Fed Watch: A Hugely Hawkish Lagarde

Fed Watch: A Hugely Hawkish Lagarde

Ebullient financial markets are underpinning central bank re-hawking, sowing the seeds of economic destruction.

Discussion

European economic data are deteriorating quite quickly and the German 10-2 curve is deeply inverted, yet Lagarde came out this morning swinging, detailing the ECB’s plan to find a sufficiently restrictive level of policy that “locks in” disinflation and hold it there “for as long as necessary.” This dynamic of hawkishness in the face of deteriorating macro data highlights well how unbelievably dangerous fighting central banks is.

The ONLY reason central banks are this comfortable re-hawking is because financial markets are ebullient. The only reason. If banks were exploding left and right, stocks were in a bear market, and credit spreads were blowing out, they would deem their policy stance to be “sufficiently restrictive.” But instead, financial market participants around the world continue to “fight the Fed”, declaring monetary policy is impotent as a result of still-strong fiscal stimulus. In short, global equity investors continue to sow the seeds of economic destruction, as elevated equity markets push central banks to continue tightening policy well beyond what the bond market has deemed is necessary.

Once we get the “crack” (you’ll know it when you see it), no amount of high-cost liquidity (i.e. the BTFP facility) can solve what comes next. Only rate cuts and QE will prevent the S&P 500, for example, from falling below 2500. It’s just logic and math.

Central banks are setting policy on the most lagging of lagging data (inflation and labor), guaranteeing recession of likely sizable severity

Since 1969, the S&P 500 has troughed in and around recession at 10.2x peak EPS, which would put the trough for this cycle at SPX 2000

Lagarde speech:

https://www.ecb.europa.eu/press/key/date/2023/html/ecb.sp230627~b8694e47c8.en.html

Exhibits

The conclusion to her speech was 2022 Jackson Hole Powell-esque. “Monetary policy currently has only one goal.”

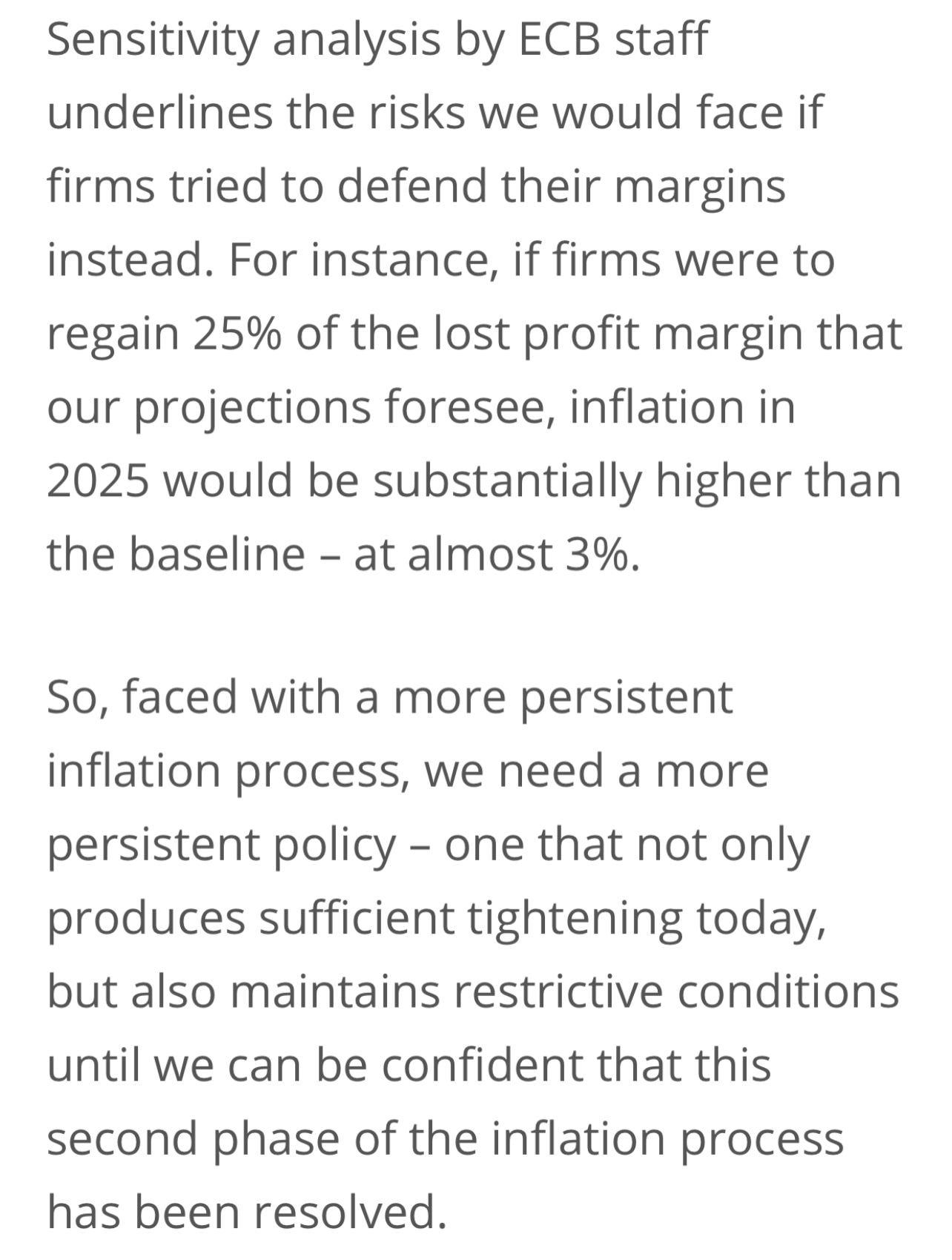

Heavy focus on wages, but with a new twist: Lagarde calls out corporate profit margins as the likely source of disinflation so that labor doesn’t have to bear the brunt of the slowdown.

Two sources of uncertainty: inflation persistence and transmission.

How to deal with the uncertainty? Set the policy rate using lagging data, then maintain an anti-Burns reaction function until inflation is structurally back to 2%.

All of the above against the backdrop of a severely inverted German 10-2 curve.