outperforming and breadth is very poor. The only thing going for bulls here is that VVIX is not up as much as VIX, and VOL has overall faded through the morning. The problem is that VOL is green overall on a green day for stocks. So sort of a neutral signal there, IMO.

The biggest issue for the bulls is the fact TIPS break-evens are on the move again on just a small move down in USD. This is a major reflationary problem for a bull case that rests on the Fed easing off on falling inflation. No bueno.

IMO, the combination of a hot CPI print and a hawkish BOJ could combine to drive rates to new highs this week, ala 1987. The prospect of Powell next Wednesday likely keeps the sell-off contained, but the set-up is there for a 1987 event post-Powell and September OPEX.